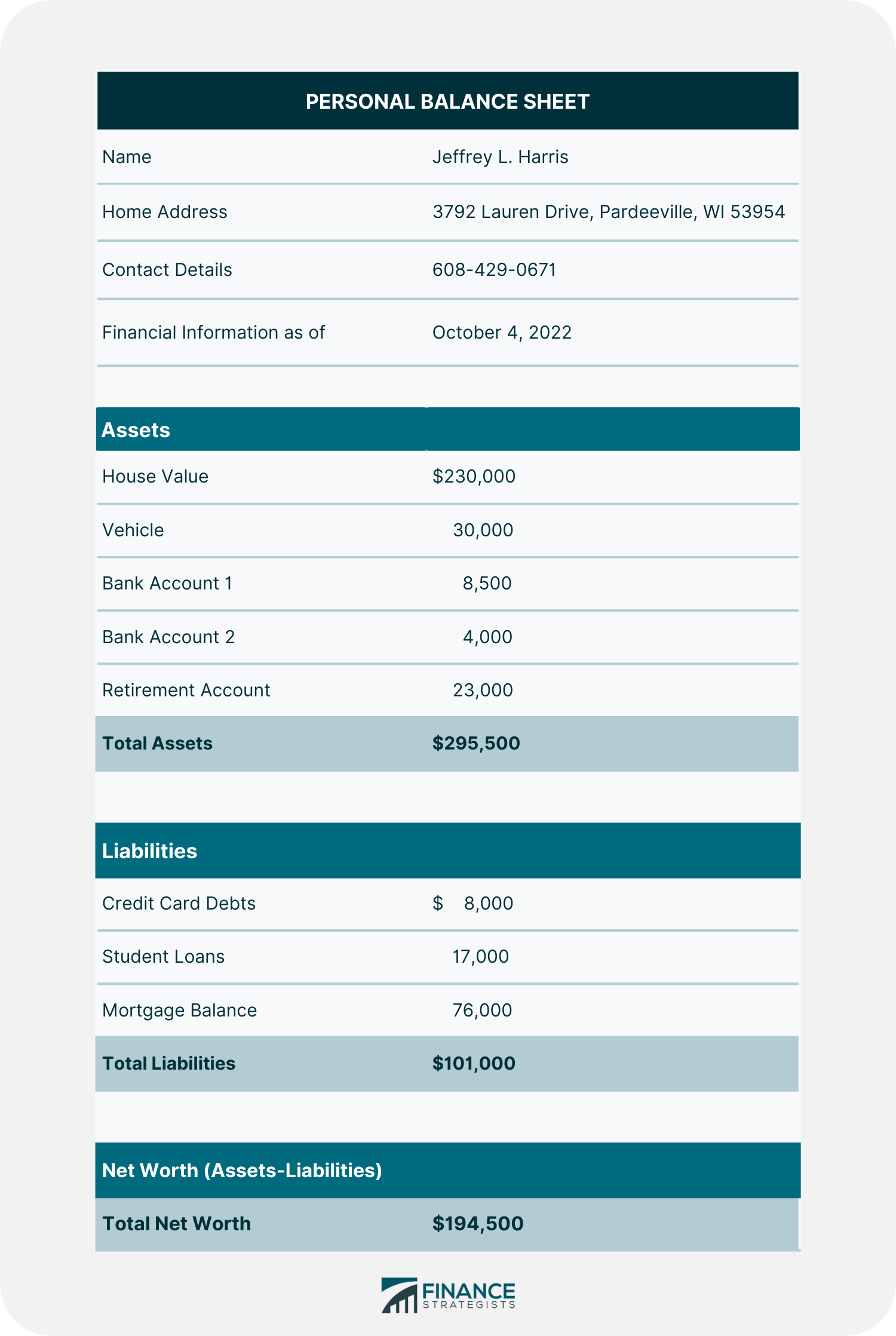

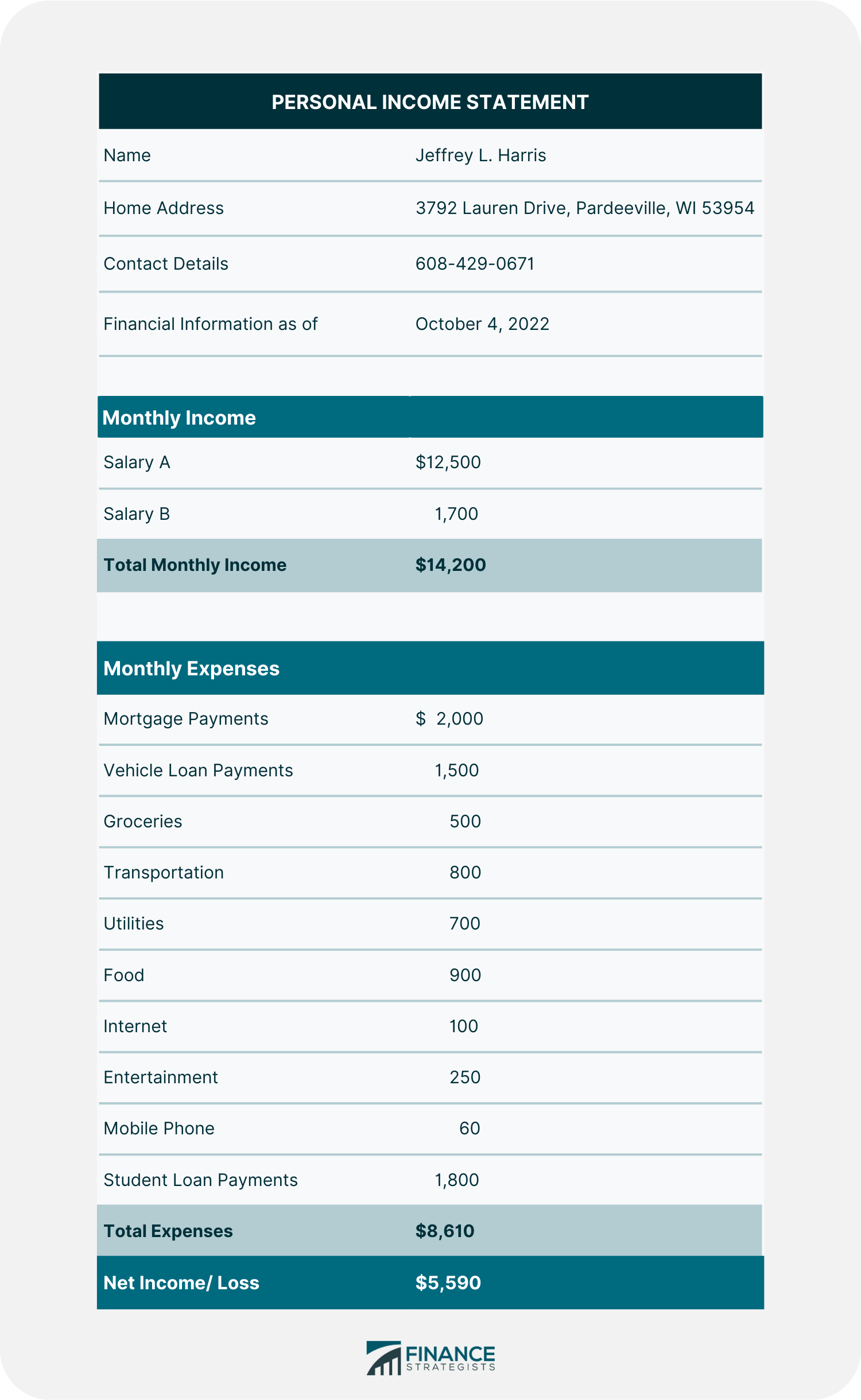

A personal financial statement is a report or set of documents that summarizes an individual's financial situation at a particular time. It is often divided into two sections: the balance sheet and the income statement. The balance sheet provides a breakdown of assets and liabilities, while the income statement summarizes income and expenses. General information about an individual, such as name and address, may also be included in a personal financial statement. Individuals can use personal financial statements to monitor their current economic situation. A personal financial statement is typically divided into two sections. These are: The financial statement contains a section known as a balance sheet, which summarizes a person's assets, including cash and investments, and liabilities like debts or loans. The balance sheet is also used to calculate an individual’s net worth, which is the value of assets minus the amount of liabilities. The next section, the income statement, details the flow of income and expenses that influences a person's financial situation. Income statements list all sources of income, such as salaries, bonuses, and dividends. Expenses such as insurance payments, electricity, or grocery bills are also included. A personal financial statement does not include the following items: Company resources and debts are removed from the financial statement unless the individual has direct and personal responsibility. When someone personally guarantees a loan for their business, the loan is included in their personal financial statement. Loaned assets are not owned, so they are not included in personal financial statements. However, if an individual owns a property and rents it out to others, then the property's value is included in the financial statement list. Furniture and home goods are often not shown as assets on a personal balance sheet since they cannot be easily sold to pay off a loan. Personal goods with high monetary value, such as jewels and antiques, may be included if their worth can be shown by an evaluation. Let us look at an example of a personal financial statement using the hypothetical case of Jeffrey. Below is an example of what Jeffrey’s balance sheet may look like in spreadsheet form. As shown above, Jeffrey has $295,500 worth of assets. This includes the assets like a house, a vehicle, bank accounts, and a retirement account. Now let us say he has $101,000 in liabilities as well. This includes credit card debts, student loans and mortgages. With this information, his balance sheet should reflect a net worth of $194,500. Here is an example of what Jeffrey’s income statement may look like in spreadsheet form: As shown above, Jeffrey receives a total monthly income of $14,200 and spends a total of $8,610 in expenses. After subtracting expenses from income, Jeffrey has a net income of $5,590. Taken together, Jeffrey’s balance sheet and income statement provide useful information about his current financial situation. Let us look at a guide on how to create a personal financial statement. Indicate the dollar value of the assets to be declared. Accuracy is important, particularly when creating a statement for the purpose of borrowing. Find the total value of all available assets. Liabilities come from debts. State the obligations that have to be settled and debts to be paid. Common items include credit card debts, mortgage debts, and student loans. Find the total value of all liabilities. Net worth is calculated by deducting total liabilities from total assets. Determine the amount of money coming in from various sources. This usually includes regular income received monthly. Make a list of all monthly spending. Start with fixed costs before moving to variable costs. The net profit or loss can be calculated by subtracting the total monthly expenses from the total income or revenue generated in that month. Here are some reasons why it is important to create a personal financial statement. A personal financial statement is an important tool that can be used for financial planning. It provides a snapshot of an individual's financial situation at a particular point in time, which can be helpful in making future projections and plans. The statement can also be used to track progress over time and to identify areas where improvements can be made. Personal financial statements are essential when filing taxes because they summarize income made throughout the year. They also provide an idea of possible deductions that can be made to lower an individual’s tax rate. Personal financial statements are often required when applying for credit, such as a loan or mortgage. Lenders use the information in the statement to assess an individual's ability to repay the debt and to determine the interest rate that will be charged. In some cases, a personal financial statement may be used in lieu of a credit report when applying for credit. A personal financial statement can be a helpful tool in managing finances and making future plans. Personal financial statements include balance sheets to monitor assets and liabilities and income statements to track an individual’s income and expenses. Details on the assets and liabilities related to an individual’s businesses, any rented items and personal belongings are not included in a personal financial statement. Personal financial statements can be used for a variety of purposes, including financial planning, overviewing an individual's financial situation, and loan applications. Personal financial statements must be updated on a regular basis to provide an accurate picture of an individual’s current economic situation. What Is a Personal Financial Statement?

What Personal Financial Statement Includes

Balance Sheet

Income Statement

What Personal Financial Statement ExcludesCompany Assets and Liabilities

Loaned Items

Personal Belongings

Personal Financial Statement Example

How to Create a Personal Financial Statement

How to Create a Personal Balance Sheet

How to Create a Personal Income Statement

Importance of a Personal Financial Statement

Financial Planning

Taxes

Loan Application

Final Thoughts

Personal Financial Statement FAQs

A personal financial statement is a report or set of documents that summarizes an individual's financial situation at a particular time.

A personal financial statement includes information on an individual's balance sheet and income statements. The balance sheet provides a summary of assets and liabilities, whereas the income statement summarizes revenue and costs.

Personal financial statements do not include details of a company’s assets and liabilities, loaned items, and personal belongings.

It is important because it provides a snapshot of an individual's financial situation at a particular point in time. It can help to identify areas where expenses may be excessive or where there is room to make cuts in order to save money. The statement can also be used to track progress toward financial goals.

A personal financial statement shows an individual's assets, liabilities, income, and expenses. It can help to identify areas of financial strength and weakness and to track progress over time.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.