The Unit Benefit Formula is a method used in pension plans to determine an employee's retirement benefits. The formula is based on the employee's years of service and earnings, providing a specific percentage of the employee's salary for each year worked. This method aims to reward long-term employees and encourage employee retention. Its purpose is to reward longevity and earnings, encouraging employee retention and providing a predictable retirement income. However, it can be complex to understand, potentially leading to misconceptions, and may be costly for employers to maintain. Furthermore, the formula's results can be significantly impacted by economic and demographic trends. Unlike other pension formulas such as the Flat Benefit, Career Average, and Final Pay Formulas, the Unit Benefit Formula considers the employee's earnings, providing potentially higher benefits for those with higher salaries. Each of these formulas has its advantages and disadvantages, making the choice between them dependent on various factors, including the specific goals of the employer and the employee's career trajectory. Understanding the Unit Benefit Formula is vital for employees, employers, and financial planners. For employees, it offers a clear picture of their potential pension benefits. For employers, it helps design attractive retirement packages for staff. For financial planners, it is a necessary tool for accurate retirement planning. The Unit Benefit Formula generally takes the form of a percentage of the employee's average salary multiplied by years of service. The components include: Percentage factor: This is a fixed percentage defined in the pension plan. Average salary: This may be the average of the employee's earnings over a specified period or their final salary. Years of service: The number of years the employee has worked for the employer. The Unit Benefit Formula calculates a pension benefit as a fraction of the employee's salary for each year of service. For example, a plan may provide 1.5% of the employee's average salary for each year worked. If an employee has an average salary of $50,000 and has worked for 20 years, their annual pension benefit would be $15,000 (1.5% * $50,000 * 20 years). Calculating the Unit Benefit Formula is straightforward. You multiply the percentage factor by the average salary and the years of service. The result is the annual pension benefit the employee will receive upon retirement. The Unit Benefit Formula is pivotal in determining an employee's pension benefits. It helps quantify the reward for the employee's service duration and earnings. By using this formula, both the employer and the employee can estimate the potential retirement benefits, aiding in financial planning. The Unit Benefit Formula provides a predictable and secure retirement income based on a worker's salary and years of service. It benefits long-serving employees by rewarding their loyalty and service duration. It also provides employers with an effective tool to attract and retain talented employees. The main disadvantage of the Unit Benefit Formula is its complexity compared to other formulas like the Flat Benefit Formula. It may be challenging for employees to understand, leading to potential misconceptions about their retirement benefits. Additionally, it can be costly for employers to maintain, especially if employees live longer than anticipated or if investment returns on pension funds are lower than expected. The Flat Benefit Formula provides a fixed amount per year of service, regardless of the employee's salary. In contrast, the Unit Benefit Formula takes into account the employee's earnings, potentially providing a higher benefit to those with higher salaries. The Career Average Formula uses the average salary over the employee's entire career to calculate retirement benefits. The Unit Benefit Formula, on the other hand, often uses the average salary over a specified period or the final salary, which can result in higher benefits for those whose earnings increase significantly over their careers. The Final Pay Formula calculates benefits based on the employee's final salary, rewarding those whose earnings peak towards the end of their careers. While the Unit Benefit Formula may also use the final salary, it often uses the average salary over a certain period, which can result in lower benefits if the employee's salary decreases towards the end of their career. The Employee Retirement Income Security Act (ERISA) in the U.S. sets minimum standards for pension plans in private industry, including those using the Unit Benefit Formula. These standards aim to protect the interests of employee benefit plan participants and their beneficiaries. Employers using the Unit Benefit Formula must ensure their plans comply with the regulations set by ERISA and the Internal Revenue Service (IRS). This includes providing participants with detailed information about the plan, ensuring the plan is adequately funded, and providing fiduciary responsibilities. Economic trends can significantly impact the sustainability and effectiveness of the Unit Benefit Formula. Low-interest rates can increase the cost of providing defined benefits, while increased life expectancy can lead to higher pension costs. Employers and financial planners must consider these factors when designing and managing pension plans using the Unit Benefit Formula. The future may see changes and innovations in the Unit Benefit Formula to adapt to changing economic and demographic trends. These could include adjustments to the percentage factor or the way the average salary is calculated. Innovations could also include the use of technology to help employees better understand their potential benefits and make more informed retirement planning decisions. The Unit Benefit Formula is a significant tool used in calculating retirement benefits within pension plans, based on an employee's years of service and earnings. It provides a predictable and secure retirement income and serves as an effective tool for attracting and retaining employees. However, the complexity of the formula and the potential for high costs to employers are notable downsides. When compared to other pension benefit formulas such as the Flat Benefit Formula, Career Average Formula, and Final Pay Formula, the Unit Benefit Formula often results in higher benefits for those with higher earnings, rewarding long-serving employees. Understanding these complexities and contrasts is vital for both employees and employers in planning for retirement and maintaining a sustainable pension system.Definition and Purpose of the Unit Benefit Formula

The Importance of the Unit Benefit Formula

Understanding the Unit Benefit Formula

Structure and Components of the Unit Benefit Formula

How the Unit Benefit Formula Works

Calculation of the Unit Benefit Formula

Application of the Unit Benefit Formula in Pension Plans

Role of the Unit Benefit Formula in Determining Pension Benefits

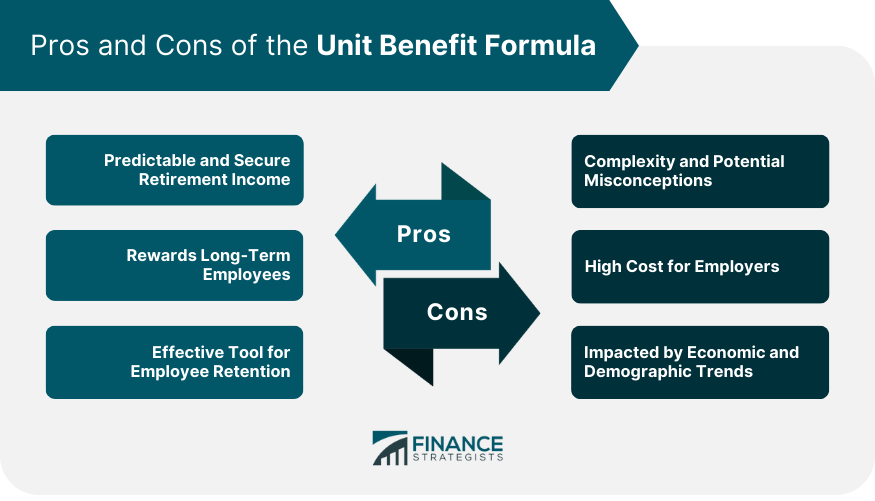

The Pros and Cons of the Unit Benefit Formula

Pros of Using the Unit Benefit Formula

Cons or Limitations of Unit Benefit Formula

Differences Between the Unit Benefit Formula and Other Pension Benefit Formulas

Unit Benefit Formula vs Flat Benefit Formula

Unit Benefit Formula vs Career Average Formula

Unit Benefit Formula vs Final Pay Formula

Legal and Regulatory Aspects of the Unit Benefit Formula

Laws and Regulations Governing the Use of the Unit Benefit Formula

Compliance With Unit Benefit Formula Regulations

Future of the Unit Benefit Formula

Impact of Economic Trends on the Unit Benefit Formula

Potential Changes and Innovations in the Unit Benefit Formula

Conclusion

Unit Benefit Formula FAQs

The Unit Benefit Formula is a method used in pension plans to determine an employee's retirement benefits. It calculates these benefits based on the employee's salary and years of service.

The Unit Benefit Formula works by multiplying a fixed percentage, typically defined in the pension plan, by the average salary and the years of service. The result is the annual pension benefit the employee will receive upon retirement.

The Unit Benefit Formula provides a predictable retirement income and rewards long-term employees. However, it can be complex to understand and potentially costly for employers. It's also influenced by economic and demographic trends.

Unlike other pension formulas such as the Flat Benefit, Career Average, and Final Pay Formulas, the Unit Benefit Formula considers the employee's earnings, providing potentially higher benefits for those with higher salaries.

Yes, the future may see changes and innovations in the Unit Benefit Formula to adapt to changing economic and demographic trends. Adjustments could be made to the percentage factor or the way the average salary is calculated.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.