A small business line of credit without a personal guarantee is a type of financing that allows businesses to borrow up to a certain amount from a lender and then repay it with interest over time but without the need for a personal guarantor. These kinds of lines of credit can be an attractive option for startups and other new companies since they allow access to capital without the need for someone to take on the risk of guaranteeing repayment. In addition to being available without having a personal guarantee, these lines of credit also usually come with higher interest rates than secured options since there is more risk assumed by lenders in offering them. However, they can also be easier to obtain and provide more flexibility when it comes to repayment as borrowers only pay interest on what they use instead of having to pay upfront for an entire lump sum. A small business has distinct characteristics when compared to other types of businesses such as corporations and nonprofits. It typically has fewer resources such as capital and personnel, but relies on the creativity of its owners in order to innovate and remain competitive in the market. The owners of small businesses are often very hands-on and provide direct oversight for every aspect of their operation, from production to marketing. A business line of credit is a type of financing that allows companies to borrow up to a certain amount from a lender and then repay it with interest over time. It can offer flexibility since the borrower only pays interest on the money they actually use, rather than having to pay for a lump sum upfront. As such, it’s an attractive option for businesses looking for short-term working capital or immediate cash needs. The amount available under each line of credit depends on the lender and the individual company’s creditworthiness, but typically ranges from several hundreds to millions of dollars. The terms of repayment also vary depending on the specific agreement, but most business lines of credit require monthly payments at predetermined intervals with interest that accumulates on the unused portion of any unpaid balance. There are two types of lines of credit, secured and unsecured, and they have distinct advantages and drawbacks. A secured business line of credit is backed by collateral, such as equipment, inventory, or real estate, which the lender will take possession of if the loan is not repaid according to the terms agreed upon. This type of loan generally carries lower interest rates since it offers greater security for lenders and faster approval times than unsecured loans because extensive documentation or personal guarantees are unnecessary. On the other hand, an unsecured business line of credit does not require any collateral, but instead relies on the borrower’s creditworthiness in order to secure a loan. Unsecured business lines have higher interest rates as they carry riskier terms than secured loans and may require more paperwork in order to qualify for approval. There are several types of these kinds of loans available to business owners, such as merchant cash advances, business credit cards, and unsecured business lines of credit. These are short-term loans that provide upfront funding for businesses in exchange for a percentage of future revenues. The benefit of this option is that it comes with no fixed repayment schedule, allowing companies to leverage their cash flow more effectively while still meeting obligations to the lender. Business credit cards are another popular choice since they come with higher limits than regular consumer cards and allow companies to gain access to open-ended financing with no collateral required as long as they maintain responsible spending habits. These cards also typically offer rewards such as points or cash back on certain purchases, making them attractive options even beyond their financing capabilities. These may be offered by some lenders in lieu of traditional secured forms that require some form of collateral from borrowers. Although these lines tend to come with higher interest rates due to the additional risk taken by lenders, they can still be attractive options for smaller companies that don’t have assets or guarantors necessary for getting approved for other kinds of loans. Getting a line of credit without a personal guarantee for a small business can be a great way to access extra capital and get more flexibility when it comes to repayment. However, there are several steps involved in securing such financing, and understanding how the process works is key to finding the best terms available. The first step is to assess your financial situation and determine how much money you need. This will help you narrow down your search for lenders since many specialize in specific types of loans and amounts. Additionally, be aware of any potential fees or restrictions that may come with each loan. Once you have identified potential lenders, make sure to review their criteria so you know what type of information they require before approving an application. This includes documents such as business plans, financial statements, tax returns, etc., which are standard requirements when applying for any kind of loan. When considering different offers from different lenders, look closely at all aspects, including interest rates and repayment terms, as these can have a major impact on your long-term costs. Also, check if the lender requires any payment guarantors or allows borrowing against future revenue streams so you can choose the option that best fits your needs. Finally, compare all available options once again and select the one that best suits your business’s current financial situation, so you can get the most out of your line of credit without having to worry about personal guarantees. In order to maximize the chances of success and maintain financial security, entrepreneurs should take the time to investigate all available options and weigh every factor involved. First of all, it is essential to find the right credit card provider that fits your business needs and provides clear terms. Ask yourself questions such as: Is this the best rate offered? Are there any annual fees, balance transfer fees, or other hidden costs? Are the rewards worth what I'll be paying annually? To further reduce costs, some providers offer promotional rates for introductory periods or even waive certain fees for qualified customers. Another critical aspect you must evaluate is the annual percentage rate (APR). You want to ensure that you're getting a competitive interest rate that won't break your budget over time. Likewise, it’s important to pay attention to any restrictions, such as late-payment penalties and long-term repayment plans. The last thing you want is to face steep financial penalties due to missed payments. You also need to research and read up on customer reviews from trusted websites so that you can select a product with a proven track record of satisfaction among customers. Finally, make sure to double-check the fine print of your chosen card before submitting an application. That way, you can avoid potential surprises down the line – such as another personal guarantee requirement – when it comes time to make payments or redeem rewards points. Taking out a small business line of credit without a personal guarantee is an effective way to finance your business without the risk associated with such guarantees. To ensure you find the best offer for your business, it is crucial to explore different lenders and their offerings, familiarize yourself with the terms and conditions of each card, and compare interest rates between cards. With these considerations in mind and a financial advisor as guide, you can be sure to get the best deal that meets your needs.What Is a Small Business Line of Credit Without a Personal Guarantee?

Defining Small Businesses

What Is a Business Line of Credit?

Types of Small Business Lines of Credit Without a Personal Guarantee

Merchant Cash Advances

Business Credit Cards

Unsecured Business Lines of Credit

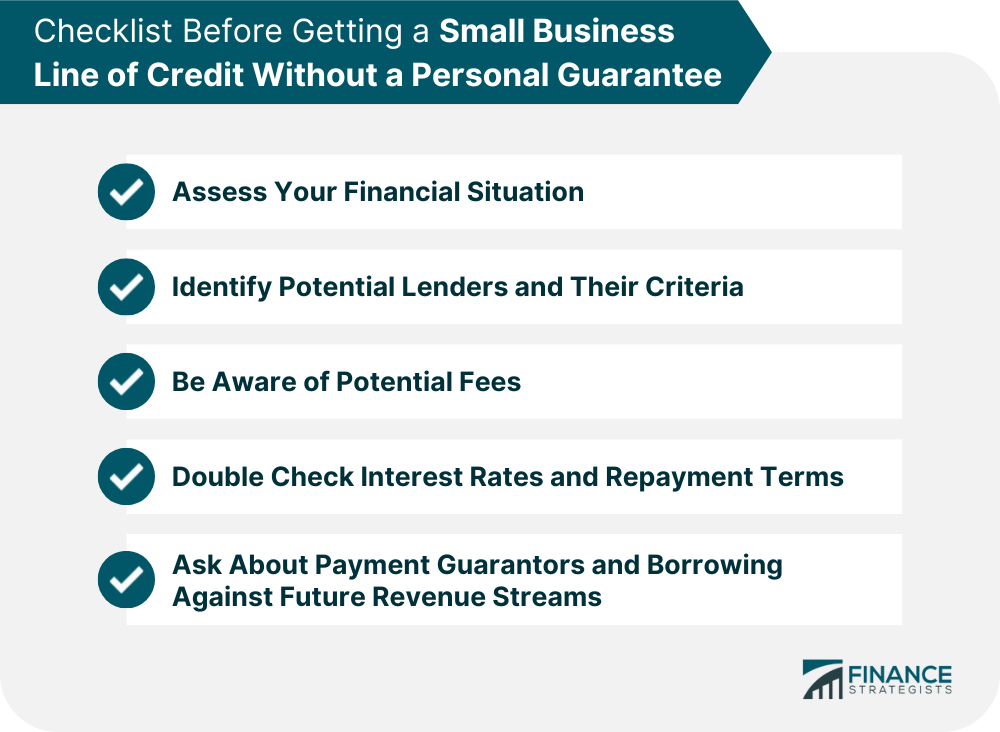

How to Get a Small Business Line of Credit Without a Personal Guarantee

Things to Consider When Applying for a Small Business Credit Card Without a Personal Guarantee

The Bottom Line

Small Business Line of Credit Without a Personal Guarantee FAQs

A small business line of credit without a personal guarantee is an alternative form of financing for businesses that do not include the requirement for the owner to sign on as personally liable for any debt associated with the loan.

In order to be eligible for a small business line of credit without a personal guarantee, the borrower must have a good credit score and their business must meet certain criteria. These requirements may vary by lender.

A small business line of credit without a personal guarantee is usually secured by assets such as accounts receivable, inventory, or equipment.

The fees associated with a small business line of credit without a personal guarantee will depend on the lender and the terms of the loan. Generally, there may be an origination fee, annual fee, and/or closing costs associated with the loan.

To apply for this type of loan, you will need to submit an online application or contact a lender directly. The application process can vary by lender, so it is important to review the requirements of each lender before applying.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.