An unsecured line of credit is a type of loan that doesn't require any collateral from the borrower, meaning the lender assumes a higher degree of risk. The rates associated with this form of borrowing, known as an unsecured line of credit rates, refer to the interest charged on the outstanding balance of the line of credit. These rates fluctuate based on various factors, including the borrower's creditworthiness, market conditions, and lender policies. An unsecured line of credit rate is typically higher than rates for secured lines of credit due to the increased risk for the lender. In case of a default, the lender may have limited recourse to recover their funds. A fixed interest rate remains constant throughout the life of the loan. This means the borrower knows exactly how much interest will be charged on the borrowed amount for the entirety of the loan. Fixed rates are beneficial in a rising interest rate environment, as they shield borrowers from increasing borrowing costs. However, fixed rates also have their downside. If market rates fall below the fixed rate, borrowers are stuck paying a higher rate of interest. Moreover, lenders often set fixed rates higher than the current market rate to account for potential future rate increases. Unlike fixed rates, variable interest rates change over time, typically in line with a reference interest rate like the Prime Rate or the London Interbank Offered Rate (LIBOR). If these reference rates increase, the variable rate will also increase, resulting in higher interest charges for the borrower. Conversely, if reference rates decrease, so will the variable rate. Variable rates offer potential savings in a declining interest rate environment. However, they also introduce uncertainty and potential budgeting challenges, as the cost of borrowing can fluctuate over the life of the line of credit. They are directly tied to the Prime Rate, which is the interest rate that commercial banks offer to their most creditworthy customers. Prime-based rates are often expressed as a certain percentage above or below the Prime Rate. When the Prime Rate changes, so does the interest rate on a Prime-based line of credit. This type of rate allows borrowers to potentially benefit from decreases in the Prime Rate, but it also exposes them to risk if the Prime Rate increases. Introductory rates, often known as teaser rates, are lower interest rates offered for a specified period at the start of a line of credit. After the introductory period, the rate usually increases to the standard rate as defined in the loan agreement. Introductory rates can make an unsecured line of credit more affordable initially. However, it's important for borrowers to understand what the standard rate will be and whether they can afford the loan once the introductory period ends. Credit scores are numerical representations of an individual's creditworthiness, and they play a significant role in determining unsecured line of credit rates. Lenders use credit scores to evaluate the risk associated with lending money to a potential borrower. A high credit score signals to lenders that a borrower is less risky, which may result in a lower interest rate. Conversely, a lower credit score could lead to higher rates or even denial of the loan application. Lenders consider the borrower's income and overall financial stability when determining unsecured line of credit rates. Steady income and financial stability suggest a borrower has the capacity to repay the loan, potentially leading to a lower interest rate. If a borrower's income is irregular or if they have recently changed jobs, lenders might perceive them as a higher risk. This could result in a higher interest rate or, in some cases, a refusal to extend credit. Though unsecured lines of credit don't require collateral, lenders may still consider the borrower's overall financial picture, including their loan-to-value (LTV) ratio on other outstanding loans. LTV is the ratio of a loan to the value of the asset purchased with the loan. A high LTV ratio on other loans might indicate that a borrower is overextended, which could lead to a higher interest rate on the unsecured line of credit. Conversely, a lower LTV ratio could signal financial responsibility, possibly resulting in a lower rate. The size of the line of credit and the repayment terms can also impact the interest rate. Typically, larger loans carry a higher risk for the lender and may come with higher interest rates. Longer repayment terms can also lead to higher rates because the lender's money is at risk for a longer period. Conversely, smaller loans and shorter repayment terms can lead to lower rates, provided the borrower's credit profile supports this. The borrower's creditworthiness is one of the most significant factors influencing unsecured line of credit rates. Creditworthiness is a measure of how likely a person is to repay a loan. It's assessed based on credit history, current financial situation, and future income potential. Lenders reward creditworthy borrowers with lower interest rates because they pose less risk of defaulting on the loan. On the other hand, borrowers with poor creditworthiness may face higher interest rates or may not be eligible for an unsecured line of credit at all. When the economy is strong, and default rates are low, lenders may lower their rates to attract borrowers. Conversely, in a weak economy or during a period of high default rates, lenders may raise rates to offset increased risk. Furthermore, rates are influenced by monetary policy set by central banks. When central banks raise benchmark rates, borrowing costs for lenders increase, and these costs are often passed on to the consumer in the form of higher rates. The level of competition among lenders in the market also influences unsecured line of credit rates. In a competitive market, lenders may lower rates to attract borrowers. However, in less competitive markets, borrowers may have fewer options, giving lenders the ability to charge higher rates. Furthermore, some lenders may differentiate themselves by offering lines of credit to borrowers with lower credit scores, but these products usually come with higher rates due to increased risk. Different financial institutions have different policies when it comes to setting rates on unsecured lines of credit. These policies are often shaped by factors such as the institution's risk tolerance, strategic focus, and capital availability. For example, a bank with a high-risk tolerance might offer unsecured lines of credit at lower rates to attract a larger customer base. In contrast, a bank with a lower risk tolerance might offer higher rates to offset potential defaults. An unsecured line of credit offers the flexibility to borrow as much or as little as needed, up to the credit limit. This makes it an attractive option for people who need access to funds but aren't sure exactly how much they'll need. As long as the credit limit isn't exceeded, the borrower can draw on the line of credit at their discretion. This means that borrowers don't have to risk losing a valuable asset like a home or car if they default on the loan. This lack of collateral makes unsecured lines of credit particularly appealing to borrowers who don't own many assets. Depending on the borrower's creditworthiness and other factors, unsecured line of credit rates can be lower than rates on other types of high-risk loans, such as payday loans. However, these rates will typically be higher than those for secured loans. Unsecured lines of credit usually come with higher interest rates compared to secured loans, as the lender takes on more risk without any collateral to recover in case of default. These higher rates can make an unsecured line of credit more expensive over the life of the loan. Due to the increased risk, lenders may limit the amount of money they're willing to lend on an unsecured basis. This means borrowers may not be able to obtain as large a line of credit as they could with a secured loan. The flexibility and ease of access to funds that come with an unsecured line of credit can lead to overspending. If not managed carefully, it can result in high levels of debt and potentially damage the borrower's credit score. A good credit score is one of the most effective ways to secure a favorable rate on an unsecured line of credit. Regularly monitoring your credit report, making timely payments, keeping your credit utilization low, and avoiding unnecessary debt can help maintain or improve your credit score. Lenders look at income and financial stability when determining rates. Demonstrating consistent income, maintaining a stable job, and keeping a low debt-to-income ratio can improve your chances of getting a lower rate. Interest rates can vary significantly between lenders, so it's important to shop around and compare offers. Look beyond just the interest rate and consider other factors like fees, terms, and repayment options to find the best overall loan for your needs. While rates for unsecured lines of credit are largely based on market conditions and personal financial factors, there may still be some room for negotiation. If you have a strong credit profile or a long-standing relationship with a lender, you might be able to negotiate a lower rate. Unsecured line of credit rates are interest rates applied to the outstanding balance of a line of credit that doesn't require any collateral. These rates can be fixed, variable, prime-based, or introductory, and they're determined based on factors like credit score, income, financial stability, and loan amount and repayment terms. Unsecured line of credit rates are influenced by various factors, such as creditworthiness, economic conditions, market competition, and financial institution policies. They offer borrowing flexibility, require no collateral, and may have lower interest rates. However, these benefits come with certain drawbacks, including higher interest rates compared to secured loans, and the risk of overspending and accumulating debt. To secure favorable unsecured line of credit rates, maintaining a good credit score, improving financial stability, comparing offers, and negotiating terms with financial institutions can be helpful strategies.What Are Unsecured Line of Credit Rates?

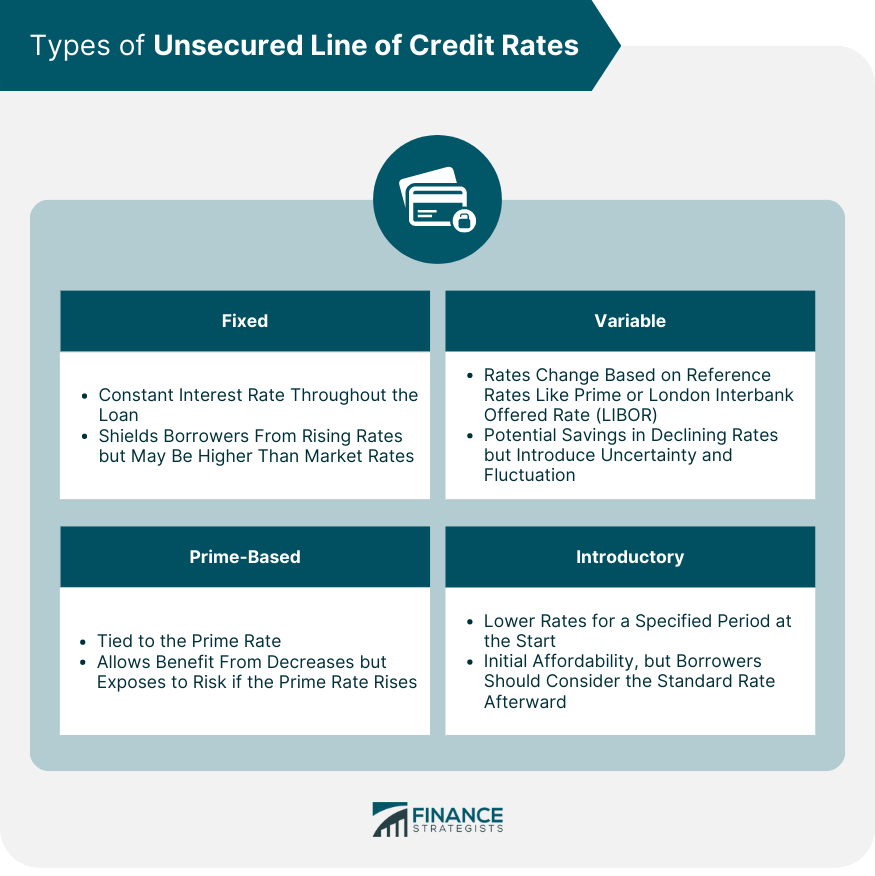

Types of Unsecured Line of Credit Rates

Fixed Interest Rates

Variable Interest Rates

Prime-Based Rates

Introductory Rates

Determining Unsecured Line of Credit Rates

Credit Score Assessment

Evaluation of Income and Financial Stability

Loan-To-Value Ratio Consideration

Loan Amount and Repayment Terms

Factors Influencing Unsecured Line of Credit Rates

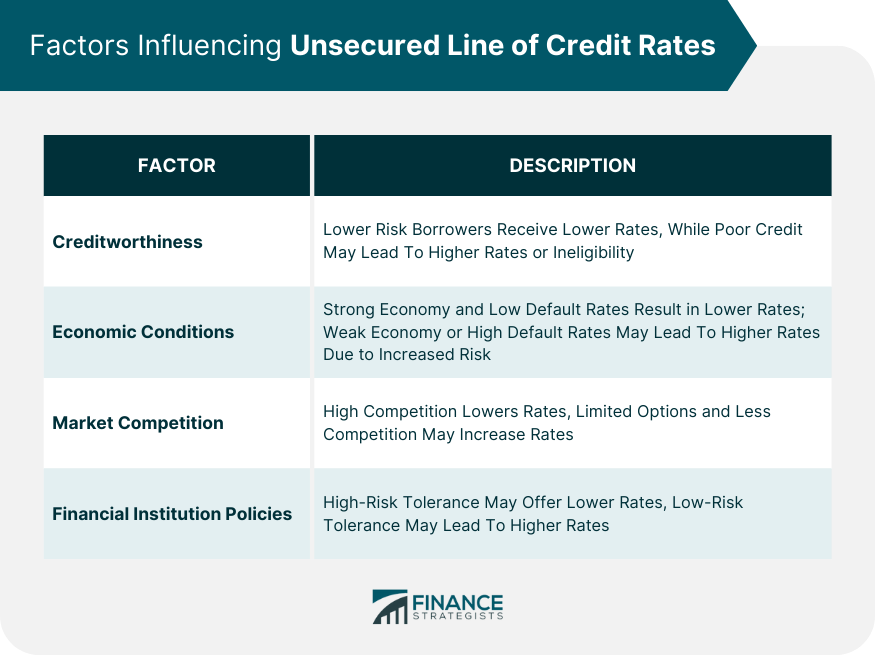

Creditworthiness of the Borrower

Economic Conditions

Market Competition

Financial Institution Policies

Advantages of Unsecured Line of Credit Rates

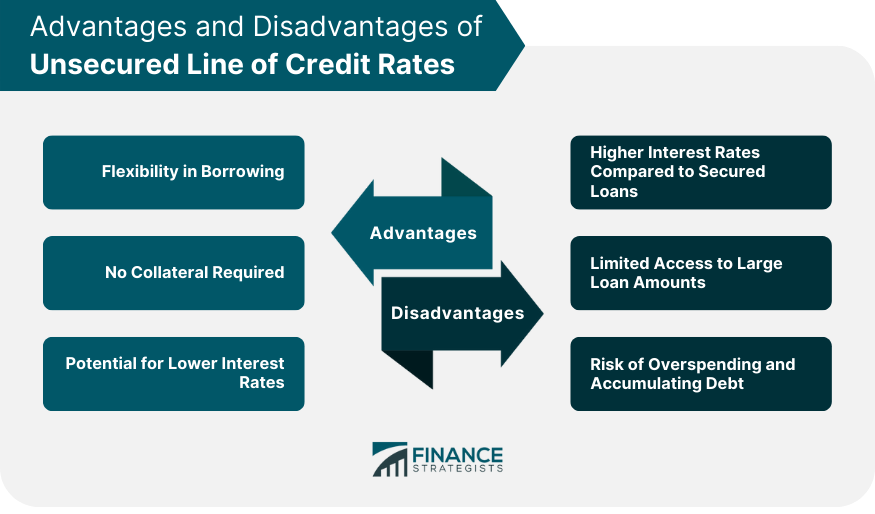

Flexibility in Borrowing

No Collateral Required

Potential for Lower Interest Rates

Disadvantages of Unsecured Line of Credit Rates

Higher Interest Rates Compared to Secured Loans

Limited Access to Large Loan Amounts

Risk of Overspending and Accumulating Debt

Tips for Favorable Unsecured Line of Credit Rates

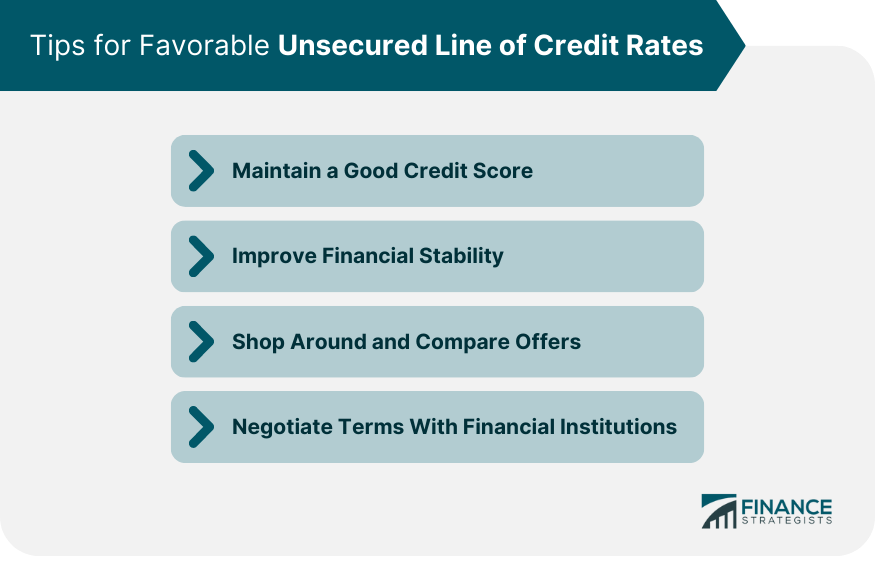

Maintain a Good Credit Score

Improve Financial Stability

Shop Around and Compare Offers

Negotiate Terms With Financial Institutions

Conclusion

Unsecured Line of Credit Rates FAQs

An unsecured line of credit is a type of loan that doesn't require any collateral. The lender provides the borrower with a maximum credit limit, and the borrower can borrow up to that limit as needed.

The interest rate for an unsecured line of credit is determined based on several factors, including the borrower's credit score, income and financial stability, loan amount and repayment terms, as well as market conditions and lender policies.

Benefits of an unsecured line of credit include flexibility in borrowing, no need for collateral, and potentially lower interest rates compared to other high-risk loans.

Drawbacks include higher interest rates compared to secured loans, limited access to large loan amounts, and the risk of overspending and accumulating debt.

To get a better interest rate, maintain a good credit score, demonstrate financial stability, shop around and compare offers, and negotiate terms with lenders.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.