Medicare is a federal health insurance program designed for individuals aged 65 and older, as well as certain younger individuals with disabilities. It consists of several parts, each providing different types of coverage. Medicare Late Enrollment Penalties refer to the additional costs that a Medicare beneficiary may have to pay if they do not enroll in Medicare during their Initial Enrollment Period or when they are first eligible for a specific type of coverage. These penalties are designed to encourage individuals to enroll in Medicare when they are first eligible and to discourage individuals from delaying enrollment until they need healthcare services. Part A covers inpatient hospital care, skilled nursing facilities, hospice, and some home health care services. Part B covers outpatient services, including doctor visits, preventive services, and medical equipment. Part D covers prescription drug coverage. Timely enrollment in Medicare is crucial to avoid late enrollment penalties. It ensures access to essential health care services and can help minimize out-of-pocket costs. Enrolling during the Initial Enrollment Period (IEP) or a Special Enrollment Period (SEP) allows beneficiaries to avoid penalties. Missing these windows can result in higher premiums and limited enrollment opportunities. The penalty for late enrollment in Medicare Part A is calculated based on the number of months a beneficiary is late. For every 12 months of delay, the penalty is 10% of the standard premium. This penalty applies to individuals who are not eligible for premium-free Part A coverage, which is usually available to those with a sufficient work history. The Part A late enrollment penalty lasts twice the number of years a beneficiary was late in enrolling. This means that if a beneficiary was two years late in enrolling, they would pay the penalty for four years. Once the penalty period ends, the individual will pay the standard Part A premium without the added penalty. To avoid the Part A penalty, individuals who are not eligible for premium-free Part A should enroll during their Initial Enrollment Period. If they do not enroll during this period, they may have to pay a higher premium for Part A when they do enroll. The Medicare Part B late enrollment penalty is calculated as 10% of the standard Part B premium for each full 12-month period the beneficiary is late. This percentage is added to the beneficiary's monthly premium. For example, if the standard premium is $150 and the beneficiary is two years late, the penalty would be $30, resulting in a total premium of $180. Unlike Part A, the Part B late enrollment penalty lasts for the duration of the beneficiary's enrollment in Part B. This means the penalty will be applied to the monthly premium for as long as the beneficiary remains in the program. It is crucial to enroll in Part B on time to avoid this lifelong penalty. To avoid the Part B penalty, individuals should enroll in Part B during their Initial Enrollment Period. If they do not enroll during this period, they may have to pay a higher premium for Part B when they do enroll. The Medicare Part D late enrollment penalty is calculated by multiplying 1% of the "national base beneficiary premium" by the number of full, uncovered months the beneficiary did not have creditable prescription drug coverage. The penalty amount is then rounded to the nearest 10 cents and added to the monthly premium. Similar to Part B, the Part D late enrollment penalty is applied for as long as the beneficiary is enrolled in a Part D plan. The penalty may change each year, as the national base beneficiary premium may be adjusted annually. It is essential to maintain continuous creditable drug coverage to avoid this penalty. To avoid the Part D penalty, individuals should enroll in a Medicare prescription drug plan during their Initial Enrollment Period. If they do not enroll during this period, they may have to pay a higher premium for Part D when they do enroll. Special Enrollment Periods allow beneficiaries to enroll in Medicare without incurring late enrollment penalties. SEPs may be triggered by certain life events, such as loss of employer coverage, moving to a new service area, or qualifying for Medicaid. Enrolling during an SEP can help avoid penalties and ensure access to necessary health care coverage. Medicare Advantage (Part C) plans are an alternative to Original Medicare, offering coverage for Parts A and B, and often Part D. Enrollment in a Medicare Advantage plan with prescription drug coverage can help beneficiaries avoid late enrollment penalties for Part D. These plans are provided by private insurers and may offer additional benefits, such as dental, vision, and wellness programs. Individuals with employer-sponsored health insurance or COBRA coverage may delay enrollment in Medicare without incurring penalties, as long as they maintain continuous coverage. Once the employer coverage or COBRA ends, beneficiaries have an eight-month Special Enrollment Period to enroll in Medicare Parts A and B without incurring penalties. Late enrollment penalties result in higher monthly premiums for Medicare Parts A, B, and D. These additional costs can strain the budgets of beneficiaries, particularly those on fixed incomes. Enrolling on time can help avoid these increased costs and make Medicare coverage more affordable. Missing the Initial Enrollment Period or a Special Enrollment Period can limit the opportunities for beneficiaries to enroll in Medicare. Late enrollment may only be possible during the General Enrollment Period, which runs from January 1 to March 31 each year. This limited window can result in delays in accessing necessary health care services. Enrolling in Medicare during the General Enrollment Period can result in delayed coverage. Coverage typically begins on July 1 of the year in which the beneficiary enrolls. This delay can leave individuals without adequate health care coverage for several months, potentially leading to negative health outcomes. Being aware of Medicare enrollment deadlines, such as the Initial Enrollment Period and Special Enrollment Periods, is essential for avoiding penalties. Beneficiaries should research their eligibility and enrollment windows to ensure they do not miss crucial deadlines. Educating oneself about the Medicare program can help prevent costly mistakes. Each individual's health care needs are unique. Beneficiaries should carefully assess their health status and anticipated future needs when choosing a Medicare plan. Selecting the appropriate coverage, including Part D prescription drug coverage or a Medicare Advantage plan, can help avoid penalties and ensure access to necessary health care services. Various resources and assistance programs are available to help beneficiaries navigate the Medicare enrollment process. State Health Insurance Assistance Programs (SHIPs), the Social Security Administration, and the Medicare website offer valuable information and guidance. Taking advantage of these resources can help beneficiaries make informed decisions and avoid late enrollment penalties. Medicare Late Enrollment Penalties are additional costs that a Medicare beneficiary may have to pay if they do not enroll in Medicare during their Initial Enrollment Period or when they are first eligible for a specific type of coverage. The penalties for late enrollment in Medicare Parts A, B, and D are designed to encourage individuals to enroll in Medicare when they are first eligible and to discourage individuals from delaying enrollment until they need healthcare services. It is crucial to enroll in Medicare on time to avoid late enrollment penalties, as they result in higher monthly premiums and can limit the opportunities for beneficiaries to enroll in Medicare. Strategies to minimize late enrollment penalties include understanding enrollment deadlines, evaluating personal health needs, and utilizing available resources and assistance. By taking advantage of these strategies, beneficiaries can avoid penalties, ensure access to necessary health care services, and make Medicare coverage more affordable.Definition of Medicare Late Enrollment Penalties

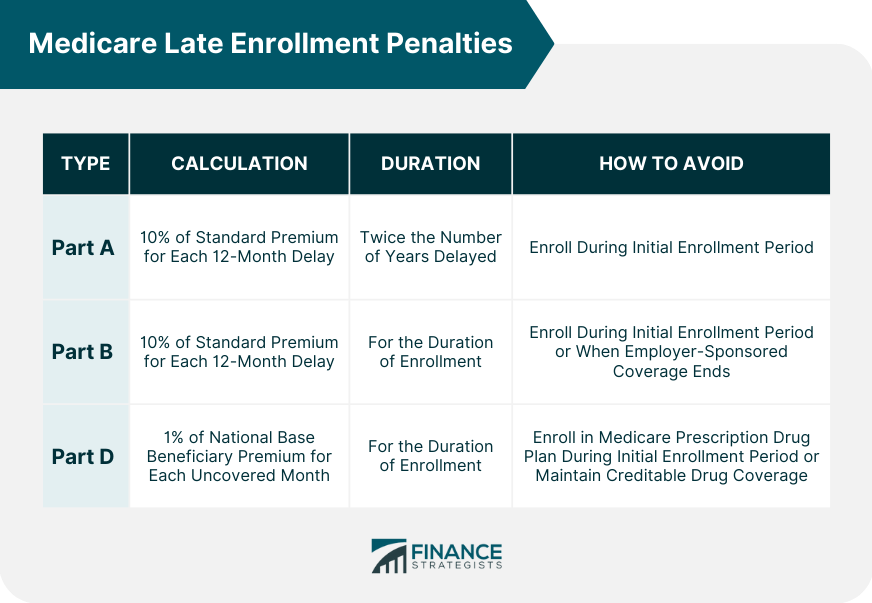

Medicare Part A Late Enrollment Penalties

Calculation of Part A Penalty

Duration of Part A Penalty

Avoiding Part A Penalty

Medicare Part B Late Enrollment Penalties

Calculation of Part B Penalty

Duration of Part B Penalty

Avoiding Part B Penalty

Additionally, individuals who do not have employer-sponsored health coverage and do not enroll in Part B when they are first eligible may have to pay a penalty for every year they delay enrollment.Medicare Part D Late Enrollment Penalties

Calculation of Part D Penalty

Duration of Part D Penalty

Avoiding Part D Penalty

It is important to note that the penalty for late enrollment in Part D is based on the number of months an individual went without Part D coverage or other creditable prescription drug coverage.

Factors Affecting Medicare Late Enrollment Penalties

Special Enrollment Periods

Medicare Advantage Plans

Employer Coverage and COBRA

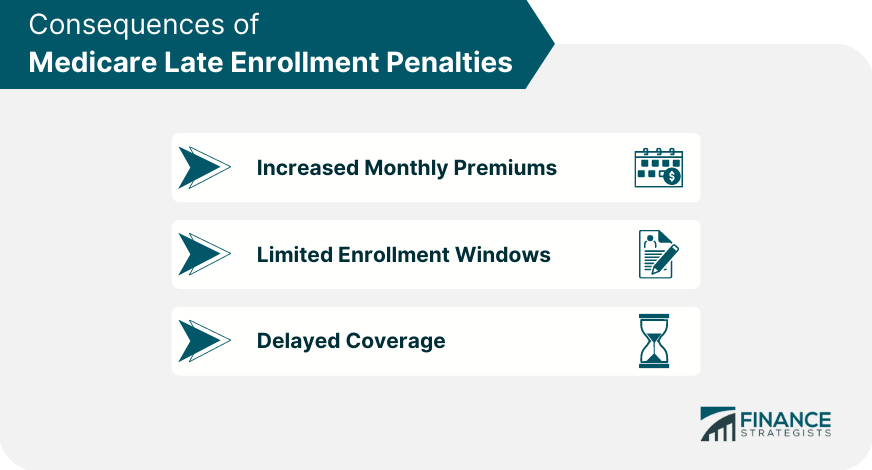

Consequences of Medicare Late Enrollment Penalties

Increased Monthly Premiums

Limited Enrollment Windows

Delayed Coverage

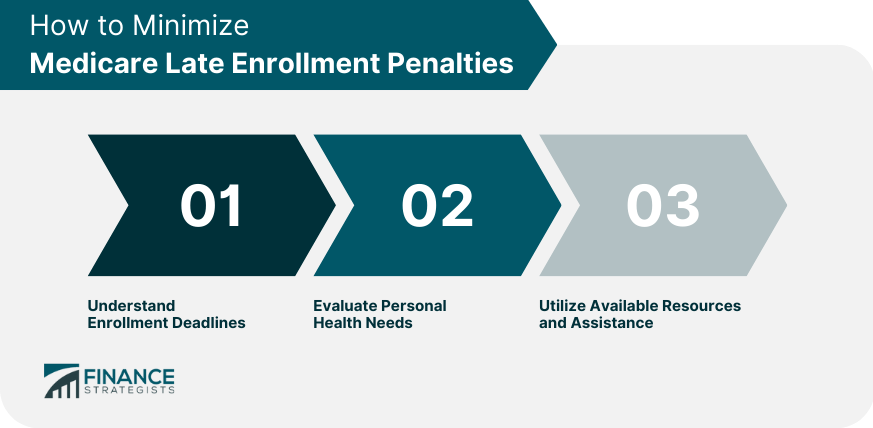

Strategies to Minimize Medicare Late Enrollment Penalties

Understand Enrollment Deadlines

Evaluate Personal Health Needs

Utilize Available Resources and Assistance

Final Thoughts

Medicare Late Enrollment Penalties FAQs

A Medicare late enrollment penalty is a fee imposed on individuals who do not sign up for Medicare Part A or Part B when they are first eligible.

The Medicare late enrollment penalty is calculated by multiplying 1% of the monthly Part B premium by the number of full, uncovered months that the individual was eligible but did not enroll.

Yes, you can avoid a Medicare late enrollment penalty by signing up for Medicare Part A and/or Part B during your Initial Enrollment Period (IEP) or Special Enrollment Period (SEP).

The Medicare late enrollment penalty is permanent and will be added to your monthly Part B premium for as long as you have Medicare.

If you cannot afford the monthly premium due to a Medicare late enrollment penalty, you may be eligible for assistance through the Medicare Savings Programs, which provide financial assistance for Medicare premiums and other costs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.