Annuity payout options determine how and when the funds invested in an annuity contract are paid out to the annuity holder. An annuity is a financial product that pays out a series of income payments over time, typically used as a retirement income source or strategy. When you purchase an annuity, you can choose from several payout options that determine how and when you'll receive income from the annuity. Understanding annuity payout options is crucial for individuals planning for retirement, as these options can significantly impact the level of income received and the financial security during the retirement years. There are different types of annuity payout options available. These include: A life annuity provides a steady stream of income for the remainder of the annuitant's life. A single-life annuity provides payments to one individual, ending upon their death. This option typically offers the highest payout amount, but the payments cease after the annuitant's death, leaving no benefits for a surviving spouse or beneficiary. A joint life annuity covers two individuals, usually spouses, and continues to provide payments until both annuitants have passed away. The payout amounts are generally lower than a single life annuity, but the payments continue for longer, providing ongoing income for the surviving annuitant. A life annuity with period certain guarantees income payments for a specific period in addition to the lifetime income. This option provides income for the annuitant's lifetime and guarantees payments for a specified period, even if the annuitant dies before the end of that period. In such cases, the remaining payments are made to the beneficiary. Similar to the single-life version, this option provides lifetime income for two individuals and guarantees payments for a specified period. If both annuitants pass away before the end of the period, the remaining payments are made to the beneficiary. A fixed-period annuity provides income payments for a specified number of years, irrespective of the annuitant's lifespan. After the period ends, the payments cease. A fixed amount annuity pays a predetermined amount each month until the annuity's value is depleted. The duration of payments depends on the initial investment and the chosen monthly payout amount. A lump sum annuity payout option provides the annuitant with the entire value of the annuity in a single payment rather than a series of periodic payments. A systematic withdrawal plan allows the annuitant to withdraw a fixed amount or a percentage of the annuity's value periodically, providing flexibility in managing income and investment. Annuity payout options can vary based on several factors that affect the amount of money an individual will receive from their annuity. The following are some factors that affect annuity payout options: The age of the annuitant at the start of payouts affects the amount received. Generally, older individuals receive higher payments since they are expected to have a shorter life expectancy than younger individuals. Women tend to live longer than men, which can result in lower annuity payout amounts for women. The insurance company takes into account gender and mortality rates when calculating annuity payouts. Annuity payouts are affected by interest rates. Higher interest rates lead to higher annuity payout amounts because the insurance company can earn more from investing the annuity's funds. The specific terms and features of the annuity contract can impact the payout amounts. For example, annuities with cost-of-living adjustments or return of premium guarantees may have lower initial payout amounts but may provide more significant benefits over time. The amount of money invested in an annuity also affects the payout amount. Generally, a larger initial investment results in higher annuity payouts. It is crucial to consider these factors when choosing an annuity payout option. An annuity can be an essential tool for retirement planning, and understanding the different payout options can help individuals make informed decisions about their financial future. Annuity payouts are a popular financial product for retirement planning. However, it is essential to understand the tax implications of annuity payouts to avoid any surprises during tax season. The following are some tax-related considerations when it comes to annuity payout options: Annuity payouts are generally subject to federal income tax on the earnings portion of the payments. The principal portion of the payments is considered a return on the original investment and is not taxable. Therefore, the amount of tax owed on annuity payouts depends on the type of annuity and the payout option selected. Qualified annuities are funded with pre-tax dollars, such as those in an employer-sponsored retirement plan. Qualified annuities are subject to income tax on the entire payment amount. Non-qualified annuities, unlike qualified annuities, are funded with after-tax dollars, such as from a personal investment account. Only the earnings portion of the payments is subject to income tax. Some annuity payout options allow for a lump-sum payment instead of regular payments. In the case of lump-sum payouts, the entire earnings portion is taxable in the year the distribution occurs. This can result in a higher tax liability, so planning is crucial. To minimize tax liability on annuity payouts, annuitants can consider spreading the income over several years. This can be done by selecting a payout option that provides regular payments over a set period. Another strategy is to opt for a systematic withdrawal plan, where the annuitant takes out a set amount each year. Additionally, selecting a tax-deferred annuity that allows earnings to grow tax-free until withdrawn can also help minimize tax liability. While annuities can be a valuable tool for retirement planning, it's crucial to consider the potential risks and limitations of annuity payout options. The following are some risks and considerations that individuals should keep in mind when selecting an annuity payout option: Inflation can erode the purchasing power of annuity payments over time. Annuities with cost-of-living adjustment features can help mitigate this risk by adjusting the payment amount to keep up with inflation. Longevity risk refers to the possibility of outliving one's retirement savings. Annuities that provide lifetime income, such as life annuities, can help manage this risk by providing a guaranteed income for life. The performance of the underlying investments can impact the annuity's value and payouts, especially in the case of variable annuities. Individuals should consider their risk tolerance and investment goals when selecting an annuity payout option. Counterparty risk is the risk that the insurance company issuing the annuity may become insolvent or unable to fulfill its obligations. To minimize this risk, individuals should choose a financially stable insurance company with a strong credit rating. Annuities often have limited liquidity, with surrender charges or penalties for early withdrawals. This can make it difficult to access the funds in case of emergencies or unforeseen expenses. Individuals should consider their liquidity needs and ensure they have other sources of liquid assets to cover unexpected expenses. To choose the right annuity payout option, individuals should keep the following factors in mind: Annuity payout options should be chosen based on individual financial needs, goals, and risk tolerance. Factors such as retirement income requirements, health, and life expectancy should be considered to determine the most suitable annuity payout option. Choosing an annuity provider with strong financial ratings is crucial to minimize counterparty risk. Financial strength ratings from reputable agencies such as Standard & Poor's, Moody's, or AM Best can be useful in evaluating the financial stability of an insurance company. A financial advisor can provide personalized guidance on choosing the most suitable annuity payout option based on an individual's financial situation and goals. They can help evaluate the pros and cons of different options and suggest strategies to manage risks. Before making a decision, annuitants should compare various annuity payout options. Factors to consider include payout amounts, guarantees, and contract features such as cost-of-living adjustments or return of premium guarantees. Annuities can be a valuable addition to an investment portfolio, but it's essential to maintain and build a balanced investment mix. To achieve this, annuitants should consider diversifying their investments and incorporating a mix of different financial products, including annuities, stocks, bonds, and other assets. Understanding annuity payout options is crucial for individuals planning for retirement, as the chosen option significantly impacts the income received and overall financial security during retirement years. Various annuity payout options are available, each with its benefits and risks, including life annuities, fixed period annuities, fixed amount annuities, lump sum payouts, and systematic withdrawal plans. Factors affecting annuity payouts include the annuitant's age, gender, interest rates, annuity contract features, and initial investment amount. Taxation of annuity payouts depends on whether the annuity is qualified or non-qualified and the type of payout option chosen. To choose the right annuity payout option, individuals should assess their financial needs and goals, consult a financial advisor, and consider diversification and portfolio balance. To ensure you make informed decisions, seek the expertise of an insurance broker who can guide you through the process and help you find the best insurance solutions tailored to your unique financial situation.What Are Annuity Payout Options?

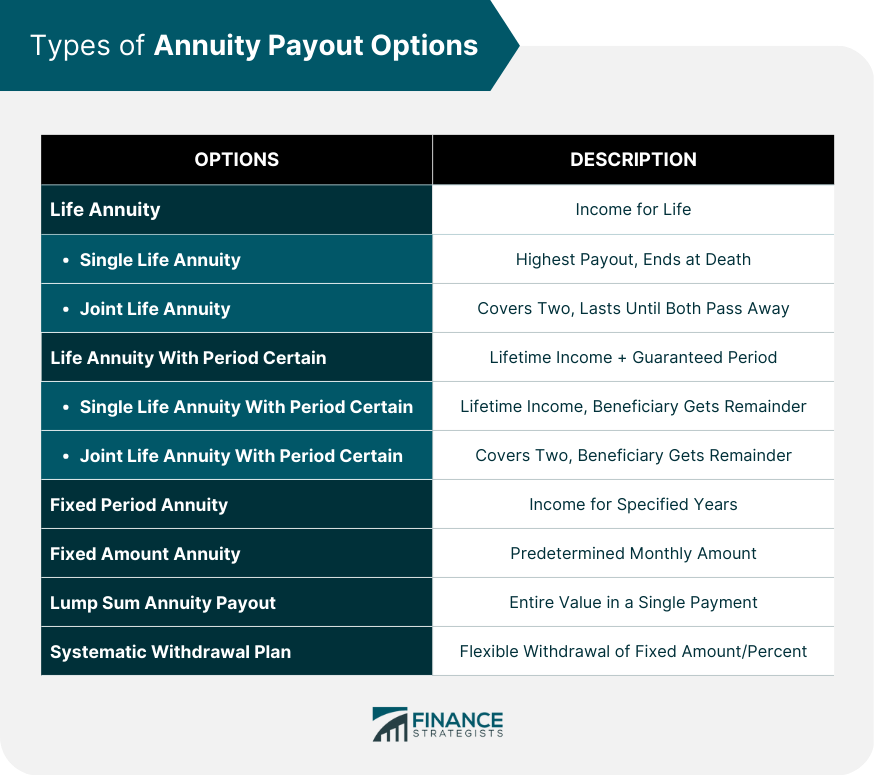

Types of Annuity Payout Options

Life Annuity

Single-Life Annuity

Joint Life Annuity

Life Annuity With Period Certain

Single Life Annuity With Period Certain

Joint Life Annuity With Period Certain

Fixed Period Annuity

Fixed Amount Annuity

Lump Sum Annuity Payout

Systematic Withdrawal Plan

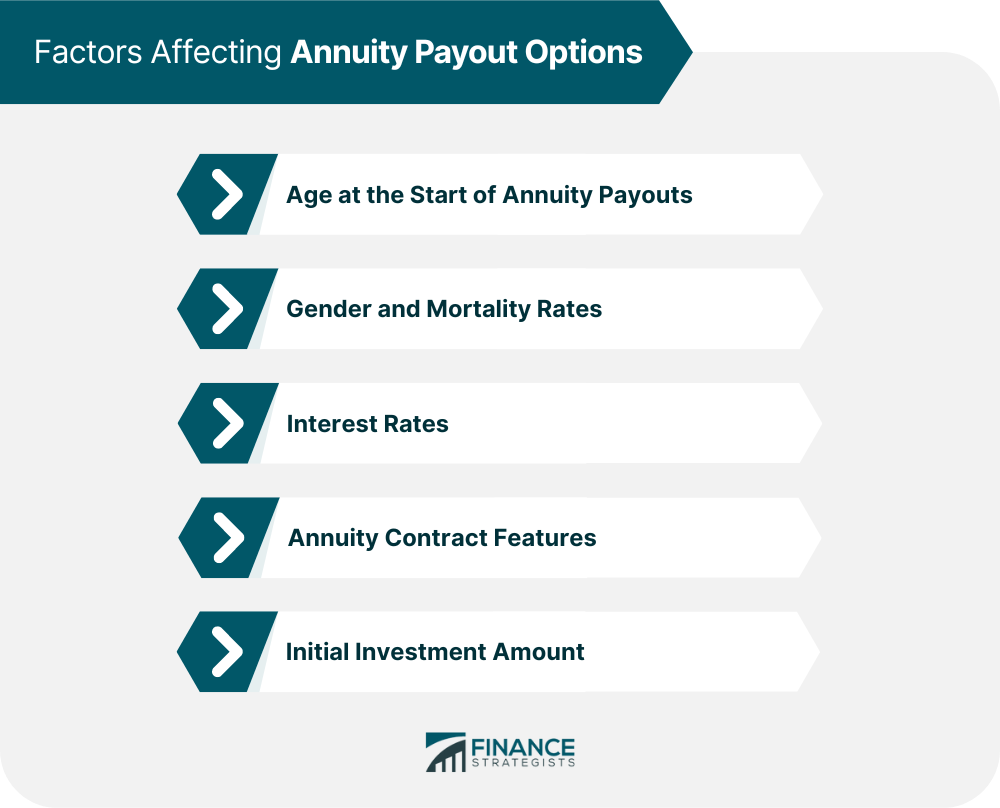

Factors Affecting Annuity Payout Options

Age at the Start of Annuity Payouts

Gender and Mortality Rates

Interest Rates

Annuity Contract Features

Initial Investment Amount

Annuity Payout Options and Taxation

Tax Treatment of Annuity Payouts

Qualified vs Non-qualified Annuities

Taxation of Lump Sum Annuity Payouts

Strategies to Minimize Tax Liability

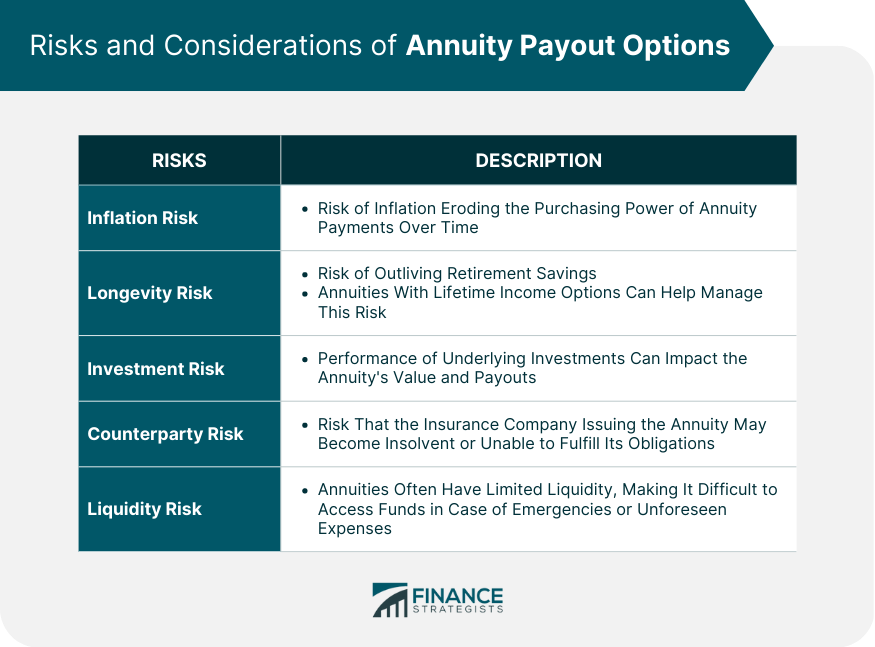

Annuity Payout Options: Risks and Considerations

Inflation Risk

Longevity Risk

Investment Risk

Counterparty Risk

Liquidity Risk

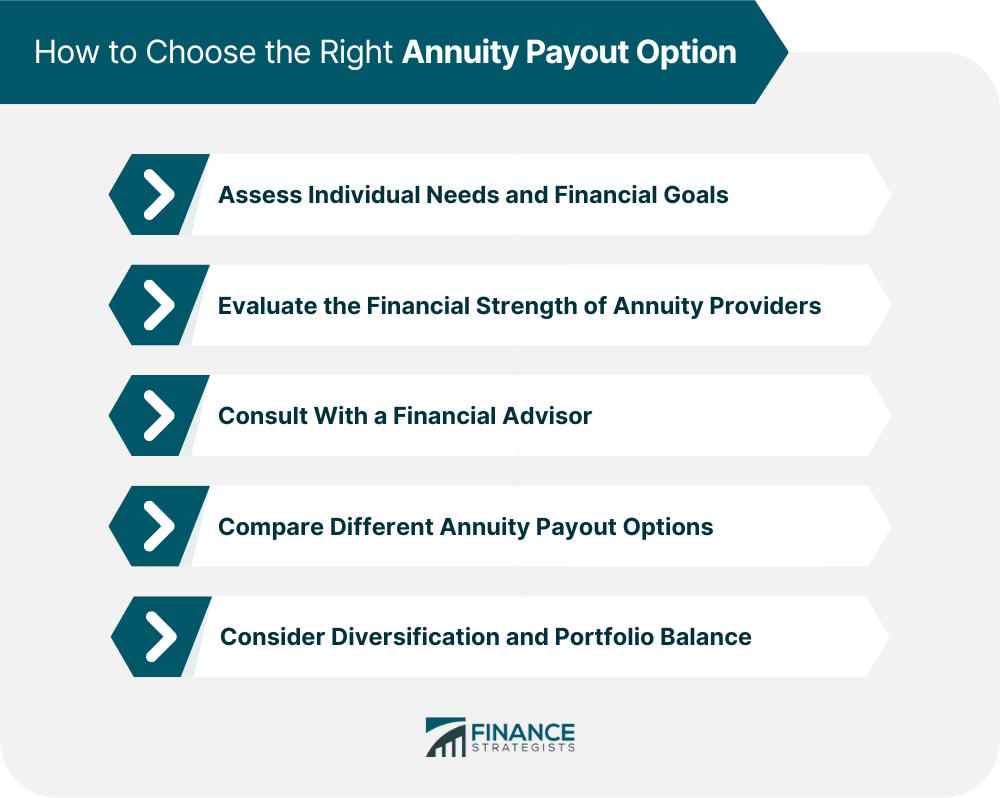

Choosing the Right Annuity Payout Option

Assessing Individual Needs and Financial Goals

Evaluating the Financial Strength of Annuity Providers

Consulting With a Financial Advisor

Comparing Different Annuity Payout Options

Considering Diversification and Portfolio Balance

The Bottom Line

Indexed Annuity FAQs

An annuity payout option determines how and when the funds invested in an annuity contract are paid out to the annuitant, affecting the amount and duration of income received during retirement.

To choose the right annuity payout option, consider your individual financial needs, goals, risk tolerance, and life expectancy. Consult with a financial advisor for personalized guidance and compare various annuity payout options before making a decision.

Annuity payouts are generally subject to federal income tax on the earnings portion of the payments. The tax treatment depends on whether the annuity is qualified or non-qualified, with qualified annuities being fully taxable and non-qualified annuities only taxed on the earnings portion.

Common risks associated with annuity payout options include inflation, longevity, investment, counterparty, and liquidity risks. To mitigate these risks, consider factors such as contract features, diversification, and choosing a financially stable annuity provider.

Changing an annuity payout option after payments have begun can be difficult, as most annuity contracts have strict terms and conditions regarding payout options. However, some annuity contracts may allow changes under specific circumstances. Consult your annuity provider or a financial advisor for more information on your specific situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.