Withdrawal benefits, in the context of retirement planning, refer to the periodic disbursement of funds from retirement savings or pension plans to support individuals during their retirement years. These benefits are designed to provide a steady income stream to retirees and help meet their financial needs after they cease active employment. The specific withdrawal amount and frequency are typically determined based on factors such as the retiree's age, account balance, and the rules and regulations governing the retirement plan. Withdrawal benefits serve as a crucial component of retirement income planning, ensuring retirees have a sustainable and comfortable financial outlook throughout their retirement journey. A Traditional Individual Retirement Account (IRA) allows you to make pre-tax contributions, which grow tax-deferred until retirement. Upon reaching the age of 59½, you can start making withdrawals, known as distributions, which are then taxed as ordinary income. A Roth IRA operates inversely to a Traditional IRA. Contributions are made post-tax, but withdrawals during retirement are generally tax-free, provided you meet certain conditions. This can be especially advantageous if you expect to be in a higher tax bracket in retirement. 401(k) and 403(b) plans are employer-sponsored retirement accounts. Like Traditional IRAs, contributions are typically made pre-tax, and withdrawals are taxed as ordinary income. Employers often match contributions to a certain percentage, providing an excellent opportunity to boost your retirement savings. Pension plans are employer-sponsored plans that guarantee a set income in retirement, based on factors like years of service and salary. These plans are becoming less common but can offer significant withdrawal benefits for those who have them. Annuities are insurance products that can provide a steady income stream in retirement. Withdrawals from an annuity depend on the type of annuity and the terms of the contract. A systematic withdrawal plan involves withdrawing a fixed amount from your retirement account each year. This amount could be a specific dollar figure or a percentage of the total account balance. The 4% rule is a widely recognized withdrawal strategy that suggests you should withdraw 4% of your retirement savings in the first year of retirement and adjust the amount every subsequent year for inflation. This rule aims to provide a steady income stream and minimize the risk of depleting your savings too soon. The bucket strategy involves dividing your retirement savings into different 'buckets' based on the time horizon and risk level. This allows you to invest more aggressively with money you won't need for several years while keeping the money you'll need soon in more conservative investments. Once you reach the age of 73, you must start taking required minimum distributions (RMDs) from certain retirement accounts, such as a Traditional IRA or 401(k). The amount you must withdraw each year is determined by the IRS and is based on your account balance and life expectancy. Sequence of returns risk refers to the danger of experiencing poor investment returns early in retirement, which can significantly impact the longevity of your savings. Carefully planned withdrawal strategies can help manage this risk. As previously noted, withdrawals from a Traditional IRA are taxed as ordinary income. This means the amount of tax you pay will depend on your total income and tax bracket in the year you make the withdrawal. One of the key advantages of a Roth IRA is the ability to make tax-free withdrawals in retirement. However, to qualify, you must be at least 59½ years old and have had the Roth IRA for at least five years. Similar to a Traditional IRA, withdrawals from a 401(k) or 403(b) plan are taxed as ordinary income. The tax implications can significantly impact your net retirement income, so it's crucial to factor this into your retirement planning. Pension payments are typically taxed as ordinary income. The tax treatment of annuity withdrawals, however, depends on the type of annuity and whether it was purchased with pre-tax or post-tax dollars. There are several strategies to minimize the tax burden on your retirement income, such as tax-efficient withdrawal strategies, Roth conversions, and tax-loss harvesting. It's essential to consult with a tax professional to understand which strategies may be best for your situation. Social Security benefits play a crucial role in most Americans' retirement income. The timing of when you start claiming these benefits can significantly impact your total retirement income and should be factored into your withdrawal strategies. You can start claiming Social Security benefits as early as age 62, but doing so will reduce your monthly benefit. Conversely, delaying benefits past your full retirement age will increase your monthly benefit. The optimal decision depends on several factors, including your health, life expectancy, and financial needs. The decision of when to claim Social Security benefits can impact your retirement account withdrawals. For example, if you delay Social Security, you may need to withdraw more from your retirement accounts in the early years of retirement. Health Savings Accounts are a tax-advantaged way to save for healthcare costs. While not traditionally viewed as a retirement account, HSAs can be a valuable tool in retirement, particularly for covering healthcare expenses. HSA contributions are made pre-tax, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. After age 65, you can withdraw funds for any purpose without penalty, but non-medical withdrawals are taxed as ordinary income. Inflation, the rise in the cost of goods and services over time, can significantly erode the purchasing power of your retirement savings. This makes it crucial to consider inflation in your retirement withdrawal strategy. Several strategies can help protect your retirement income from inflation. These include investing in inflation-protected securities, maintaining a portion of your portfolio in growth-oriented investments, and periodically adjusting your withdrawal amount to account for inflation. A diversified portfolio is a key tool for managing market risk, including during market downturns. By spreading your investments across various asset classes, you can help smooth out returns and reduce the impact of a poor-performing asset on your overall portfolio. During a market downturn, you may need to adjust your withdrawal strategy to avoid depleting your retirement savings too quickly. Strategies might include reducing your withdrawal amount, relying on a fixed-income portfolio, or even delaying retirement, if possible. Understanding withdrawal benefits - the funds accessible from retirement accounts after a certain age - is a pivotal aspect of retirement planning. These benefits, stemming from different types of retirement accounts like Traditional IRA, Roth IRA, 401(k), 403(b), pension plans, and annuities, provide a consistent income stream during retirement years. Each account type offers unique withdrawal benefits with varied tax implications, thus making it critical to comprehend their individual characteristics. Furthermore, employing strategic withdrawal strategies such as the systematic withdrawal plan, the 4% rule, the bucket strategy, or adhering to Required Minimum Distributions (RMDs), can optimize the longevity and utility of these benefits. Altogether, understanding the nature of withdrawal benefits and implementing astute strategies is paramount to ensuring financial security in retirement.Definition of Withdrawal Benefits

Types of Retirement Accounts and Withdrawal Benefits

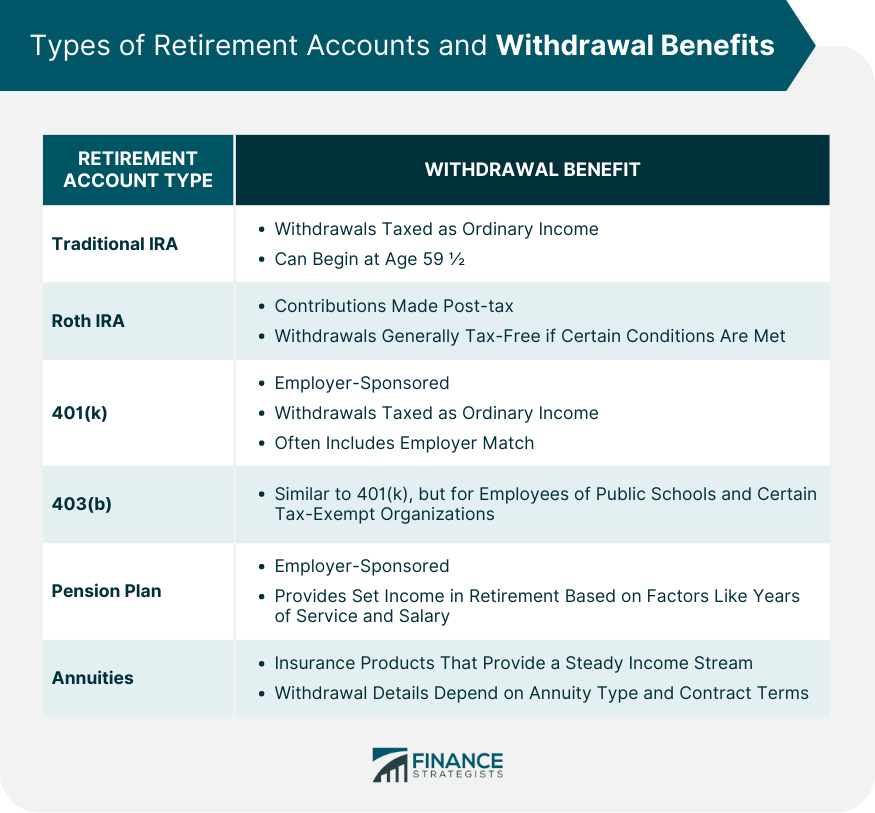

Traditional IRA Withdrawal Benefits

Roth IRA Withdrawal Benefits

401(k) and 403(b) Withdrawal Benefits

Pension Plan Withdrawal Benefits

Annuities Withdrawal Benefits

Withdrawal Strategies for Retirement Income

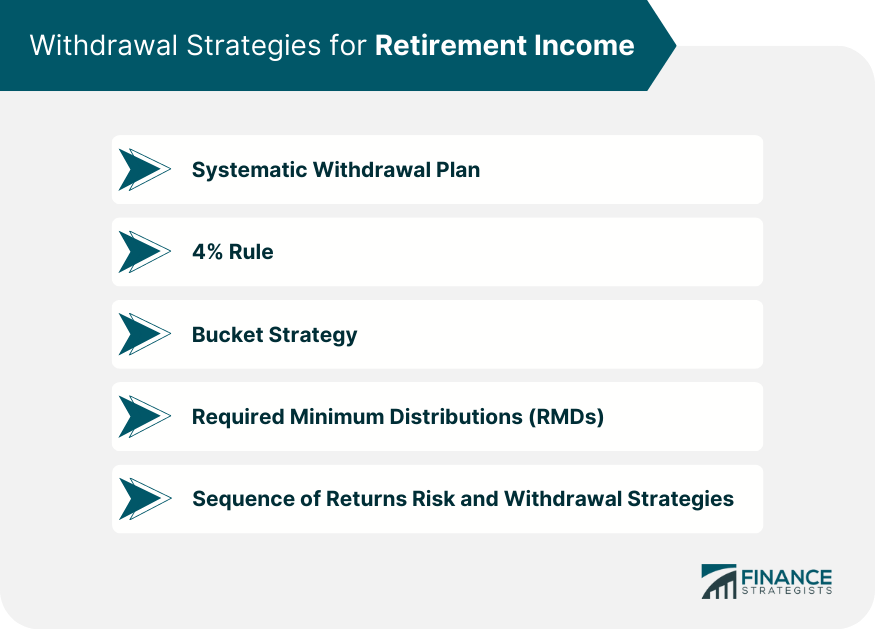

Systematic Withdrawal Plan

4% Rule

Bucket Strategy

Required Minimum Distributions (RMDs)

Sequence of Returns Risk and Withdrawal Strategies

Tax Implications of Withdrawal Benefits

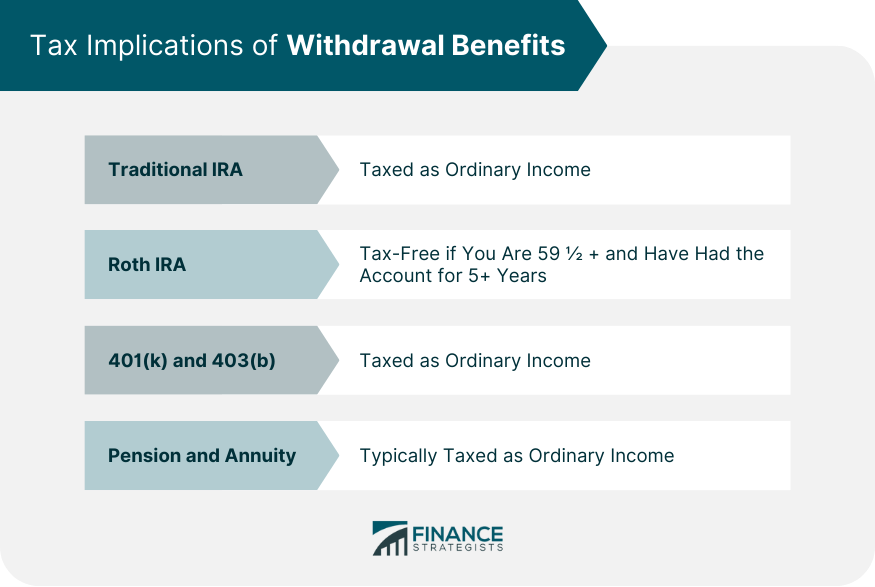

Taxation of Traditional IRA Withdrawals

Tax-Free Roth IRA Withdrawals

401(k) and 403(b) Withdrawal Taxes

Pension and Annuity Withdrawal Taxes

Strategies to Minimize Tax Burden on Withdrawals

Social Security and Withdrawal Benefits

Social Security Benefits and Withdrawal Strategies

Claiming Social Security Benefits Early vs Late

Impact of Social Security on Retirement Withdrawals

Health Savings Accounts (HSAs) and Withdrawal Benefits

Using HSAs for Retirement Health Expenses

HSA Withdrawal Rules and Tax Implications

Inflation and Withdrawal Benefits

Impact of Inflation on Retirement Withdrawals

Strategies to Mitigate Inflation Risk

Navigating Withdrawal Benefits in Market Downturns

Importance of a Diversified Portfolio

Market Downturn Strategies and Withdrawal Benefits

Conclusion

Withdrawal Benefits FAQs

Withdrawal benefits refer to the funds you can access from your retirement accounts, such as an IRA, 401(k), or pension plan, typically starting at age 59.5. They're crucial in retirement planning as they provide a consistent source of income during retirement, replacing the earnings from your employment years.

Withdrawal benefits from a Traditional IRA are taxed as ordinary income upon withdrawal, while contributions are made pre-tax. On the other hand, contributions to a Roth IRA are made post-tax, and withdrawals are generally tax-free during retirement, given you meet certain conditions.

The tax implications of withdrawal benefits depend on the type of retirement account. Withdrawals from Traditional IRAs, 401(k)s, and 403(b)s are taxed as ordinary income, while Roth IRA withdrawals are generally tax-free. The tax treatment of pension and annuity withdrawals depends on the specifics of the plan or contract.

If you withdraw funds from your retirement account before the age of 59.5, you may incur a 10% early withdrawal penalty, in addition to regular income tax. Exceptions exist for certain situations such as specific medical expenses, first-time home purchase, and disability.

Optimizing withdrawal benefits involves creating a personalized strategy based on your unique situation. This includes considering factors such as your retirement age, lifestyle, health, life expectancy, and financial needs. It often helps to consult with a financial advisor who can guide you through this process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.