Retirement withdrawal order refers to the sequence in which retirees draw income from their various retirement accounts to meet their financial needs during retirement. The importance of having a strategic withdrawal order cannot be overstated, as it can significantly impact the longevity of one's savings and the amount of taxes paid during retirement. When determining the optimal withdrawal order, it is crucial to understand the tax implications of different types of retirement accounts: In these accounts, contributions are made with pre-tax dollars, meaning the money you contribute is not subject to income tax at the time of contribution. Instead, the taxes are deferred until you withdraw the funds during retirement. The money in these accounts grows tax-deferred, meaning you don't pay taxes on the investment gains or interest while the funds remain in the account. When you withdraw money during retirement, the withdrawals are taxed as ordinary income, at your tax rate at that time. This can be beneficial if you expect to be in a lower tax bracket during retirement compared to when you were working and contributing to the account. These accounts are funded with after-tax dollars, meaning you've already paid income tax on the money you contribute. The advantage of these accounts is that the investments grow tax-free, and qualified withdrawals during retirement are not subject to income tax. This can be particularly beneficial if you expect to be in a higher tax bracket during retirement or if you anticipate that tax rates will increase in the future. In taxable accounts, contributions are made with after-tax dollars, just like in tax-free accounts. However, unlike tax-free accounts, the dividends and investment gains (capital gains) generated within these accounts are subject to taxes. Capital gains are taxed at either short-term or long-term rates, depending on how long you held the investment before selling it. Short-term capital gains (for investments held less than one year) are taxed at your ordinary income tax rate, while long-term capital gains (for investments held for one year or longer) are taxed at lower rates, depending on your income level. Dividends may be taxed at your ordinary income tax rate or at lower qualified dividend rates, depending on various factors such as the type of dividend and the holding period. Each retiree has unique financial goals and needs, which must be taken into account when determining a withdrawal order. These may include plans for travel, healthcare expenses, and support for family members. Tax laws and regulations, both federal and state, can have a significant impact on the amount of taxes paid during retirement. Staying informed about current and potential future tax policies is essential for an effective withdrawal strategy. Market conditions and the performance of various investments can influence the optimal withdrawal order. Retirees should be prepared to adjust their withdrawal strategies as needed to account for changes in the market. Considering one's age and life expectancy is critical when determining a withdrawal order, as this will affect the required duration of income and the need to plan for long-term healthcare or other expenses. The traditional withdrawal order involves drawing income from accounts in the following sequence: 1. Taxable Accounts: Withdrawals from these accounts first can help minimize capital gains taxes and preserve tax-advantaged accounts for a longer period. 2. Tax-Deferred Accounts: Withdrawals from these accounts will be taxed as ordinary income, but the potential for tax-deferred growth makes them a valuable source of income. 3. Tax-Free Accounts: By tapping into tax-free accounts last, retirees can maximize the benefits of tax-free growth and potentially pass on tax-free assets to their heirs. Some retirees may prefer a modified withdrawal order, which involves the following sequence: 1. Taxable Accounts: As with the traditional strategy, withdrawals from taxable accounts come first to minimize capital gains taxes. 2. Tax-Free Accounts: In this approach, tax-free accounts are tapped before tax-deferred accounts, allowing for potentially lower taxes in retirement. 3. Tax-Deferred Accounts: By drawing from tax-deferred accounts last, retirees can maximize tax-deferred growth. A hybrid withdrawal order combines elements of both traditional and modified strategies, allowing retirees to adapt their approach based on their specific financial circumstances and goals. Maintaining a balance between different types of accounts can help retirees manage their tax liability and adapt to changes in tax laws or personal circumstances. For tax-deferred accounts, retirees must begin taking Required Minimum Distributions (RMDs) by April 1 of the year following the year they turn 72. These mandatory withdrawals may impact the optimal withdrawal order, as they must be taken into account to avoid penalties. For those who plan to leave a financial legacy to their heirs, preserving tax-free accounts can be beneficial. Assets in Roth accounts can be passed on to beneficiaries tax-free, making them an attractive estate planning tool. An effective retirement withdrawal strategy should be flexible and adaptable to changes in one's financial situation, market conditions, and tax laws. Regularly reviewing and adjusting the withdrawal order can help ensure that the strategy remains optimal over time. A well-planned retirement withdrawal order is crucial for maximizing retirement income, minimizing taxes, and ensuring the longevity of one's savings. By understanding the tax implications of various account types, considering personal financial goals, and being aware of tax laws and regulations, retirees can develop a strategic withdrawal order. Common withdrawal strategies include traditional, modified, and hybrid orders, each with its own advantages. Factors such as tax diversification, RMDs, preserving tax-free accounts for heirs, and maintaining flexibility should be considered when choosing an optimal withdrawal order. Customizing the withdrawal order based on individual scenarios and regularly reviewing and adjusting it as needed is essential for achieving a secure and fulfilling retirement.Definition of Retirement Withdrawal Order

Factors Influencing Retirement Withdrawal Order

Types of Accounts and Their Tax Implications

Tax-deferred accounts (Such as 401(k), Traditional IRA)

Tax-free accounts (Such as Roth IRA, Roth 401(k))

Taxable accounts (Such as brokerage accounts)

Personal Financial Goals and Needs

Tax Laws and Regulations

Market Conditions and Investment Performance

Age and Life Expectancy

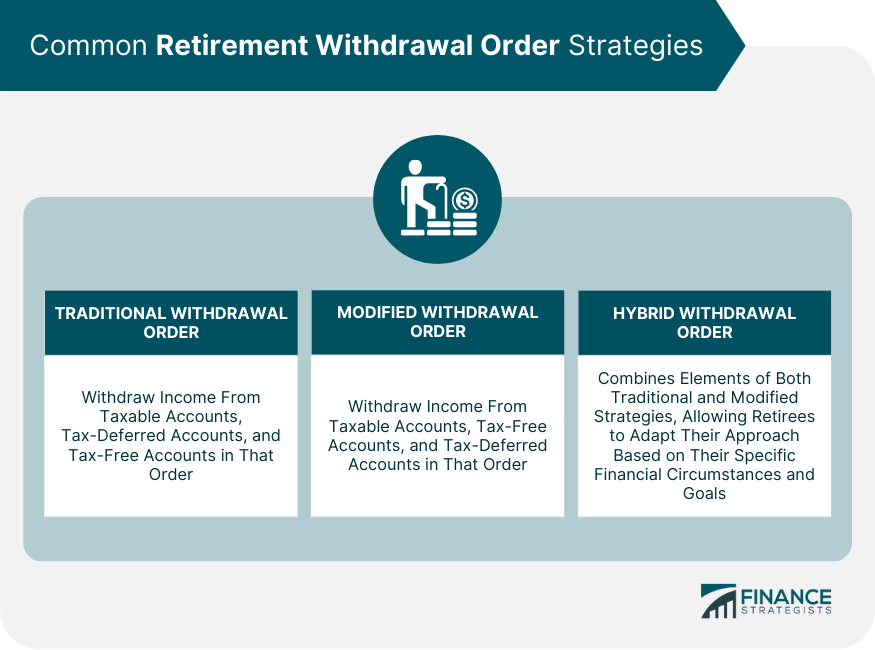

Common Retirement Withdrawal Order Strategies

Traditional Withdrawal Order

Modified Withdrawal Order

Hybrid Withdrawal Order

Key Considerations for Choosing a Withdrawal Order

Tax Diversification

Required Minimum Distributions (RMDs)

Preservation of Tax-Free Accounts for Heirs

Flexibility and Adaptability to Changes in Financial Circumstances or Tax Laws

Conclusion

Retirement Withdrawal Order FAQs

A retirement withdrawal order refers to the sequence in which retirees withdraw funds from their various retirement accounts to meet their financial needs. A strategic retirement withdrawal order is crucial for maximizing retirement income, minimizing taxes, and ensuring the longevity of one's savings.

Retirement accounts, such as tax-deferred accounts (e.g., 401(k), Traditional IRA), tax-free accounts (e.g., Roth IRA, Roth 401(k)), and taxable accounts (e.g., brokerage accounts), have different tax implications. These tax implications play a significant role in determining the optimal retirement withdrawal order to minimize taxes and maximize income.

The three common retirement withdrawal order strategies are traditional, modified, and hybrid. The traditional order involves withdrawing from taxable accounts, followed by tax-deferred accounts, and finally tax-free accounts. The modified order prioritizes taxable accounts, then tax-free accounts, and lastly tax-deferred accounts. The hybrid order combines elements of both traditional and modified strategies, allowing retirees to adapt their approach based on their specific financial circumstances and goals.

Factors to consider when choosing a retirement withdrawal order include tax diversification, Required Minimum Distributions (RMDs), preservation of tax-free accounts for heirs, and the flexibility and adaptability to changes in financial circumstances or tax laws.

A retirement withdrawal order should be customized to fit each retiree's unique situation. For early retirees, a modified withdrawal order may be more appropriate, while a traditional order may be suitable for those who retire later. High-income earners may benefit from a hybrid withdrawal order, while low-income earners may find a modified order advantageous. Regularly reviewing and adjusting the withdrawal order based on one's circumstances is essential for optimizing retirement income and minimizing taxes.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.