In-service distributions refer to withdrawals of money or assets from a retirement account by an employee who is still employed by the same company. These distributions are allowed under certain circumstances, such as when the employee reaches a certain age or has a financial hardship. In the context of employer-sponsored retirement plans such as 401(k) or 403(b) plans, in-service distributions can be a useful tool for employees who need access to funds while still employed. However, they may also have negative consequences, such as reducing the amount of money available for retirement and incurring penalties or taxes. It is important for employees to carefully consider their financial situation and consult with a financial advisor before making any decisions about in-service distributions from their retirement accounts. These employer-sponsored retirement plans allow employees to save and invest a portion of their income before taxes are taken out. In some cases, these plans permit In-Service Distributions. Like 401(k) plans, 403(b) plans are designed for employees of public schools, non-profit organizations, and certain ministers. They may also allow In-Service Distributions under specific circumstances. These non-qualified, deferred compensation plans are meant for state and local government employees and some non-governmental organizations. 457(b) plans may also offer In-Service Distributions. Some other qualified retirement plans may also permit In-Service Distributions, depending on the specific plan's provisions and guidelines. Typically, employees must be at least 59½ years old to be eligible for In-Service Distributions. However, some plans may have different age criteria. In certain situations, employees may qualify for In-Service Distributions if they face financial hardship, such as unexpected medical expenses, funeral costs, or expenses related to natural disasters. Some plans may require a minimum length of service before allowing In-Service Distributions. Each retirement plan may have unique requirements for In-Service Distributions. It is essential to review the plan documents to understand the specific criteria. These distributions are based on the employee's age, typically starting at 59½ years. Employees facing financial hardship may be eligible for hardship withdrawals, provided they meet the plan's criteria. Some plans allow employees to borrow money from their retirement accounts. These loans usually have specific repayment terms and interest rates. Retirement plans may have additional distribution options based on the plan's provisions and guidelines. In-Service Distributions are generally subject to ordinary income tax and, in some cases, early distribution penalties. The distribution amount is usually added to the employee's annual taxable income, and taxes are paid at the employee's ordinary income tax rate. If the employee is under 59½ years old, a 10% early distribution penalty may apply, unless an exception is met. Employees can consider rollover options to minimize the tax impact of In-Service Distributions. A direct rollover involves transferring the distribution amount directly to another qualified retirement plan or an IRA, avoiding immediate tax consequences. An indirect rollover requires the employee to receive the distribution and then deposit it into another qualified plan or IRA within 60 days. However, a mandatory 20% withholding tax may apply, which must be compensated by the employee. Retirement plan loans usually have tax implications if they are not repaid on time or if the employee defaults. In such cases, the outstanding loan balance is considered a taxable distribution and may be subject to income taxes and early distribution penalties. Employees can explore various strategies to minimize the tax impact of In-Service Distributions, such as timing the distribution, using rollover options, and consulting with tax professionals. In-Service Distributions can provide immediate financial relief to employees facing financial hardships or needing funds for specific life events. Depending on the plan's provisions, these distributions can be used for essential expenses such as education, medical bills, or buying a home. In-Service Distributions allow employees to access better investment options by rolling over the funds into an IRA or another retirement plan. In-Service Distributions can result in tax penalties if not managed correctly, especially in the case of early distributions or defaulted loans. Withdrawing funds from retirement accounts may reduce the overall retirement savings and impact long-term financial goals. In-Service Distributions may hinder retirement savings growth, affecting an employee's ability to achieve their long-term financial goals. Having an emergency fund can help employees cover unexpected expenses without tapping into their retirement accounts. Personal loans can be another option to cover financial needs, as they generally have lower interest rates than credit cards. For homeowners, a home equity line of credit (HELOC) can provide access to funds based on the equity in their homes. Employees can explore other personal financial resources, such as savings accounts, investments, or assistance from friends and family, before considering In-Service Distributions. The Internal Revenue Service (IRS) has specific rules governing In-Service Distributions, including eligibility criteria, taxation, and reporting requirements. The Employee Retirement Income Security Act (ERISA) provides guidelines for retirement plans and their provisions, including In-Service Distributions. Each retirement plan may have its own rules and restrictions regarding In-Service Distributions, which both employers and employees must follow. Employers and employees must adhere to reporting requirements for In-Service Distributions, including providing accurate information on tax forms and plan documents. Employees should plan for potential financial needs by building emergency funds, evaluating insurance options, and managing debt effectively. Before considering In-Service Distributions, employees should explore alternative financial resources to cover their immediate needs. Employees should be aware of the tax implications and strategies to minimize the tax impact of In-Service Distributions. Employees should regularly review their retirement plan's performance to ensure they are on track to achieve their long-term financial goals. In-service distributions refer to the ability of employees to withdraw money or assets from their employer-sponsored retirement plans, such as 401(k), 403(b), or 457(b) plans, under certain circumstances while still being employed by the same company. The eligibility criteria for in-service distributions may vary depending on factors such as age, length of service, hardship criteria, and plan-specific requirements. In-service distributions can provide immediate financial relief for employees facing financial hardships or needing funds for specific life events. However, they may also have negative consequences, such as reducing the amount of money available for retirement and incurring penalties or taxes. Employees should carefully consider their financial situation and explore alternatives before making any decisions about in-service distributions. Employers and employees must adhere to IRS and ERISA regulations governing in-service distributions, as well as plan-specific rules and reporting requirements. Regularly reviewing the retirement plan's performance can help employees stay on track to achieve their long-term financial goals.What Are In-Service Distributions?

Types of Retirement Plans Allowing In-Service Distributions

401(k) Plans

403(b) Plans

457(b) Plans

Other Qualified Retirement Plans

Eligibility Criteria for In-Service Distributions

Age Requirements

Hardship Criteria

Length of Service

Plan-Specific Requirements

Types of In-Service Distributions

Age-Based Distributions

Hardship Withdrawals

Loans From Retirement Plans

Other Plan-Specific Distribution Options

Tax Implications and Penalties

Taxation of In-Service Distributions

Ordinary Income Tax

Early Distribution Penalties

Rollover Options to Minimize Tax Impact

Direct Rollovers

Indirect Rollovers

Loan Repayments and Tax Implications

Strategies to Minimize Tax Impact

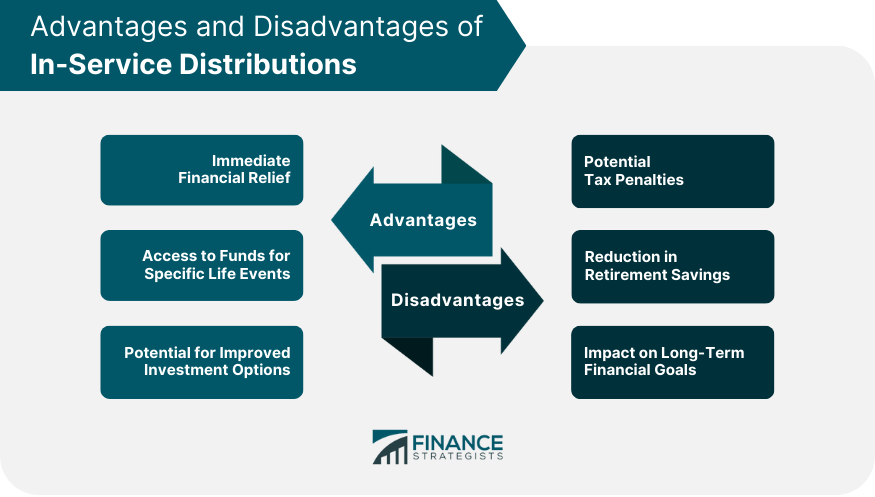

Advantages and Disadvantages of In-Service Distributions

Advantages

Immediate Financial Relief

Access to Funds for Specific Life Events

Potential for Improved Investment Options

Disadvantages

Potential Tax Penalties

Reduction in Retirement Savings

Impact on Long-Term Financial Goals

Alternatives to In-Service Distributions

Emergency Funds

Personal Loans

Home Equity Lines of Credit

Other Personal Financial Resources

Regulations for In-Service Distributions

IRS Rules Governing In-Service Distributions

ERISA Regulations

Plan-Specific Rules and Restrictions

Reporting Requirements for Employers and Employees

Best Practices for Managing In-Service Distributions

Planning for Potential Financial Needs

Evaluating Alternatives to In-Service Distributions

Understanding Tax Implications and Strategies

Regularly Reviewing Retirement Plan Performance

Conclusion

In-Service Distributions FAQs

In-service distributions refer to withdrawals of money or assets from a retirement account by an employee who the same company still employs.

The minimum age requirement for in-service distributions varies depending on the retirement plan. Generally, employees must be at least 59 1/2 years old to qualify.

Employees may take an in-service distribution for various reasons, such as financial hardship, medical expenses, or to pay for a child's college education.

In some cases, taking an in-service distribution may incur penalties or taxes. It's important to consult with a financial advisor before deciding about taking an in-service distribution.

Taking an in-service distribution reduces the amount of money available for retirement and can have long-term consequences for an employee's retirement savings. It's important to consider the impact of an in-service distribution before deciding.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.