Excess Contribution Refunds are the process of returning excess funds that an individual has contributed to a retirement account beyond the allowable limits set by the IRS. These limits vary depending on the type of retirement account, such as Traditional IRA (Individual Retirement Arrangement), Roth IRA, 401(k), 403(b), SEP IRA, or SIMPLE IRA. Excess contributions can occur due to misunderstandings of the rules, employer errors, or other circumstances. If not corrected in a timely manner, excess contributions can result in tax penalties. Individuals can avoid excess contributions and maximize their retirement savings by understanding retirement account rules, monitoring contributions, and seeking professional guidance when necessary. There are several types of retirement accounts available to individuals, each with its own set of rules and contribution limits: Traditional IRA: A tax-deferred individual retirement account that allows individuals to contribute pre-tax dollars, which grow tax-deferred until withdrawn during retirement. Roth IRA: An individual retirement account funded with after-tax dollars, allowing for tax-free growth and withdrawals in retirement. 401(k): An employer-sponsored retirement plan that allows employees to contribute pre-tax dollars, with employers often providing matching contributions. 403(b): Similar to a 401(k), but specifically designed for employees of non-profit organizations, public schools, and certain religious institutions. SEP IRA: A Simplified Employee Pension (SEP) Individual Retirement Account designed for small businesses and self-employed individuals. SIMPLE IRA: A Savings Incentive Match Plan for Employees (SIMPLE) IRA is an employer-sponsored retirement plan for small businesses with fewer than 100 employees. Each retirement account type has specific annual contribution limits that are subject to change: Annual Limits: The maximum amount an individual can contribute to a specific retirement account in a given year Catch-Up Contributions: Additional contributions allowed for individuals aged 50 or older to help them save more for retirement Aggregate Limits: If applicable, the total combined contribution limit across multiple retirement accounts Excess contributions occur when an individual contributes more than the allowable limit to a retirement account. This may be due to misunderstanding the rules, employer errors, or other circumstances. If not corrected, excess contributions can result in tax penalties. Individuals must monitor their retirement account contributions to ensure they stay within the limits. Regularly reviewing account statements, coordinating with the human resources or payroll department, and understanding the rules can help prevent over-contributions. Several scenarios can lead to excess contributions: Employer Errors: Mistakes made by employers in calculating or processing contributions Changing Jobs: Starting a new job and contributing to a new retirement plan without accounting for contributions made at a previous job Multiple Retirement Accounts: Contributing to more than one retirement account without considering the aggregate limits If an excess contribution is identified, it is important to address it promptly to avoid penalties: Tax Filing Deadline: Typically, the deadline for correcting excess contributions is the tax filing deadline (usually April 15) for the year in which the excess contribution was made. Extension Period: If an individual has filed for an extension on their tax return, they may have until October 15 to correct excess contributions. To request an excess contribution refund, follow these steps: Correcting excess contributions may have tax implications: Taxes on Withdrawn Earnings: Earnings generated by the excess contribution may be subject to income tax and, in some cases, an additional 10% early withdrawal penalty. Penalties for Not Correcting Excess Contributions: Please correct excess contributions to avoid a 6% excise tax on the excess amount, which is assessed annually until the excess contribution is corrected. To avoid excess contributions, individuals should implement the following strategies: Regularly Reviewing Account Statements: Keep track of all contributions made to retirement accounts throughout the year to ensure they stay within limits. Coordinating With Human Resources or Payroll Department: Communicate with the appropriate department at your workplace to ensure that your contributions are accurately calculated and processed. Educating Oneself on Contribution Limits: Familiarize yourself with the rules and limits of your retirement account to avoid misunderstandings. Consulting With a Financial Advisor: Seek the guidance of a professional financial advisor to help navigate retirement account rules and avoid excess contributions. There are unique circumstances that may require special attention when dealing with excess contributions: Rules for inherited IRAs differ from those of traditional or Roth IRAs, and individuals inheriting an IRA should consult a financial advisor to understand the specific rules that apply. Spousal IRAs are established for a non-working spouse and are subject to different contribution limits. Understanding the rules for spousal IRAs can help avoid excess contributions. When conducting a rollover or transfer between retirement accounts, it is crucial to follow the appropriate guidelines to avoid unintentional excess contributions. Excess contribution refunds are the process of returning funds an individual has contributed to a retirement account beyond the allowable limits set by the IRS. Each retirement account type has specific annual contribution limits that are subject to change, and excess contributions can occur due to misunderstandings of the rules, employer errors, or other circumstances. To avoid excess contributions, individuals should implement monitoring strategies, understand the rules, and consult with a financial advisor. If an excess contribution is identified, it is important to address it promptly to avoid penalties. The process of obtaining an excess contribution refund involves notifying the financial institution, completing required forms, and calculating earnings or losses. Correcting excess contributions may have tax implications, and there are unique circumstances that may require special attention when dealing with excess contributions, such as inherited IRAs, spousal IRAs, and rollovers/transfers.What Are Excess Contribution Refunds?

Understanding the Basics of Excess Contribution Refund

Types of Retirement Accounts

Contribution Limits

Excess Contributions

Identifying Excess Contributions

Identifying Over-Contributions

Common Scenarios Leading to Excess Contributions

Excess Contribution Refund Process

Deadlines for Correcting Excess Contributions

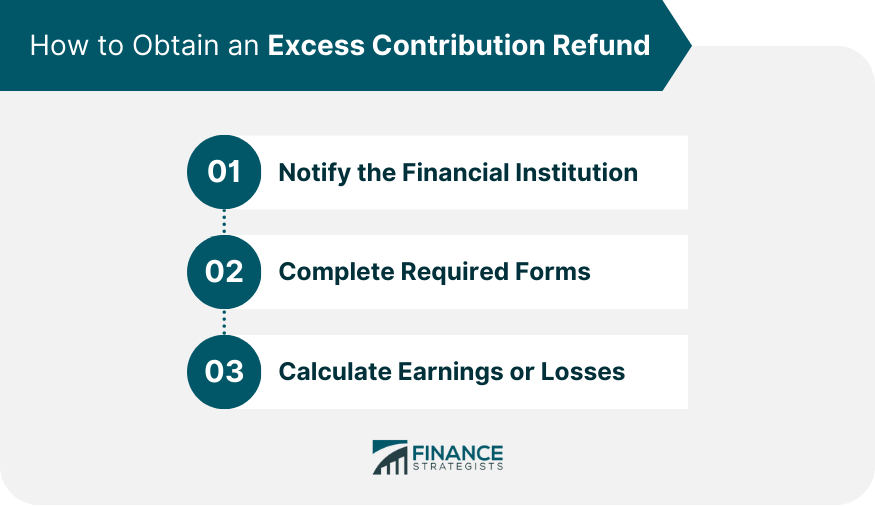

Steps to Obtain a Refund

1. Notify the Financial Institution: Contact the financial institution that holds the retirement account and inform them of the excess contribution.

2. Complete Required Forms: Fill out any necessary forms provided by the financial institution to initiate the refund process.

3. Calculate Earnings or Losses: Determine any earnings or losses associated with the excess contribution, as this amount must also be withdrawn.

Tax Implications

Prevention Strategies for Excess Contributions and Excess Contribution Refunds

Monitoring Contributions

Properly Understanding the Rules

Special Considerations for Excess Contributions and Excess Contribution Refunds

Inherited IRAs

Spousal IRAs

Rollovers and Transfers

Conclusion

Excess Contribution Refund FAQs

An excess contribution refund is a return of funds to a retirement account holder who has over-contributed beyond the allowable limit.

To obtain an excess contribution refund, you should first contact the financial institution that holds the retirement account and inform them of the excess contribution. Next, fill out any necessary forms provided by the financial institution to initiate the refund process. Finally, determine any earnings or losses associated with the excess contribution, as this amount must also be withdrawn.

Yes, you can request an excess contribution refund from your 401(k) plan. However, it's important to note that not all plans allow refunds, and the process may vary depending on the plan's rules.

The deadline for requesting an excess contribution refund typically depends on your retirement account type. For example, IRA holders have until the tax deadline (usually April 15) of the following year to request a refund.

An excess contribution refund may affect your taxes, depending on when the excess contribution was made and when it was refunded. Generally, any earnings on the excess contribution will be subject to income tax and a 10% early withdrawal penalty if you're under the age of 59 ½.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.