Restricted stock awards are a form of equity-based compensation given to employees in the form of company shares. These shares come with specific conditions and restrictions, typically requiring the employee to meet certain performance or service milestones before they fully own the stock. Restricted stock awards serve as a tool for companies to attract, motivate, and retain key employees by offering them an ownership stake in the business. This form of compensation aligns employee and company interests, incentivizes long-term commitment, and rewards strong performance. Restricted stock awards differ from stock options and phantom stock plans, which grant the right to purchase or receive company shares at a later date. Stock options require employees to pay an exercise price, while phantom stock plans provide a cash payout based on the value of the underlying shares. In contrast, restricted stock awards grant actual shares upfront, subject to vesting conditions. Restricted stock awards are granted to employees according to a vesting schedule, which outlines the conditions and timeframes for earning full ownership of the shares. Vesting can be based on performance milestones, length of service, or a combination of both, typically taking place over several years. Employees holding restricted stock awards may be entitled to receive dividends on their shares, even before the stock vests. Dividend rights vary depending on the company's policies and the specific terms of the award agreement. Voting rights associated with restricted stock awards depend on the terms of the grant agreement. Employees may have the right to vote on company matters proportional to their unvested shares, or voting rights may be withheld until the stock vests. Restricted stock awards are subject to transfer restrictions, limiting the employee's ability to sell or transfer the shares until they have fully vested. These restrictions help ensure that employees remain committed to the company and its long-term success. Employees who leave the company or fail to meet performance or service requirements may forfeit their unvested restricted stock awards. Forfeiture provisions protect the company's interests and encourage employee retention and performance. When restricted stock awards vest, employees are generally taxed on the fair market value of the shares at the time of vesting. The vested shares are considered ordinary income and are subject to federal, state, and local income taxes and Social Security, Medicare, and unemployment taxes. Employees may choose to make a Section 83(b) election, which allows them to pay income tax on the fair market value of the restricted stock awards at the time of grant rather than at vesting. This election can be advantageous if the employee anticipates significant stock price appreciation, as it allows them to lock in a lower tax rate based on the initial grant value. Companies are responsible for withholding and reporting income taxes associated with restricted stock awards. This process can be complex and requires diligent record-keeping and clear communication with employees about their tax liabilities and withholding options. Companies can generally claim a tax deduction for the value of restricted stock awards at the time they vest and become taxable income for employees. This deduction can help offset the costs of the equity-based compensation program, but companies must carefully navigate the relevant tax rules and limitations. The FASB provides guidelines for accounting for restricted stock awards, which require companies to recognize the expense associated with these awards over the vesting period. Companies must carefully follow these guidelines to ensure accurate financial reporting and compliance with Generally Accepted Accounting Principles (GAAP). Restricted stock awards are subject to SEC regulations, including disclosure and reporting requirements under the Securities Act and the Securities Exchange Act. Companies must ensure that their restricted stock award plans and related documentation comply with these regulations to avoid potential penalties and reputational damage. Companies listed on stock exchanges must adhere to the exchange's specific listing requirements regarding equity-based compensation plans, such as restricted stock awards. Depending on the specific exchange, these requirements may include shareholder approval, disclosure obligations, and corporate governance standards. Employees receiving restricted stock awards may become subject to insider trading restrictions due to their access to non-public material information about the company. It is crucial for companies to educate employees about insider trading laws and implement policies to prevent potential violations and associated legal consequences. Designing and implementing Restricted Stock Awards (RSAs) is a process that involves several steps. Here is a step-by-step guide to designing and implementing RSAs: 1. Establish the Purpose and Goals: Begin by defining the goals and objectives of the RSA program, such as retaining talent, aligning employee interests with shareholders, or rewarding high performers. 2. Determine Eligibility: Decide which employees are eligible to receive RSAs. This could include all employees or a specific group, such as executives, managers, or high-performing employees. 3. Develop the Terms and Conditions: Define the terms and conditions of the RSAs, including the vesting period, performance metrics (if any), and restrictions on the transfer of shares. 4. Determine the Number of Shares: Decide how many shares each employee will receive. This can be done based on the employee's position, performance, or other factors relevant to the company. 5. Set the Grant Date and Value: Establish a grant date, which is the date when the RSAs are awarded to the employees. Determine the fair market value of the shares on the grant date, as this will be used for accounting and tax purposes. 6. Draft the RSA Agreement: Create a legal agreement that outlines the terms and conditions of the RSAs. This should include details such as the grant date, number of shares, vesting schedule, performance conditions, and any restrictions on the transfer of shares. 1. Obtain Board Approval: Present the RSA program to the company's board of directors for approval. Be prepared to answer any questions or address concerns the board may have. 2. Communicate With Employees: Inform eligible employees about the RSAs, including the terms and conditions, the number of shares granted, and the vesting schedule. Provide them with a copy of the RSA agreement and any other necessary documentation. 3. Implement the RSA Program: Grant the RSAs to the eligible employees and track the vesting schedule, ensuring that the shares are properly issued and recorded on the company's cap table. 4. Monitor and Review the Program: Regularly evaluate the effectiveness of the RSA program in achieving its goals and make any necessary adjustments. Restricted stock awards provide a powerful incentive for key employees to remain with the company and contribute to its success. By offering a stake in the business, employees are motivated to work towards the company's long-term growth and profitability. When employees receive restricted stock awards, their financial interests become aligned with those of shareholders. This alignment encourages employees to make decisions that benefit the company and its investors, promoting long-term value creation. Unlike stock options, which require employees to pay an exercise price, restricted stock awards grant actual shares without any upfront cost. This feature makes them an attractive form of equity-based compensation for employees who can benefit from potential stock price appreciation without an initial investment. Restricted stock awards retain some value even in declining markets, as employees still own the underlying shares. In contrast, stock options can become worthless if the exercise price is higher than the current market price, providing no benefit to the employee. Restricted stock awards generally involve simpler administration and communication compared to stock options or phantom stock plans. Since employees receive actual shares, the value and ownership implications are more straightforward and easier to understand. Issuing restricted stock awards can result in the dilution of existing shareholders' ownership, as the company issues new shares to employees. This dilution may lead to a decrease in the value of existing shares and a reduced EPS ratio, potentially impacting shareholder perceptions and the stock's market value. Restricted stock awards can have significant tax implications for both employees and companies. Employees may face tax liabilities upon vesting, while companies must navigate complex tax withholding and reporting requirements and the impact on their tax deductions. If the company's stock price declines or underperforms, employees holding restricted stock awards may become demotivated as the value of their awards decreases. This demotivation could negatively impact productivity and overall job satisfaction, potentially leading to higher employee turnover. The issuance of restricted stock awards can reduce a company's EPS ratio as the number of outstanding shares increases. A lower EPS can impact a company's stock price and market valuation, potentially making it less attractive to investors. Restricted stock awards can be particularly attractive for start-ups and small businesses, which may have limited cash resources for employee compensation. By offering equity in the company, these businesses can incentivize employee commitment and align their interests with the company's long-term success. Family-owned businesses can use restricted stock awards to incentivize and retain key non-family employees while maintaining family control of the company. By carefully structuring the plan, family businesses can balance the need for employee incentives with the desire to preserve family ownership. Restricted stock awards may be less common in non-profit organizations, as these entities typically do not issue shares. However, non-profits can explore alternative equity-based compensation plans, such as phantom stock or stock appreciation rights, to incentivize and retain key employees while aligning their interests with the organization's mission and goals. Publicly traded companies often use restricted stock awards as part of their overall compensation packages to attract, motivate, and retain top talent. These companies must navigate complex regulatory and disclosure requirements and manage the impact of restricted stock awards on their earnings per share and shareholder perceptions. Restricted stock awards are valuable for attracting, motivating, and retaining key employees, but companies must understand the complexities and implications. Effective plans align with objectives and comply with regulations, and companies should evaluate factors such as objectives, participants, vesting, taxes, and regulations. Balancing these factors is crucial for success. Staying informed about emerging trends and best practices is necessary to remain competitive, including exploring new forms of equity compensation, innovative designs, and technology solutions. Companies should consult experts in equity compensation to navigate the complexities of restricted stock awards and maximize benefits. A financial advisor or legal professional can provide guidance on plan design, compliance, and administration.What Are Restricted Stock Awards?

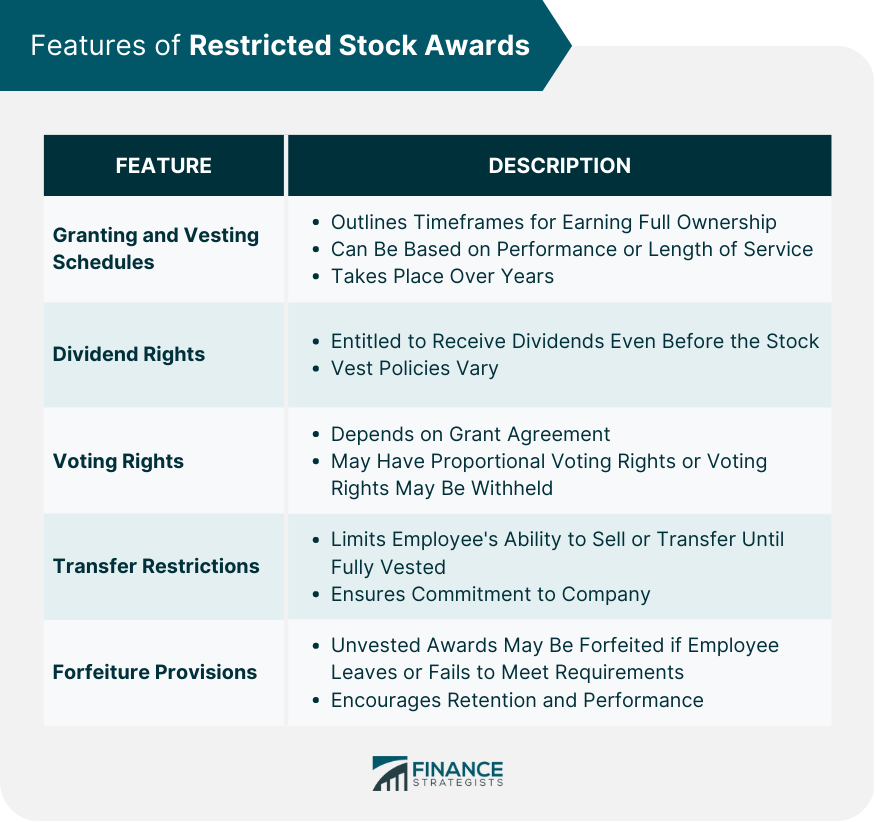

Features of Restricted Stock Awards

Granting and Vesting Schedules

Dividend Rights

Voting Rights

Transfer Restrictions

Forfeiture Provisions

Tax Implications of Restricted Stock Awards

Taxation at Vesting

Section 83(b) Election

Tax Withholding and Reporting Requirements

Employer Tax Deductions

Accounting and Regulatory Considerations of Restricted Stock Awards

Financial Accounting Standards Board (FASB) Guidelines

Securities and Exchange Commission (SEC) Regulations

Stock Exchange Listing Requirements

Insider Trading Restrictions

Designing and Implementing Restricted Stock Awards

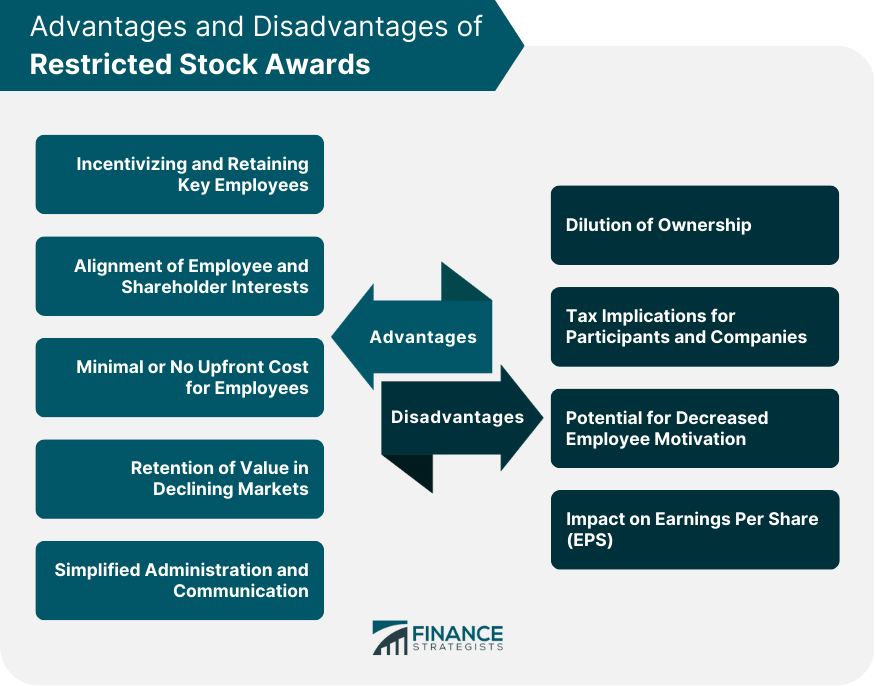

Advantages of Restricted Stock Awards

Incentivizing and Retaining Key Employees

Alignment of Employee and Shareholder Interests

Minimal or No Upfront Cost for Employees

Retention of Value in Declining Markets

Simplified Administration and Communication

Disadvantages and Challenges of Restricted Stock Awards

Dilution of Ownership

Tax Implications for Participants and Companies

Potential for Decreased Employee Motivation

Impact on Earnings Per Share (EPS)

Restricted Stock Awards in Various Industries

Start-Ups and Small Businesses

Family-Owned Businesses

Non-profit Organizations

Publicly Traded Companies

Final Thoughts

Restricted Stock Awards FAQs

Restricted stock awards provide a powerful incentive for employee commitment and retention by aligning their interests with the company's success. They also typically involve minimal or no upfront costs for employees, retain value in declining markets, and have simplified administration and communication requirements.

Restricted stock awards grant actual shares of the company, while stock options give employees the right to purchase shares at a predetermined price, and phantom stock plans provide cash or stock bonuses tied to the company's stock price. Each plan has distinct tax implications, vesting conditions, and potential benefits for employees and companies.

Employees generally face tax liabilities when restricted stock awards vest, as the fair market value of the shares is considered ordinary income. However, employees can make a Section 83(b) election to pay income tax at the grant date, potentially locking in a lower tax rate if the stock price is expected to appreciate significantly.

Companies must adhere to Financial Accounting Standards Board (FASB) guidelines, Securities and Exchange Commission (SEC) regulations, stock exchange listing requirements, and insider trading restrictions when offering restricted stock awards. These considerations involve accurate financial reporting, disclosure obligations, and compliance with corporate governance standards.

Companies may face challenges such as dilution of ownership, tax implications for participants and the company, potential for decreased employee motivation in declining markets, and impact on earnings per share (EPS). To overcome these challenges, companies should carefully design and administer their restricted stock award plans, ensuring compliance with relevant regulations and effective communication with employees.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.