Stock investing means buying ownership shares in public companies. When you purchase a stock, you own a small piece of that business. If the company grows, becomes more profitable, or becomes more valuable in investors’ eyes, the stock price may rise. Stocks are not just numbers on a screen. They represent real businesses with products, customers, revenue, expenses, competitors, and risks. That distinction matters because successful investing is not only about watching price movements. It is about understanding what you own and why it may become more valuable over time. Investors generally make money from stocks in two ways: price appreciation and dividends. Price appreciation happens when the value of a stock rises above what you paid for it. If you buy a stock at $50 and later sell it for $75, the $25 difference is your gain before taxes and fees. Dividends are another potential source of return. Some companies distribute a portion of their profits to shareholders in the form of cash payments. Not every company pays dividends, especially younger or faster-growing companies that may reinvest profits back into the business. For long-term investors, both price growth and dividends can contribute to total return. As with everything in the market, stocks rise and fall. Prices move based on company performance, economic conditions, interest rates, investor expectations, and broader market sentiment. A company can be profitable and still see its stock decline if investors expect stronger results. That volatility is part of the trade-off. Note that stocks have historically offered long-term growth potential, but they do not provide guaranteed returns. This is why money needed soon may not belong in stocks. If you need cash for a short-term goal, a market downturn could force you to sell at the wrong time. You can invest in individual stocks or through stock funds. Individual stocks give you exposure to one company. This can create upside if the company performs well, but it also increases risk because your outcome depends heavily on that single business. Stock funds, such as mutual funds and exchange-traded funds, hold many stocks at once. Some funds track broad indexes, such as the overall U.S. stock market, while others focus on specific sectors, regions, or investing styles. Funds can be a simpler starting point, especially for beginners, because they provide diversification without requiring you to choose every company yourself. Your time horizon is the length of time you expect to keep your money invested before you need to use it. As such, it’s one of the most important factors in stock investing because it affects how much risk you can reasonably take. If you are investing for retirement decades from now, you may be able to tolerate short-term market swings because your money has time to recover. If you need the money in the next year or two, stocks may be too risky. Longer timelines allow compounding to work, in which your returns generate returns of their own over time. This is why starting early is recommended, even with modest contributions. The more time your money has to stay invested, the more opportunity it has to grow. Before choosing a stock or fund, clarify your why. Your goal shapes nearly every decision that follows. Investing for retirement is different from investing for a home down payment, education expenses, or general wealth-building. A long-term goal can usually tolerate more stock exposure because there is more time to recover from downturns. A short-term goal may require more stability. Without a clear goal, it’s easy to chase whatever looks exciting in the moment. Your investing decisions should be focused. Clarify your goals. Many investors want to wait for the perfect moment to buy, wishing to hit it big by timing the market. The problem is that the perfect moment is usually obvious only in hindsight. Markets can fall further after you buy, or they can rise while you are waiting on the sidelines. A more practical approach is to invest consistently. This may mean contributing a set amount each month or investing automatically through a retirement plan. This strategy, often called dollar-cost averaging, helps reduce the emotional pressure of deciding when to invest. It also builds the habit of putting money to work regularly. Diversification means spreading your money across different investments so that one bad outcome does not derail your entire portfolio. If all your money is in one stock, your results depend heavily on that company. If your money is spread across many companies, sectors and asset types, the risk is more balanced. As mentioned, broad-market funds can be an efficient way for beginners to diversify. Instead of trying to pick a handful of winners, you can gain exposure to hundreds or even thousands of companies. You should also note that diversification doesn’t eliminate risk, but it can make your portfolio less dependent on any single decision. If you buy individual stocks, take time to understand the business behind the ticker symbol. Look at how the company makes money, whether it’s profitable, how much debt it carries, and what could support or threaten future growth. A familiar company is not automatically a good investment. A popular product, strong brand, or trending stock can still be overpriced. The question is not only whether the company is good. The question is whether the stock is attractive at the price you are paying. Hype is one of the easiest traps in stock investing. A stock rises quickly, people talk about it online, and suddenly it feels like everyone is making money except you. That fear of missing out can push investors to buy after much of the move has already happened. The danger is that hype often separates price from fundamentals. A stock can become expensive simply because attention is high. Before buying, ask whether the investment still makes sense based on the business, valuation, risk, and your own plan. If the only reason to buy is that the price has been rising, that is speculation, not strategy. Risk tolerance refers to how much volatility you can handle without making poor decisions. Many investors believe they are comfortable with risk until their portfolio drops sharply. A portfolio that is too aggressive can lead to panic selling during downturns. One that’s too conservative may not grow enough to meet long-term goals. The right balance is the one you can realistically stick with through both strong and weak markets. Costs matter because they reduce the return you keep. Expense ratios, trading fees, advisory fees, and tax costs may seem small individually, but they can compound over time. The more you pay in unnecessary costs, the less money is invested for your future. Frequent trading can also add costs and create tax consequences in taxable accounts. A simple, low-cost strategy followed consistently is generally more effective than a complex one that’s expensive to maintain. Where you invest can matter as much as what you invest in. A 401(k), traditional IRA, Roth IRA, and taxable brokerage account all have different tax rules, contribution limits, and withdrawal restrictions. If your employer offers a retirement plan with a match, that can be a strong place to start because the match is part of your compensation. Roth accounts may be useful for investors who expect tax-free withdrawals to be valuable later. Taxable brokerage accounts can offer flexibility for goals that do not fit inside retirement accounts. The right account depends on your goal, timeline, and tax situation. Stock investing rewards patience more than prediction. Short-term price movements can be noisy, emotional, and difficult to interpret. Long-term investing focuses on business growth, compounding, and disciplined behavior. This does not mean you should ignore your portfolio. It means you should avoid reacting to every headline. Markets will decline at times. Some investments will disappoint. A long-term mindset helps you stay focused on the reason you invested in the first place. Again: time in the market is better than timing the market. Even strong companies can struggle. A business may face competition, regulatory pressure, weak earnings, management problems, or changing consumer demand. If too much of your portfolio is tied to a single company, one bad outcome can cause significant damage. This risk is especially important if you own stock in your employer. In that case, your paycheck and investments may depend on the same company. Diversification reduces the risk that a single business causes a major setback in your financial plan. Yes, market declines are uncomfortable, but they’re normal. The mistake is turning temporary fear into a permanent loss by selling without a plan. When investors panic, they often sell after prices have already fallen and hesitate to reinvest until prices have recovered. A better approach is to revisit your goals, timeline, and risk tolerance before making major changes. If your long-term plan is still intact, a downturn may not require action. Sometimes the hardest part of investing is doing nothing when emotions are high. Keep your cool. While investing isn’t set-it-and-forget-it, it’s also not something that should be driven by every market headline, price swing, or short-term fear. Regularly review and revisit your plan, but don’t be reactive. Trading and investing are not the same thing. Trading focuses on short-term price movements. Investing focuses on long-term ownership and value creation. Both involve risk, but they require different skills and mindsets. Beginners often run into trouble when they treat investing like a game of constant buying and selling. Frequent moves can increase costs, taxes, and emotional decision-making. If your goal is long-term wealth building, your strategy should reflect that. You do not need to react to every price change to be an investor. This means deciding how much of your portfolio should be in stocks, bonds, cash, or other assets. Your allocation should reflect your goals, timeline, and risk tolerance. Someone investing for a goal 30 years away may choose more stock exposure because they have time to ride out volatility. Someone who needs the money soon may need more stability. The point is not to copy another person’s allocation. The point is to choose one that fits your situation. Consistency is key. Your regular investment could be a percentage of income, a fixed monthly amount, or automatic contributions through a workplace retirement plan. The amount does not have to be perfect at first. What matters is building a repeatable habit. You can increase contributions as your income grows, debt decreases, or your budget becomes more flexible. Discipline is more important than starting with a large amount. Over time, your portfolio may drift away from your intended allocation. If stocks perform well, they may become a larger share of your portfolio than you originally planned. If stocks decline, your portfolio may become more conservative than intended. Rebalancing means bringing your portfolio back in line with your target allocation. This doesn’t need to happen constantly. A periodic review, such as once or twice a year, can help you manage risk without encouraging unnecessary trading. The goal is to stay aligned with your plan. Stock investing shouldn’t be complicated. The basics are straightforward: understand what stocks are, know why they carry risk, diversify, invest consistently, and think long term. The best tip isn’t finding the next hot stock. It’s about building a disciplined system you can follow through different market conditions. For most investors, patience, diversification, low costs, and consistent contributions matter more than prediction. If you’re unsure how to build a portfolio that fits your goals, risk tolerance, and time horizon, consider consulting a financial advisor or investment professional. Their help can be invaluable as you build your investment portfolio. With consistency and a strategic approach, stock investing becomes less about guessing and more about building wealth over time.Stock Investing: Overview

What Is Stock Investing?

How Investors Make Money From Stocks

Why Stocks Come With Risk

Stocks vs Stock Funds

Why Time Horizon Matters

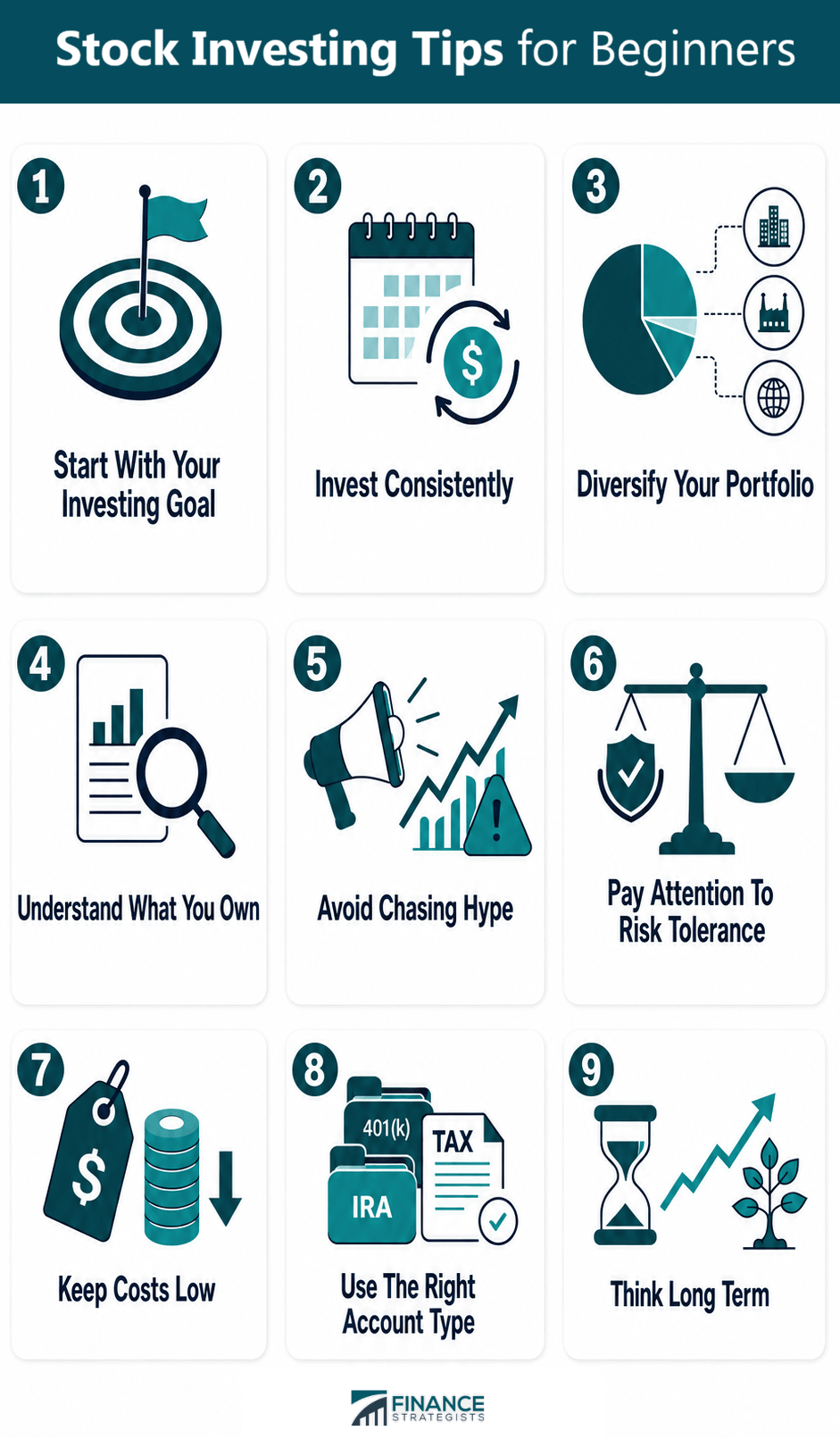

Stock Investing Tips For Beginners

Start With Your Investing Goal

Invest Consistently

Diversify Your Portfolio

Understand What You Own

Avoid Chasing Hype

Pay Attention to Risk Tolerance

Keep Costs Low

Use The Right Account Type

Think Long Term

Common Stock Investing Mistakes To Avoid

Putting Too Much Money In One Stock

Panic Selling

Confusing Trading With Investing

How to Build a Simple Stock Investing Plan

Choose A Target Allocation

Decide How Much to Invest Regularly

Review and Rebalance

Conclusion

Tips on Stock Investing FAQs

You can start with a small amount, especially if your brokerage allows fractional shares. The more important step is building the habit of investing consistently.

Stock investing always involves risk, but beginners can reduce risk by diversifying, investing for the long term and avoiding speculative trades.

You may be better served by starting with index funds because they offer broad diversification. Individual stocks require more research and carry more company-specific risk.

You should review your portfolio periodically, such as quarterly or annually, but avoid checking so often that short-term market moves lead to emotional decisions.

Yes. Stock prices can fall, and returns are not guaranteed. That is why it is important to invest based on your goals, time horizon, and risk tolerance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.