Microeconomics delves into the specific decisions of individuals and firms within the marketplace, offering a focused lens into how they navigate supply, demand, and market structures. This discipline underscores the choices made when faced with scarcity, shedding light on individual behaviors rather than broader economic trends. Its insights inform both policymakers and businesses, paving the way for informed economic policies and strategic decisions. By breaking down complex market behaviors into smaller, digestible segments, microeconomics equips analysts with tools to understand and predict market shifts. This understanding is pivotal for crafting policies and guiding business strategies, emphasizing its real-world relevance and importance. Microeconomics introduces several foundational concepts that anchor economic thought. These principles, which include the likes of opportunity cost, diminishing returns, and rational behavior, offer a structured lens to decode market dynamics. Without these fundamentals, the complexities of market behavior would remain an enigma, elusive to even the keenest minds. Furthermore, these concepts aren't just theoretical cornerstones; they find practical application in daily life. For instance, businesses frequently wrestle with opportunity costs when deciding on investment opportunities. Consumers, whether they realize it or not, often grapple with the idea of diminishing returns when making purchasing decisions, such as whether to eat that additional slice of pizza or buy an extra pair of shoes. The tug of war between supply and demand stands central to market economics. This ever-present dynamic dictates not only prices but also the production and consumption patterns of goods and services. When demand surges, prices often rise, encouraging producers to supply more. Conversely, when demand wanes, prices might drop, signaling producers to reduce output. Moreover, the interplay of supply and demand is inherently dynamic, perpetually adjusting to external influences, from technological innovations to governmental policies. For businesses, understanding this fluid dance means better forecasting and profitability. For consumers, it shapes purchasing decisions and budgets. In essence, this law orchestrates the rhythm of the market. At its core, elasticity measures the sensitivity of demand or supply to changes in price or other economic variables. A product with high elasticity sees significant shifts in quantity demanded or supplied with even minimal price changes. In contrast, inelastic products remain relatively stable despite price fluctuations. Understanding this is pivotal for businesses, as it impacts pricing strategies, revenue projections, and overall profitability. Moreover, elasticity isn't just limited to price; it encompasses various facets like income elasticity (how demand changes with income variations) or cross-price elasticity (how the demand for one good changes with the price change of another). This multidimensionality of elasticity offers rich insights, allowing businesses and policymakers to predict market reactions to a host of changes, be it a tax imposition, a competitor's pricing move, or broader economic shifts. Every choice has repercussions, and marginal analysis seeks to understand the implications of one more or one less—be it producing one more unit, hiring an additional worker, or consuming an extra item. It's this focus on the 'additional' that allows businesses and individuals to optimize decision-making, ensuring maximum utility or profit. For a business, understanding the marginal cost (additional cost) and marginal benefit (additional revenue) of producing one more unit can dictate whether to ramp up production or dial it down. For consumers, the marginal utility of consuming one more unit guides purchasing decisions. This incremental perspective, grounded in microeconomics, often paves the way for optimal outcomes in various economic scenarios. Utility, in essence, is the satisfaction or happiness derived from consuming a good or service. It's this pursuit of utility that often guides consumers in their market choices. However, deciphering utility isn't straightforward, as it's a subjective measure and varies from individual to individual. What brings immense satisfaction to one might be utterly inconsequential to another. Beyond the intrinsic value of a product, several external factors, such as societal norms, peer influence, and marketing campaigns, can shape perceived utility. When product prices change, they can impact the purchasing power of consumers and might lead to shifts in consumption patterns. The income effect reflects how price changes, by influencing real income, alter the quantity demanded of a good. The substitution effect, on the other hand, kicks in when consumers replace a now relatively more expensive product with a cheaper alternative. These two effects, often intertwined, play a crucial role in shaping market dynamics. For businesses, predicting these shifts can be the difference between retaining market share during price changes or ceding ground to competitors. For policymakers, understanding these effects can guide taxation and subsidy decisions, ensuring that they align with broader economic goals. Consumer surplus is the economic term for the difference between what consumers are willing to pay for a product or service and what they actually end up paying. It's a measure of the net benefit derived by consumers from market transactions. In essence, it's the economic windfall that consumers enjoy when the market price is below their maximum willingness to pay. For businesses, tapping into this surplus can offer lucrative opportunities. Whether it's through dynamic pricing strategies, segmented market offerings, or promotional campaigns, businesses often aim to capture a portion of this surplus. For policymakers, consumer surplus serves as an indicator of market efficiency and can influence decisions ranging from trade policies to regulatory frameworks. For producers, the costs of production are a constant preoccupation. Beyond the obvious elements like raw materials and wages, various other factors, from technological advancements to regulatory environments, can influence these costs. A spike in global oil prices, for instance, might inflate transportation costs, impacting multiple industries. In an interconnected global economy, these cost variables are in perpetual flux. For businesses, navigating these shifts effectively is crucial for maintaining profitability. Cost-efficient production not only ensures competitive pricing but also fortifies a firm's market position, enabling it to weather economic downturns and capitalize on booms. Every commercial entity's end game is profit maximization. However, this objective isn't just about boosting revenues; it's also about astute cost management, risk mitigation, and forward-thinking investments. While short-term gains can offer immediate rewards, businesses often need to balance these with long-term strategies to ensure sustained profitability. This equilibrium between immediate and future gains demands meticulous planning and agility. Whether it's investing in research and development, entering new markets, or innovating product lines, businesses must make calculated moves, always with an eye on the overarching goal of profit maximization. The production function encapsulates the relationship between inputs (like labor and capital) and outputs (goods or services). It's the blueprint that dictates how businesses transform resources into sellable products. An efficient production function ensures that resources are utilized optimally, minimizing waste and maximizing output. In today's competitive landscape, fine-tuning the production function is not just an operational necessity; it's a strategic imperative. Leveraging technology, adopting lean methodologies, and continuous process improvements can elevate a firm's production function, offering it a competitive edge. Such efficiencies not only translate to cost savings but also enable rapid market responsiveness, a critical factor in today's dynamic market environments. Perfect competition is an idealized market structure where numerous firms offer identical products, and no single entity can influence market prices. Consumers, in this scenario, enjoy the most considerable choice and price benefits, given the fierce competition among producers. For businesses, operating in such a market demands a relentless focus on cost efficiencies, as prices—and consequently profit margins—are often wafer-thin. However, while perfect competition offers a theoretical benchmark, real-world markets rarely mirror this ideal. Yet, its principles provide valuable insights. Understanding how prices, outputs, and profits would behave in a perfectly competitive setup offers a reference point against which real market behaviors can be analyzed and understood. A monopoly exists when a single firm dominates the market, either due to unique capabilities, ownership of a key resource, or regulatory support. This singular control often affords the monopolistic firm significant pricing power, enabling it to set prices that maximize profits. For consumers, this might mean fewer choices and potentially higher prices. However, monopolies aren't necessarily nefarious. In some instances, they can drive innovation. Given their secure market position and significant resources, monopolies might invest heavily in research and development, introducing groundbreaking products or solutions. Nonetheless, unchecked monopolistic power can lead to consumer exploitation, necessitating regulatory oversight to ensure market fairness. Monopolistic competition offers a middle ground between perfect competition and monopoly. Here, several firms offer products that are similar but not identical. This differentiation, often a result of branding, quality variations, or other factors, allows firms a degree of pricing power. For consumers, it offers a blend of choice and variety. In such a market, branding, and advertising become paramount. Firms continually strive to distinguish their offerings, seeking to carve a niche and foster brand loyalty among consumers. This constant endeavor to differentiate, while competitive, often spurs innovation, benefiting consumers with varied and improved product choices. In an oligopolistic market, a handful of firms dominate, wielding significant market power. Their decisions, from pricing to production, often hinge on anticipated reactions from competitors. It's a market characterized by interdependence, where collaborative tendencies (like forming cartels) might coexist with fierce competition. Navigating an oligopolistic market demands strategic acumen. Firms must continually anticipate competitor moves, devising strategies that not only cater to consumers but also counter potential threats from rival firms. For consumers, oligopolies can offer benefits in terms of product innovations and choices, but there's also the risk of collusive behaviors leading to higher prices. In the intricate ballet of the market, prices pirouette to the tunes of supply and demand. Microeconomics, with its focus on individual market agents, offers the tools to understand this dance in depth. It sheds light on how producers and consumers, with their respective costs, utilities, and expectations, arrive at a price that both can agree upon. However, price determination isn't solely a function of market forces. External factors—be it government regulations, technological breakthroughs, or global events—can influence this equilibrium. For businesses, mastering the art of price determination can enhance profitability. For policymakers, it provides the insights needed to ensure market fairness and stability. Production isn't merely about manufacturing goods; it's about optimizing resources to maximize output. Microeconomics delves deep into this realm, exploring how firms can best utilize inputs to yield the most favorable results. From understanding the nuances of the production function to grappling with cost structures, it offers a comprehensive toolkit for businesses. Furthermore, in a world increasingly conscious of sustainability, production isn't just about quantity; it's also about quality. Microeconomics, by spotlighting the nitty-gritty of production processes, can guide firms in crafting sustainable, efficient, and profitable production strategies. At the heart of the market lies the consumer, and microeconomics, with its granular lens, seeks to understand this entity. It probes into the myriad factors that shape consumer choices, from income levels to societal trends. By dissecting these influences, it offers valuable insights into market demands, allowing businesses to tailor their offerings more effectively. Beyond consumption patterns, microeconomics also delves into consumer welfare. It assesses how market transactions, policies, and structures impact the well-being of the individual consumer. Such insights are invaluable for policymakers, ensuring that regulations and initiatives enhance, rather than impede, societal welfare. Countries, much like individuals, have strengths. Some nations are better at producing wine, others excel in technology. This idea is captured by the principle of comparative advantage, which suggests that nations should produce what they're most efficient at and trade for the rest. It's the bedrock of international trade, arguing for specialization and exchange to maximize global output. Yet, despite the apparent advantages, not all sectors within a country benefit equally from trade. This disparity has led to debates around protectionism and trade barriers. To protect local industries, countries might implement tariffs, quotas, or other barriers. While these can shield local jobs and businesses in the short term, they might lead to inefficiencies or trade wars in the long run. Protectionism can be a double-edged sword. On one hand, it safeguards domestic industries from fierce international competition, allowing them to grow and mature. On the other hand, consumers often face higher prices, and retaliatory measures from other countries can hamper exports. Trade agreements, like NAFTA or the EU's Single Market, aim to foster smoother trade between nations by reducing barriers. These pacts can boost economies by opening up new markets, promoting competition, and encouraging efficiency. However, they also have distributional effects, benefiting some sectors while challenging others. Microeconomics plays a crucial role in assessing these agreements. By breaking down complex economic interactions into understandable bits, it offers policymakers the insights they need to navigate the turbulent waters of global trade. Whether it's assessing tariffs' impact or understanding how quotas might affect supply chains, microeconomics remains an indispensable tool in the world of international commerce. Microeconomics studies the behavior of individual economic units, encompassing households, firms, and markets. It dives into decision-making processes, price determination, and how supply aligns with demand. Beyond everyday transactions, microeconomics offers pivotal insights into public policy, welfare economics, and global trade. It assesses societal well-being through concepts like Pareto Efficiency and addresses market inefficiencies using tools like taxes and regulations. Moreover, it helps stakeholders understand the implications of tariffs and trade agreements. Overall, microeconomics isn't merely theoretical; it's an essential tool offering nuanced insights, guiding policymakers and business leaders in our dynamic economic landscape.What Is Microeconomics?

Principles of Microeconomics

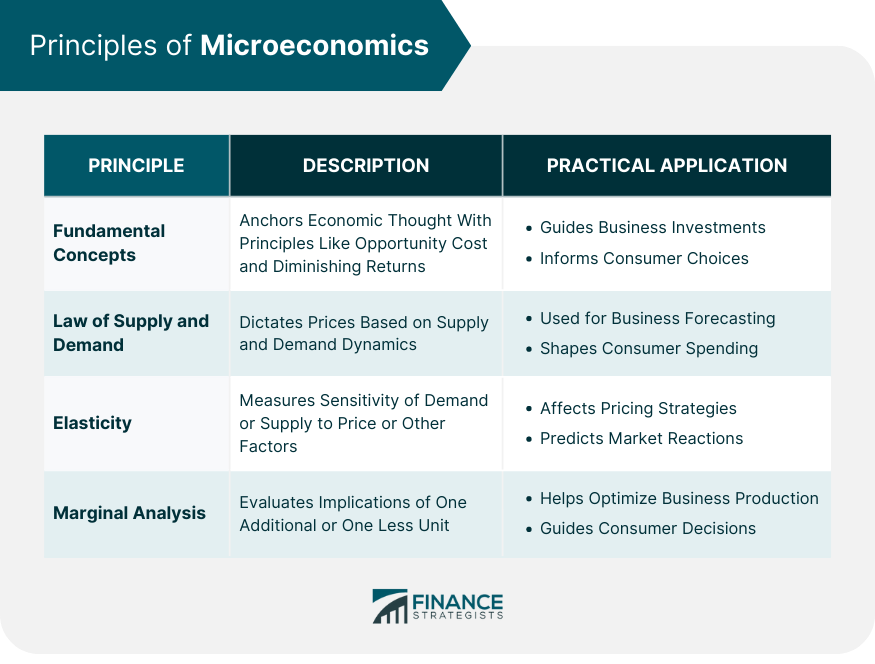

Fundamental Concepts

Law of Supply and Demand

Elasticity

Marginal Analysis

Factors Influencing Consumer Behavior in Microeconomics

Utility and Satisfaction

Income and Substitution Effects

Consumer Surplus

Factors Influencing Producer Behavior in Microeconomics

Costs of Production

Profit Maximization

Production Function

Market Structures of Microeconomics

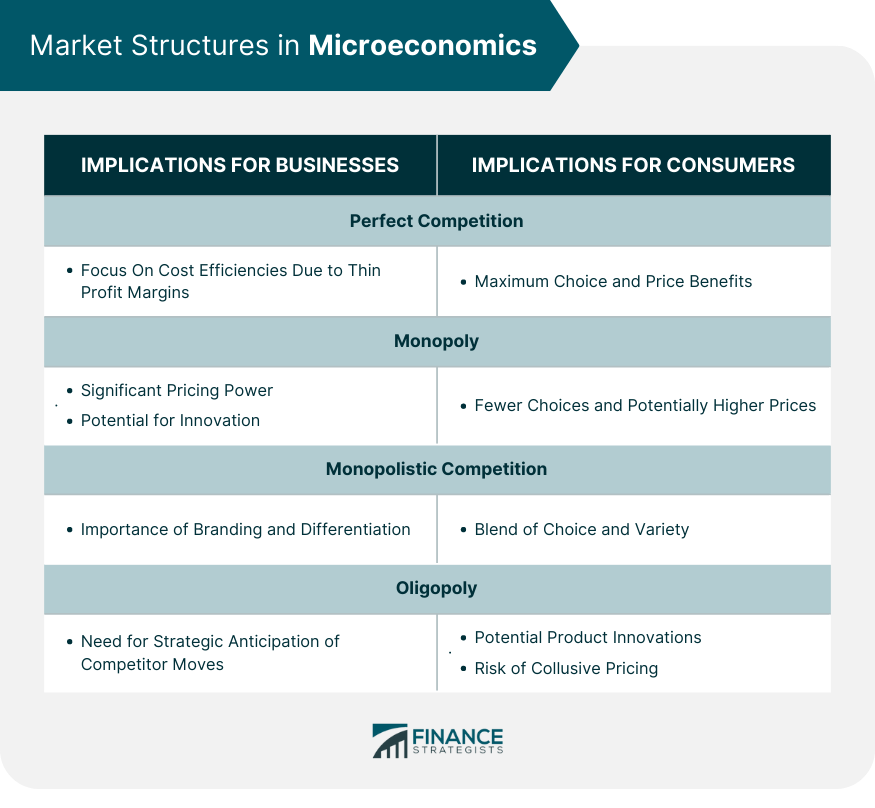

Perfect Competition

Monopoly

Monopolistic Competition

Oligopoly

Uses of Microeconomics

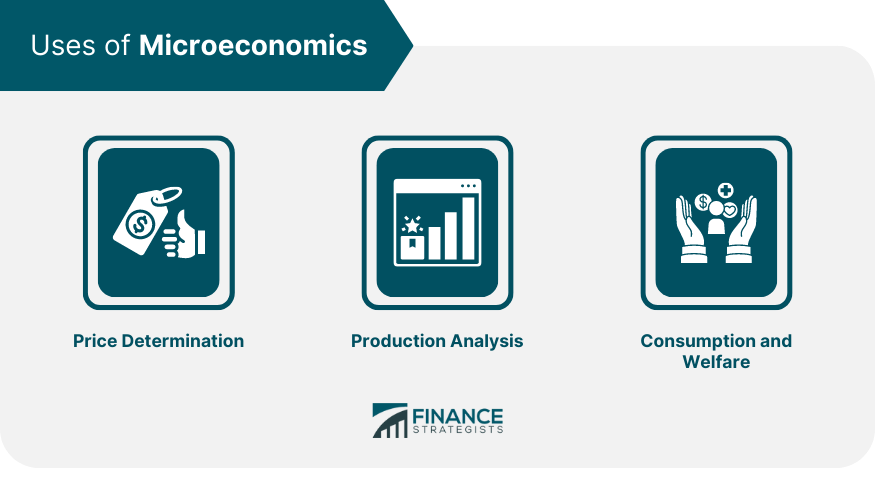

Price Determination

Production Analysis

Consumption and Welfare

Role of Microeconomics in Global Trade

Comparative Advantage and Trade

Protectionism and Trade Barriers

Economic Effects of Trade Agreements and Policies

Final Thoughts

Microeconomics FAQs

Microeconomics studies individual economic units like consumers and firms, examining how they make decisions and interact in markets.

Microeconomics studies individual units like households and firms, while macroeconomics examines whole economies, focusing on aspects like inflation and GDP.

The primary market structures include perfect competition, monopoly, monopolistic competition, and oligopoly, each with distinct characteristics.

Microeconomics utilizes supply and demand principles, along with external factors, to understand and predict price levels in the market.

By analyzing costs of production, profit maximization, and the production function, microeconomics offers insights into efficient and effective business strategies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.