A frozen plan is a type of retirement plan that has been closed to new participants or new contributions. This can occur due to various reasons such as financial instability, merger, and acquisition, or changing business priorities. Existing employees may still participate in the plan, but new employees are not allowed to enroll. A frozen plan can include pension plans, retirement plans, or investment plans. A pension plan is a retirement plan where the employer contributes a specific amount to an employee's retirement account. A frozen pension plan is one that has been closed to new participants or new contributions. A retirement plan is an account set up by an employer to help employees save for their retirement. A frozen retirement plan is one that has been closed to new participants or new contributions. An investment plan is a type of plan that helps employees invest their money in various investment vehicles, such as stocks, bonds, and mutual funds. A frozen investment plan is one that has been closed to new participants or new contributions. A frozen retirement plan is a type of retirement plan that has been closed to new participants, but still maintains benefits for those who were already enrolled in the plan prior to its closure. In a frozen retirement plan, the employer may choose to stop making contributions to the plan or stop allowing employees to make contributions, but the plan is still maintained and managed by the plan administrator. The benefits earned by employees who were enrolled in the plan before it was frozen are still protected and preserved, but no new benefits are accrued. There are two general types of frozen retirement plans: frozen defined benefit plans and frozen defined contribution plans. A frozen defined benefit plan is a type of pension plan where the employer promises to pay a specific benefit to the employee upon retirement, based on a formula that takes into account the employee's years of service and salary history. In a frozen defined benefit plan, the benefit formula is still applied to the employee's years of service and salary earned up to the point the plan was frozen, but no additional benefits are accrued. A frozen defined contribution plan, on the other hand, is a retirement plan where the employer makes contributions to the employee's account, which is invested and grows over time. In a frozen defined contribution plan, the employer may choose to stop making contributions to the plan, but the employee's account balance is still preserved and can continue to grow based on investment returns. It's important to note that although a retirement plan may be frozen, it doesn't necessarily mean that it's terminated or that benefits are lost. In some cases, frozen plans may be merged with other plans or terminated at a later date. A company may freeze its plans due to financial instability or a decline in business revenue. A frozen plan can help the company cut costs and protect the retirement benefits of existing employees. A company may freeze its plans due to a merger or acquisition. In such cases, the new company may want to integrate its existing retirement plans with the acquired company's plans. A company may freeze its plans due to changing business priorities, such as a shift in focus to a new business line or a change in corporate strategy. A frozen plan can have a significant impact on employees. Existing employees may be limited in their ability to contribute to their retirement accounts, and new employees may not have access to the plan. In addition, employees may have limited investment options and may not receive future benefit increases. A frozen plan can help an employer reduce its retirement plan costs, but it can also create administrative burdens. Employers may have to manage two or more plans if they merge with another company, and they may have to comply with additional regulations if they freeze their plans. A frozen plan can have significant financial implications for both employees and employers. Employees may have to rely on other retirement plans or investments to achieve their retirement goals, while employers may have to pay additional fees for managing multiple plans. Transfer Options: A frozen plan participant may have the option to transfer their retirement account to another plan. The transfer may be a tax-free transaction, and the participant can continue to grow their retirement savings. Rollover Options: A frozen plan participant may have the option to roll over their retirement account to an IRA. This can provide more investment options and more control over the retirement account. Withdrawal Options: A frozen plan participant may have the option to withdraw their retirement account funds. However, this can result in significant taxes and penalties, and it may not be the best option for long-term retirement savings. Frozen plans are subject to various governmental regulations, including the Employee Retirement Income Security Act (ERISA). Employers must comply with these regulations to protect the retirement benefits of their employees. Plan sponsors are responsible for managing the frozen plan and ensuring compliance with regulations. They must provide regular updates to participants and provide them with transfer and rollover options. Employees have certain protections under ERISA, including the right to receive a summary plan description and the right to request plan documents. In addition, employees have the right to sue for benefits if they feel their benefits have been unfairly denied or if the plan sponsor has breached their fiduciary duty. Frozen plans can have a significant impact on both employers and employees. While freezing a plan can help employers reduce costs, it can limit employees' ability to save for retirement and create administrative burdens. Participants in a frozen plan have various options, including transferring or rolling over their retirement account. Employers must comply with various regulations to protect their employees' retirement benefits. In conclusion, understanding frozen plans' various aspects is essential for both employers and employees to make informed decisions about their retirement planning.What Is Frozen Plan?

Types of Frozen Plan

Pension Plan

Retirement Plan

Investment Plan

How Does Frozen Retirement Plan Work?

Reasons for Freezing a Plan

Financial Instability

Merger and Acquisition

Changing Business Priorities

Effects of Frozen Plan

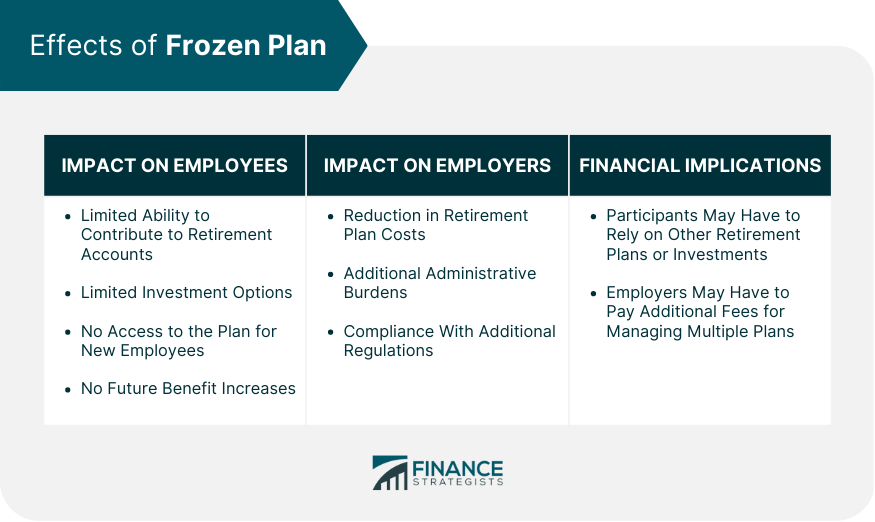

Impact on Employees

Impact on Employers

Financial Implications

Options for Frozen Plan Participants

Frozen Plan Compliance and Regulations

Governmental Regulations

Plan Sponsor Responsibilities

Employee Protections

Final Thoughts

Frozen Plan FAQs

A frozen plan is a retirement plan that has been closed to new participants or new contributions. It can occur in the form of a pension plan, retirement plan, or investment plan due to various reasons such as financial instability, merger, and acquisition, or changing business priorities.

A frozen plan can have a significant impact on both employers and employees. Existing employees may be limited in their ability to contribute to their retirement accounts, and new employees may not have access to the plan. Employers may have to manage two or more plans if they merge with another company, and they may have to comply with additional regulations if they freeze their plans.

Yes, frozen plan participants may have the option to transfer their retirement account to another plan. The transfer may be a tax-free transaction, and the participant can continue to grow their retirement savings.

Frozen plans are subject to various governmental regulations, including the Employee Retirement Income Security Act (ERISA). Employers must comply with these regulations to protect the retirement benefits of their employees.

Yes, freezing a retirement plan can help employers reduce their retirement plan costs. However, this can create administrative burdens, and they may have to manage two or more plans if they merge with another company.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.