A home equity line of credit (HELOC) may be a good idea depending on your circumstances and purpose for applying. By taking out a HELOC, you are putting your home at risk if you default, so it is important to be sure you can pay. Generally speaking, home improvements are the best use of a HELOC. Unlike a traditional mortgage, which provides a lump sum of money upfront, a home equity line of credit provides access to a revolving line of credit that can be used for a variety of purposes. While a HELOC can provide homeowners with financial flexibility and potentially lower interest rates than other forms of borrowing, there are also some potential drawbacks to consider before deciding whether it's a good idea for your financial situation. A home equity line of credit is a type of loan that allows homeowners to borrow money against the equity they have built up in their homes. Equity is the difference between the current market value of the home and the amount of money still owed on the mortgage. For example, if a homeowner's home is currently worth $300,000 and they owe $200,000 on their mortgage, they have $100,000 in equity. A HELOC allows homeowners to borrow against this equity, using their home as collateral for the loan. The amount that can be borrowed depends on the value of the home, the amount of equity the homeowner has built up, and the lender's policies. With a HELOC, the borrower can draw on the line of credit as needed, up to the maximum amount allowed by the lender. Interest is only charged on the amount borrowed, not on the entire line of credit. A HELOC works like a credit card in that the borrower can use the line of credit as needed, up to the maximum amount allowed by the lender. The borrower only pays interest on the amount borrowed, and the interest rate may be variable or fixed. The borrower can make payments on the principal and interest as they would with a traditional loan, or they can pay only the interest each month and pay off the principal at the end of the loan term. A HELOC typically has a draw period, during which the borrower can use the line of credit, and a repayment period, during which the borrower must pay back the principal and interest. The draw period can last several years, and the repayment period can be several years or decades. At the end of the repayment period, the borrower must pay back the entire amount borrowed, or the loan may be extended or converted to a traditional mortgage. A HELOC is different from other forms of borrowing, such as a traditional mortgage or personal loan, in several ways. First, a HELOC is a revolving line of credit, which means the borrower can use the line of credit as needed, up to the maximum amount allowed by the lender. With a traditional mortgage or personal loan, the borrower receives a lump sum of money upfront and must make payments on the entire amount borrowed. Second, a HELOC is secured by the borrower's home, while a personal loan is typically unsecured. This means that if the borrower defaults on the loan, the lender can foreclose on the home to recover their money. With a personal loan, the lender may have to go to court to recover their money if the borrower defaults. Below are some of the advantages of a HELOC: One of the main advantages of a HELOC is that it often has lower interest rates than other forms of borrowing, such as credit cards and personal loans. Because the loan is secured by the borrower's home, the lender is taking less risk and can offer lower interest rates. This can save borrowers a significant amount of money in interest charges over the life of the loan. Another advantage of a HELOC is that it offers flexible borrowing options. Borrowers can draw on the line of credit as needed, up to the maximum amount allowed by the lender. This means that borrowers can borrow only what they need, rather than being forced to take out a lump sum of money upfront. Additionally, borrowers can pay back the principal and interest as they would with a traditional loan, or they can pay only the interest each month and pay off the principal at the end of the loan term. This flexibility can be useful for borrowers who have unpredictable or fluctuating expenses. Another potential advantage of a HELOC is that the interest paid on the loan may be tax-deductible. This is because the loan is secured by the borrower's home, making it a type of mortgage interest. However, there are limitations on the amount of interest that can be deducted, and borrowers should consult with a tax professional to determine their eligibility for this deduction. Finally, taking out a HELOC can potentially increase the value of the borrower's home. This is because home renovations and improvements funded by a HELOC can increase the home's value, making it more attractive to potential buyers if the homeowner decides to sell in the future. Below are some of the disadvantages of a HELOC: One potential disadvantage of a HELOC is that the interest rate may be variable. This means that the interest rate can fluctuate over the life of the loan, potentially increasing the borrower's monthly payments. While some lenders offer fixed-rate HELOCs, they may come with higher interest rates than variable-rate loans. Another potential disadvantage of a HELOC is that it is secured by the borrower's home. This means that if the borrower defaults on the loan, the lender can foreclose on the home to recover their money. While this risk is relatively low if the borrower is able to make their payments on time, it is important to understand that taking out a HELOC does put the borrower's home at risk. Like any loan, a HELOC may come with fees and charges, such as origination fees, appraisal fees, and annual fees. These fees can add up over the life of the loan, and borrowers should be aware of them when considering whether to take out a HELOC. Finally, taking out a HELOC can create a temptation to overspend. Because the line of credit is available for use as needed, it can be easy for borrowers to draw on the line of credit for expenses that they may not be able to afford otherwise. This can lead to a cycle of debt and financial stress, particularly if the borrower is not able to make their monthly payments on time. Before deciding whether to take out a HELOC, there are several factors that borrowers should consider, including: The amount of equity that the borrower has built up in their home will determine how much they are able to borrow with a HELOC. Borrowers should calculate their home's current value and subtract the amount they owe on their mortgage to determine their equity. Generally, lenders will allow borrowers to borrow up to 85% of their home's equity, although this can vary depending on the lender's policies. Like any loan, a HELOC will be impacted by the borrower's credit score and credit history. Borrowers with higher credit scores and a history of responsible borrowing are more likely to be approved for a HELOC and may qualify for lower interest rates. Borrowers with lower credit scores may still be able to qualify for a HELOC, but may face higher interest rates and less favorable terms. Borrowers should also consider their current and future financial situation before taking out a HELOC. If the borrower is already struggling with debt or has a low income, taking out a HELOC may not be a good idea. Similarly, if the borrower anticipates a change in income or expenses in the near future, such as a job loss or major life event, they should consider whether they will be able to make their monthly payments on the loan. Finally, borrowers should consider the purpose of their borrowing. While a HELOC can be used for a variety of purposes, such as home renovations or debt consolidation, it may not be the best option for all expenses. Borrowers should consider whether there are other forms of borrowing that may be more appropriate for their needs, such as a personal loan or credit card. While there are potential risks and drawbacks to taking out a HELOC, there are also several situations in which it may be a good idea, including: Taking out a HELOC to fund home renovations or improvements can be a smart investment, as it can increase the value of the home and make it more attractive to potential buyers if the homeowner decides to sell in the future. Consolidating high-interest debt, such as credit card debt, into a HELOC can be a smart financial move, as it can potentially save borrowers money in interest charges over the life of the loan. Finally, taking out a HELOC to fund education or other large expenses can be a good idea, as it can provide borrowers with access to a flexible line of credit that can be used as needed. While there are situations in which a HELOC can be a good idea, there are also situations in which it may not be the best option, including: Taking out a HELOC for short-term expenses, such as a vacation or holiday shopping, is generally not a good idea, as it can create a cycle of debt and financial stress. Taking out a HELOC to invest in the stock market or other risky investments is also not a good idea, as it can put the borrower's home at risk and may result in significant financial losses. Finally, taking out a HELOC for frivolous spending, such as shopping sprees or luxury purchases, is not a good idea, as it can lead to a cycle of debt and financial stress. If a HELOC is not the best option for a borrower's financial situation, there are several alternatives to consider, including: Personal loans are unsecured loans that can be used for a variety of purposes. While they may come with higher interest rates than HELOCs, they do not put the borrower's home at risk. Credit cards can be a useful form of borrowing for short-term expenses or emergencies. However, they often come with high interest rates and can lead to a cycle of debt if not used responsibly. Cash-out refinancing allows homeowners to refinance their mortgage and take out a lump sum of money at the same time. While this can be a good option for some borrowers, Cash-out refinancing can also come with higher interest rates and fees than a HELOC. An equity line of credit for homes can be a useful form of credit borrowing for homeowners who have built up equity in their homes and need access to flexible funds for expenses such as home renovations, debt consolidation, and education. However, it is important to weigh the potential advantages and disadvantages of a HELOC and consider factors such as equity in the home, credit score and history, and current and future financial situation before deciding whether to take out a HELOC. It is also important to consider alternative forms of borrowing, such as personal loans or credit cards, and to avoid taking out a HELOC for short-term expenses, risky investments, or frivolous spending. With careful consideration and responsible borrowing practices, a home equity line of credit can be a good option for homeowners who need access to funds and want to make smart financial decisions.Is a Home Equity Line of Credit a Good Idea?

What Is a Home Equity Line of Credit?

How Does a Home Equity Line of Credit Work?

How Is a Home Equity Line of Credit Different From Other Forms of Borrowing?

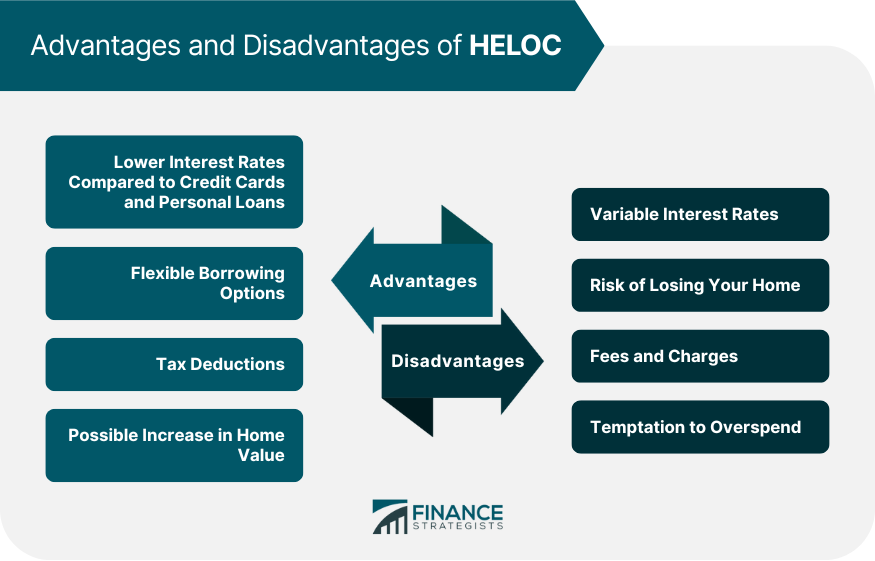

Advantages of a Home Equity Line of Credit

Lower Interest Rates

Flexible Borrowing Options

Tax Deductions

Possible Increase in Home Value

Disadvantages of a Home Equity Line of Credit

Variable Interest Rates

Risk of Losing Your Home

Fees and Charges

Temptation to Overspend

Factors to Consider Before Taking Out a Home Equity Line of Credit

Equity in the Home

Credit Score and History

Current and Future Financial Situation

Purpose of Borrowing

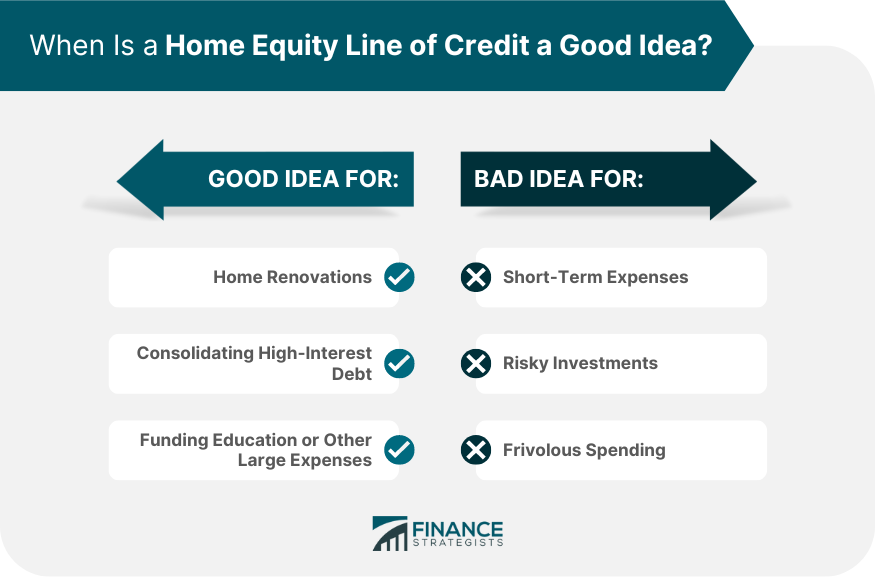

When Is a Home Equity Line of Credit a Good Idea?

Home Renovations

Consolidating High-Interest Debt

Funding Education or Other Large Expenses

When Is a Home Equity Line of Credit Not a Good Idea?

Short-Term Expenses

Risky Investments

Frivolous Spending

Alternatives to a Home Equity Line of Credit

Personal Loans

Credit Cards

Cash-Out Refinancing

The Bottom Line

Is Home Equity Line of Credit a Good Idea? FAQs

A home equity line of credit (HELOC) is a type of loan that allows homeowners to borrow money against the equity they have built up in their homes. Unlike a traditional mortgage, which provides a lump sum of money upfront, a HELOC provides access to a revolving line of credit that can be used for a variety of purposes.

The advantages of a HELOC include lower interest rates compared to credit cards and personal loans, flexible borrowing options, tax deductions, and the possibility of increasing the home value through renovations.

The disadvantages of a HELOC include variable interest rates, the risk of losing your home if you default on the loan, fees and charges, and the temptation to overspend.

Before taking out a HELOC, you should consider factors such as the equity in your home, your credit score and history, your current and future financial situation, and the purpose of borrowing.

A HELOC can be a good idea when used to fund home renovations, consolidate high-interest debt, or fund education or other large expenses. However, it is not a good idea for short-term expenses, risky investments, or frivolous spending.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.