A guaranteed income annuity (GIA) is a type of insurance product offered by insurance companies to provide a predictable and guaranteed stream of income to the annuity holder. It is often used as a financial tool for retirees or pre-retirees who want to ensure a steady flow of income during their retirement years. The main purpose of a GIA is to provide financial security and peace of mind for individuals during their retirement years. By offering a guaranteed income stream, GIAs help mitigate the risk of outliving one's savings and protect against market volatility. Investors who may consider a GIA include those who: Seek a predictable source of income during retirement Want to protect against longevity risk Desire to diversify their retirement income sources Prefer low-risk investment options Wish to minimize the impact of market fluctuations on their retirement income The primary feature of a GIA is the guaranteed income stream it provides. Once an individual purchases a GIA, the insurance company is contractually obligated to make regular payments to the annuity holder for the agreed-upon duration. Many GIAs offer the option of lifetime income, which ensures that the annuity holder receives regular payments for the rest of their life. This can provide a valuable safety net for retirees who may be concerned about outliving their savings. Alternatively, some GIAs provide income for a fixed period, typically ranging from 5 to 30 years. This option may be suitable for individuals who want to supplement their income for a specific duration, such as until another income source becomes available or to cover a predetermined expense. GIAs typically offer a variety of payment frequency options, including monthly, quarterly, semi-annual, or annual payments. Annuity holders can choose the frequency that best suits their financial needs and budgeting preferences. GIAs can be structured to cover either a single life or joint life. A single-life annuity provides income for the life of one individual, while a joint-life annuity continues payments for the lifetime of both annuitants, usually at a reduced rate after the first annuitant passes away. This option can help ensure that a surviving spouse continues to receive income after the first annuitant's death. Some GIAs offer an inflation protection feature, which increases the annuity payments periodically to help offset the impact of rising prices on purchasing power. This can be an essential consideration for individuals concerned about maintaining their standard of living during retirement. Insurance companies may offer various riders and additional benefits that can be added to a GIA to customize the product to an individual's specific needs. These may include features such as death benefits, long-term care benefits, or guaranteed minimum withdrawal benefits, among others. A single premium immediate annuity (SPIA) is a GIA that requires a one-time, lump-sum premium payment. In exchange, the insurance company begins making regular income payments immediately or within a short period, typically within one year. SPIAs are ideal for individuals who want to start receiving income right away and have a lump-sum available to invest. A deferred income annuity (DIA) is a GIA in which the annuity holder makes a lump-sum premium payment or a series of payments over time. The income payments start at a later, pre-determined date. The deferral period can range from several years to decades. DIAs are suitable for individuals who want to secure a guaranteed income stream in the future, often as a part of their retirement planning strategy. A qualified longevity annuity contract (QLAC) is a type of deferred income annuity specifically designed for use with qualified retirement plans, such as 401(k)s or traditional IRAs. QLACs can help individuals manage the required minimum distribution (RMD) rules associated with these accounts, as the purchase amount is excluded from the RMD calculation, and income payments are deferred until a later age, typically up to age 85. A variable annuity with guaranteed lifetime withdrawal benefit (GLWB) is a hybrid product that combines features of variable annuities and guaranteed income annuities. The annuity holder's premiums are invested in various investment options, allowing for potential growth. The GLWB rider guarantees a minimum income stream for life, regardless of investment performance, providing a level of income security. GIAs provide financial security by offering a predictable and guaranteed income stream, which can help retirees maintain their standard of living and cover essential expenses throughout retirement. GIAs can offer tax advantages, as the income payments are often partially or fully tax-deferred, depending on the type of annuity and the funding source. This can be particularly beneficial for individuals in higher tax brackets or those who expect to be in a lower tax bracket during retirement. By providing lifetime income options, GIAs help mitigate the risk of outliving one's savings, a significant concern for many retirees, especially as life expectancies continue to increase. GIAs remove the investment risk associated with market fluctuations, as the insurance company guarantees the income payments, regardless of market performance. GIAs can serve as an essential component of a diversified retirement income strategy, complementing other sources of income, such as Social Security, pensions, and investment portfolios. The steady and predictable income provided by GIAs can help retirees manage their budget effectively and plan for expenses more accurately. GIAs are generally considered to be illiquid investments, as withdrawing funds early may result in surrender charges and penalties. It is essential to consider one's liquidity needs before purchasing a GIA. GIAs generally offer lower potential returns than riskier investments, such as stocks or mutual funds. Individuals should carefully evaluate their risk tolerance and long-term financial goals before choosing a GIA. Fixed payment GIAs may not keep pace with inflation, which could erode the purchasing power of the income stream over time. It is crucial to consider inflation protection features when evaluating GIAs. The income payments from a GIA are dependent on the financial strength of the issuing insurance company. It is important to carefully research and choose a reputable, financially stable insurance company when considering a GIA. Withdrawing funds from a GIA may have tax implications, including possible tax penalties if withdrawals are made before the age of 59 ½. Understanding the tax consequences before making any withdrawals from a GIA is crucial. Before purchasing a GIA, it is essential to assess one's financial needs and goals, including retirement income needs, budgeting preferences, and risk tolerance. Selecting a reputable, financially stable insurance company is crucial when purchasing a GIA. Researching the insurance company's financial ratings, customer reviews, and complaint history can help ensure a sound investment. Different types of GIAs and riders may have different benefits and drawbacks, depending on an individual's specific financial goals and circumstances. Careful evaluation of product options and riders can help ensure that the GIA aligns with one's financial needs and goals. GIAs may have associated fees and charges, such as administrative fees, mortality and expense fees, and surrender charges. Understanding these fees and charges and their potential impact on the GIA's overall returns is essential. The GIA application process can take several weeks or even months, depending on the insurance company's requirements and processing times. It is crucial to allow sufficient time for the application and underwriting process when planning to purchase a GIA. Guaranteed Income Annuities (GIAs) offer retirees and pre-retirees a predictable and guaranteed income stream, which can provide financial security and peace of mind during their retirement years. GIAs also offer tax advantages, protection against outliving savings, and eliminate investment risk. However, GIAs come with risks and considerations that individuals should evaluate carefully, such as illiquidity and surrender charges, lower potential returns, and the credit risk of the issuing insurance company. Before purchasing a GIA, individuals should carefully assess their financial needs and goals, evaluate product options and riders, and understand the fees and charges associated with the product. Seeking the help of a professional insurance broker can also be beneficial in making sound investment decisions that align with one's financial goals and circumstances. What Is a Guaranteed Income Annuity (GIA)?

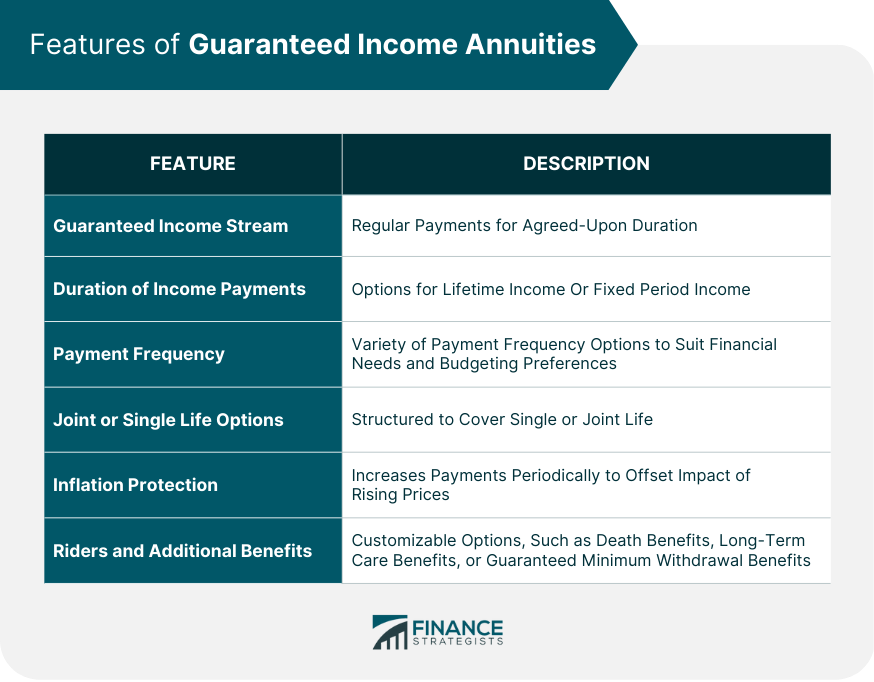

Features of Guaranteed Income Annuities

Guaranteed Income Stream

Duration of Income Payments

Lifetime Income

Fixed Period Income

Payment Frequency

Joint or Single Life Options

Inflation Protection

Riders and Additional Benefits

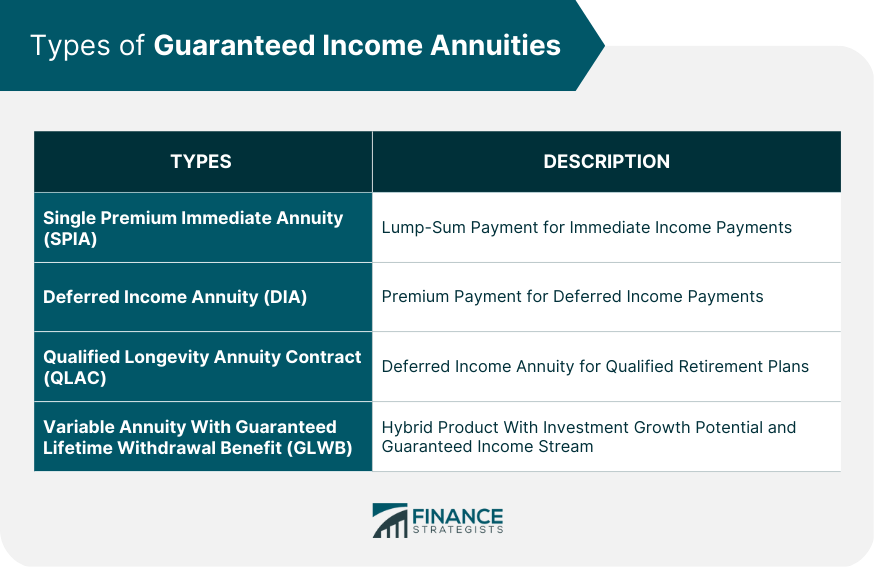

Types of Guaranteed Income Annuities

Single Premium Immediate Annuity (SPIA)

Deferred Income Annuity (DIA)

Qualified Longevity Annuity Contract (QLAC)

Variable Annuity With Guaranteed Lifetime Withdrawal Benefit (GLWB)

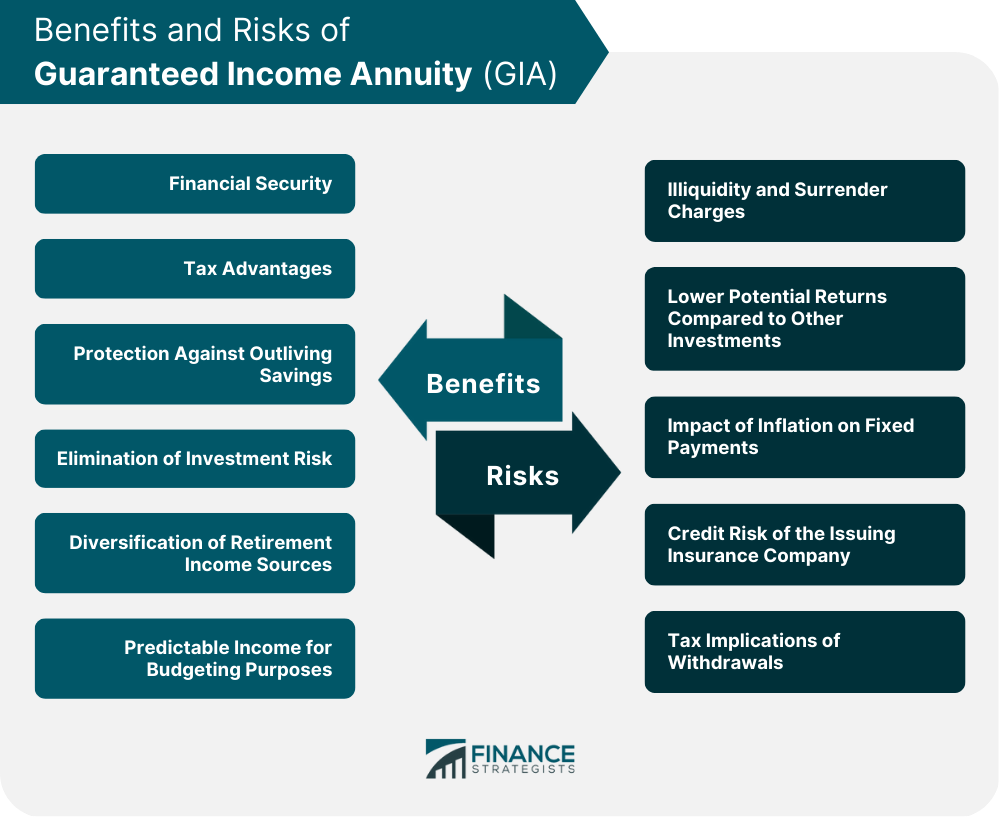

Benefits of a Guaranteed Income Annuity

Financial Security

Tax Advantages

Protection Against Outliving Savings

Elimination of Investment Risk

Diversification of Retirement Income Sources

Predictable Income for Budgeting Purposes

Risks and Considerations of a Guaranteed Income Annuity

Illiquidity and Surrender Charges

Lower Potential Returns Compared to Other Investments

Impact of Inflation on Fixed Payments

Credit Risk of the Issuing Insurance Company

Tax Implications of Withdrawals

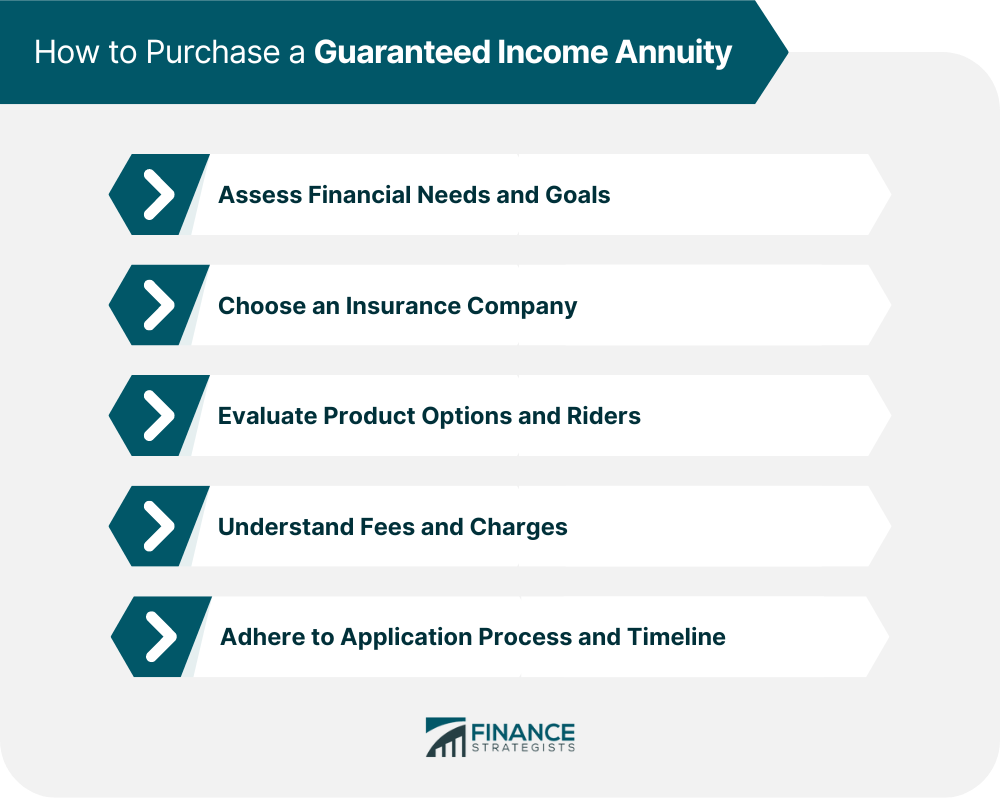

How to Purchase a Guaranteed Income Annuity

Assessing Financial Needs and Goals

Choosing an Insurance Company

Evaluating Product Options and Riders

Understanding Fees and Charges

Application Process and Timeline

Final Thoughts

Guaranteed Income Annuity (GIA) FAQs

A guaranteed income annuity (GIA) is an insurance product that provides a predictable and guaranteed stream of income to the annuity holder, often used as a financial tool for retirees or pre-retirees who want to ensure a steady flow of income during their retirement years.

Investors who may consider a GIA include those who seek a predictable source of income during retirement, want to protect against longevity risk, desire to diversify their retirement income sources, prefer low-risk investment options, and wish to minimize the impact of market fluctuations on their retirement income.

GIAs offer a guaranteed income stream, which can help retirees maintain their standard of living and cover essential expenses throughout retirement. By providing lifetime income options, GIAs help mitigate the risk of outliving one's savings, a significant concern for many retirees, especially as life expectancies continue to increase.

Yes, GIAs are generally considered to be illiquid investments, as withdrawing funds early may result in surrender charges and penalties. It is essential to consider one's liquidity needs before purchasing a GIA.

Individuals can purchase a GIA by assessing their financial needs and goals, choosing a reputable, financially stable insurance company, evaluating product options and riders, understanding fees and charges, and allowing sufficient time for the application and underwriting process. Seeking the help of a professional insurance broker can also be beneficial in making informed investment decisions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.