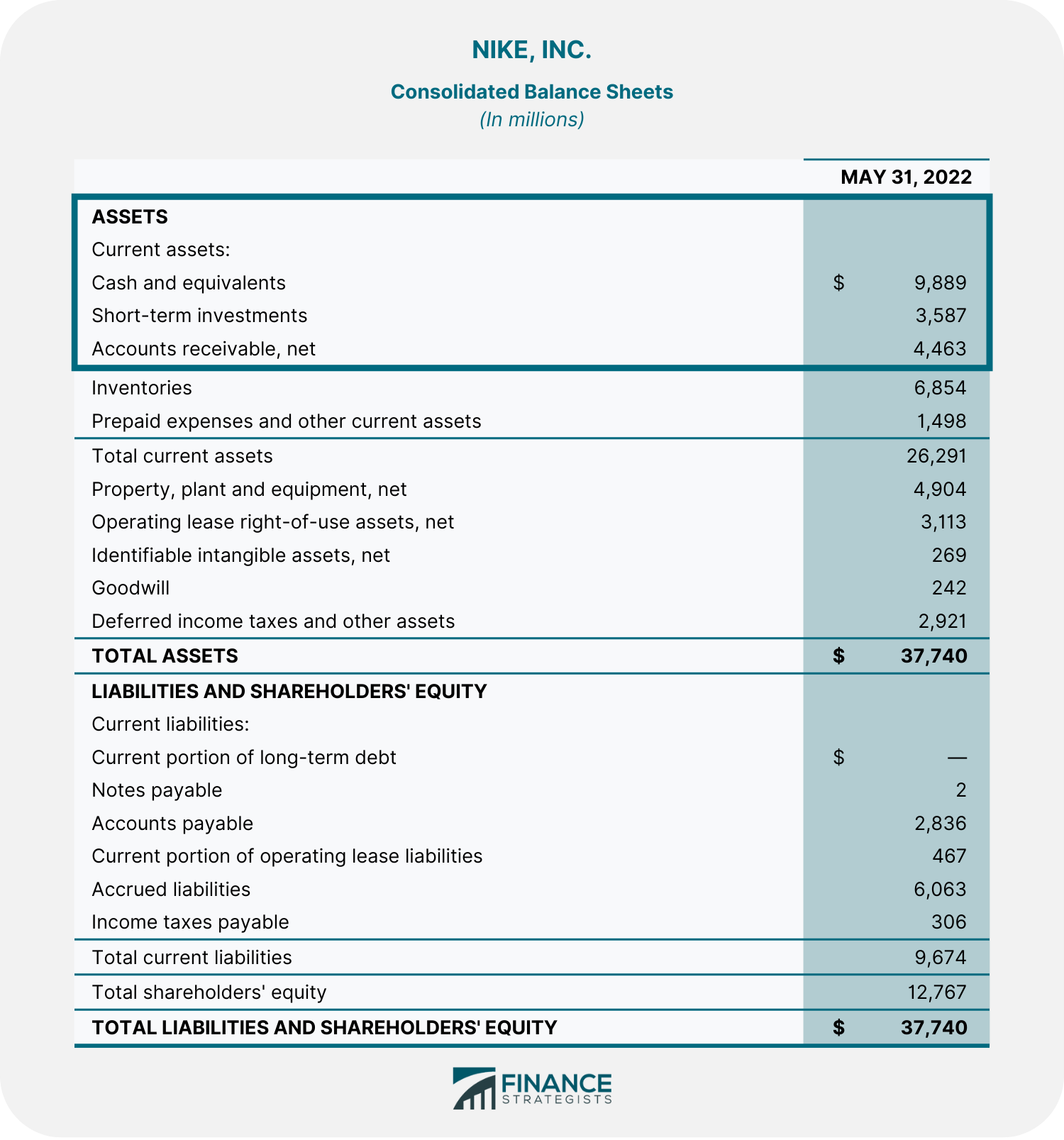

Quick assets are the most liquid assets that a company owns. These types of assets are either already in the form of cash or can easily be converted into cash within 90 days. Quick assets help finance day-to-day business operations. They can also provide businesses with a cushion against short-term financial instability. For instance, a company can use its quick assets to pay off its current liabilities. In businesses with unstable revenue and profit levels, keeping a large reserve of quick assets helps to cover any shortfalls. In contrast, businesses with stable cash flows may be able to maintain a good financial standing even with lesser quick assets on hand. When identifying their quick assets, companies consider the following components: Cash items include cash on hand, cash in the bank without restrictions on withdrawals, and working funds such as a petty cash fund or a change fund. On the other hand, cash equivalents are short-term, highly liquid investments that are readily convertible into cash. Some examples include treasury bills, treasury notes, money market funds, and commercial paper. Accounts receivable is the money that a company expects to receive from its customers after providing them goods or services on credit. Accounts receivable could also be considered as the invoices that customers have not yet paid. Once cash payments have been received for the invoices issued, the amount received is considered as part of the cash and equivalents component. Marketable securities are unrestricted short-term investments that can be easily sold, if needed. They are highly liquid because they can be converted to cash quickly, without losing any of their value. Some examples of marketable securities are stocks, bonds, ETFs, and preferred shares. Quick assets are most commonly calculated by adding cash and equivalents, accounts receivable, and marketable securities, such as in the formula below. Quick assets appear at the top of a balance sheet. They are arranged from most to least liquid. To illustrate, below is an example of Nike Inc.'s balance sheet as of May 31, 2021. The quick assets that can be found on the balance sheet of Nike, Inc. include cash and cash equivalents ($9,889,000), short-term investments ($3,587,000), and accounts receivable ($4,463,000). This means that the company’s quick assets reached a total of $17,939,000 as of May 31, 2021. The quick ratio or acid test ratio compares the quick assets of a company to its current liabilities. A company’s quick ratio indicates its short-term liquidity and ability to fulfill its short-term obligations using only its most liquid assets. The quick ratio is an important measure because the credit rating and reputation of a company can suffer if it is not able to meet its financial obligations. The quick ratio is calculated using the following formula: A ratio of 1.0 and above indicates that a company is in a reasonably liquid position. In such a case, the value of their quick assets would be enough to cover their current liabilities if needed. Companies with a ratio lower than 1.0 are less liquid. Thus, they might have to rely on alternative measures, such as increasing sales, to meet their current liabilities. Using the balance sheet of Nike presented above, let us calculate the company's quick ratio. The information needed from the balance sheet has been collated below: The total value of Nike, Inc.’s quick assets is $17,939,000 as of May 31, 2021. This figure is calculated by adding cash and equivalents, short-term investments, and accounts receivable. Quick assets = $9,889,000 + $3,587,000 + $4,463,000 = $17,939,000 Once the total value of a company’s quick assets has been determined, the quick ratio can then be calculated. There are two different formulas. The first one uses only cash and equivalents, short-term investments, and accounts receivable in the numerator. While the second formula subtracts inventories and prepaid expenses from current assets. Regardless of whichever formula is used the result is the same. The quick ratio of Nike, Inc. is as follows: Quick Ratio = ($9,889,000 + $3,587,000 + $4,463,000) / $9,674,000 = 1.85 or Quick Ratio = ($26,291,000 – $6,854,000 - $1,498,000) / $9,674,000 = 1.85 The 1.85 quick ratio of Nike, Inc. reveals that the company has more than enough quick assets to cover its current liabilities. This means that they do not need to liquidate any non-current assets and that they might have excess cash left after meeting their obligations. Identifying and monitoring quick assets can contribute to a company’s growth. This is primarily because quick assets are used in the computation of the quick ratio. The quick ratio is an important liquidity metric, which measures the ability of a company to utilize its most liquid assets to pay off their current liabilities. It is a more conservative measure than the current ratio since it excludes inventory and prepaid expenses, which can take longer to convert into cash. A low quick ratio may signal financial distress and inability to meet short-term obligations. This may result in creditors demanding early repayment, setting higher interest rates, or reducing credit lines. Quick assets are also used to evaluate the working capital needs of a company. Quick assets are part of current assets, which are subtracted from current liabilities to calculate working capital. Working capital is used to finance a company's day-to-day operations and a lack of it can lead to solvency issues. Both quick assets and current assets are important for a company's short-term liquidity. However, there are some notable differences between the two. Below is a summary of these differences: Quick assets are important for a company's short-term liquidity and solvency. Cash and cash equivalents, marketable securities, and accounts receivable are all components of a company’s quick assets. Quick assets are used in computing for the quick ratio, which measures a company's ability to settle its short-term obligations using its most liquid and “quickly” convertible assets. Quick assets are also used to evaluate the working capital needs of a company and to finance its day to day operations. Quick assets are more liquid than current assets since they do not include inventory and prepaid expenses. Despite their differences, both quick assets and current assets are important metrics that investors and creditors evaluate before they decide to have dealings with a company or business. Thus, it is important for companies to identify and monitor both their quick and current assets. What Are Quick Assets?

Types or Components of Quick Assets

Cash and Equivalents

Accounts Receivable

Marketable Securities

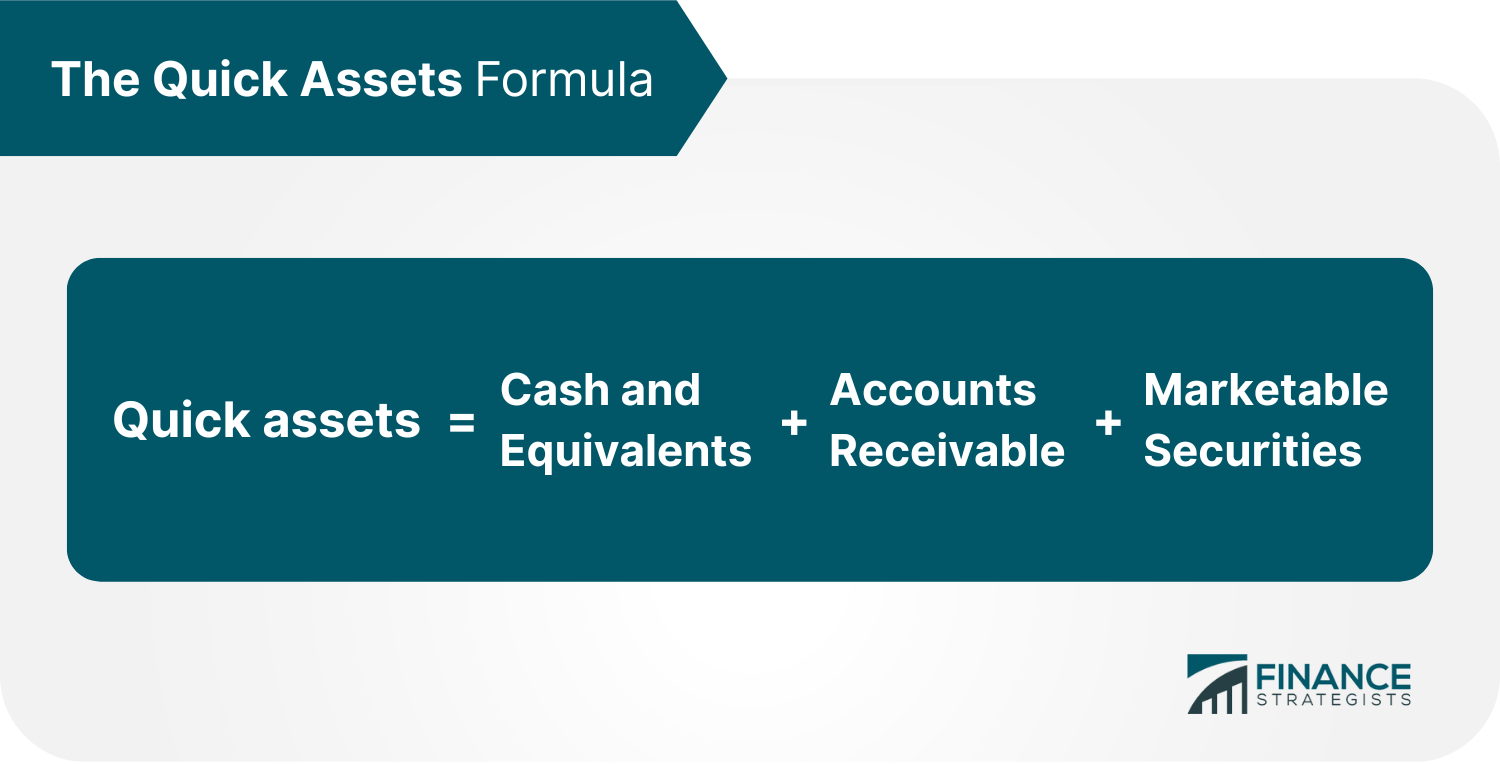

Quick Assets Formula

Real-Life Example of Quick Assets

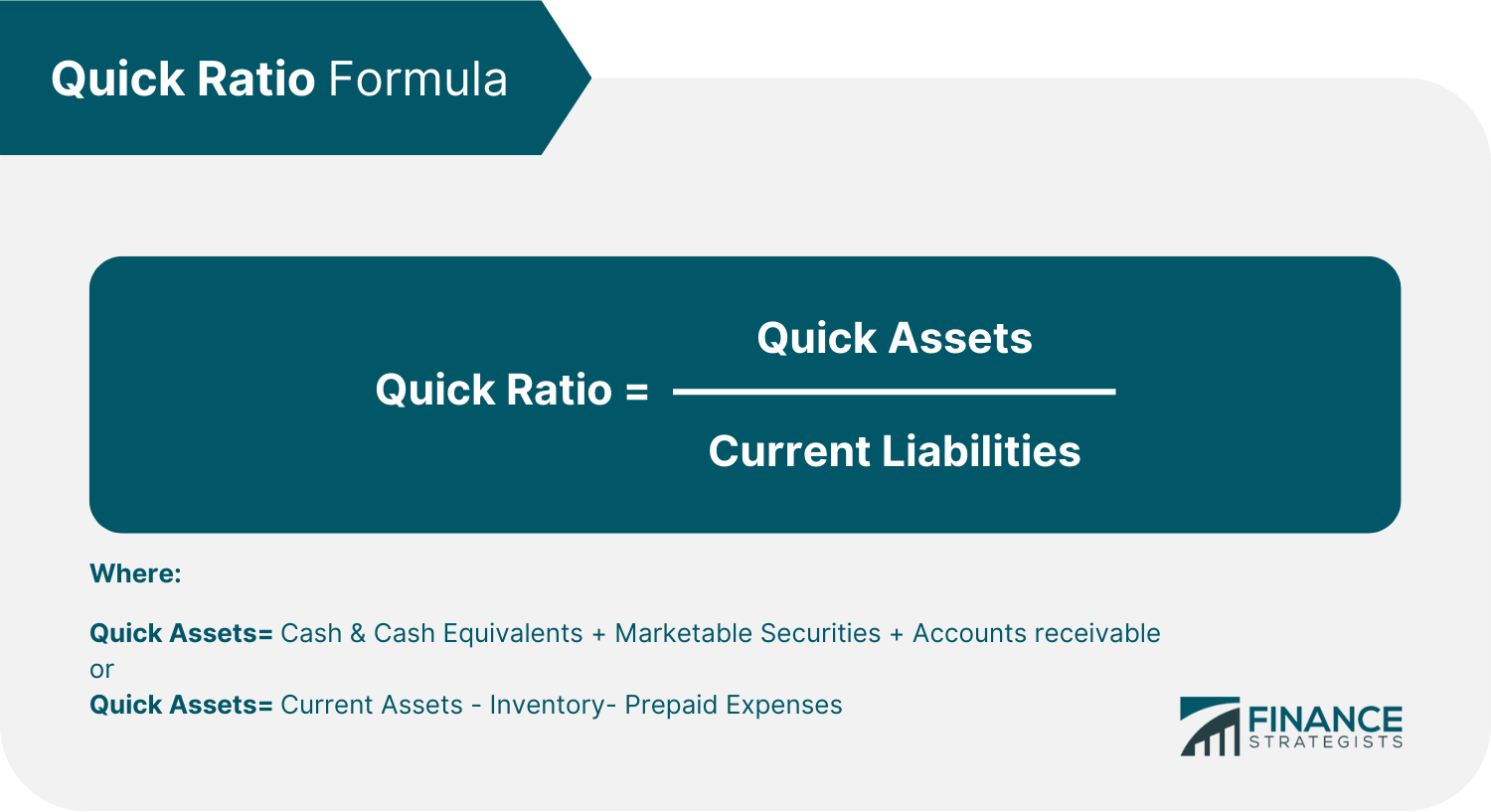

Quick Ratio

Calculating Quick Assets and Quick Ratio

Importance of Quick Assets

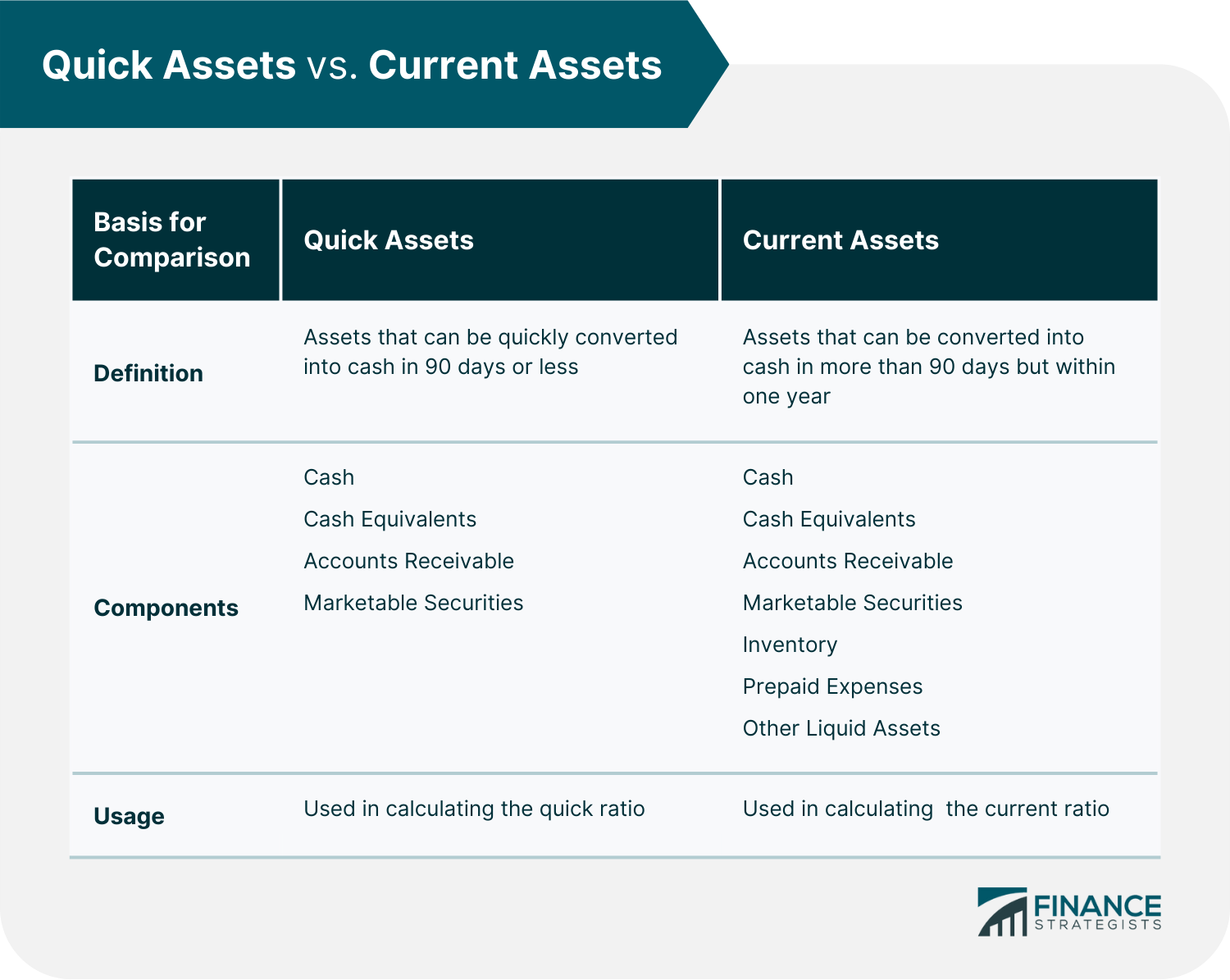

Quick Assets vs. Current Assets

The Bottom Line

Quick Assets FAQs

The types of quick assets are cash and equivalents, accounts receivable, and marketable securities.

Quick assets are calculated by adding together cash and equivalents, accounts receivable, and marketable securities. It can also be calculated by subtracting inventory and prepaid expenses from the total current assets.

Quick assets are more liquid than current assets as they do not include inventory and prepaid expenses. Quick assets are those assets that can be easily converted into cash within 90 days or less. Current assets are those assets that can be converted into cash in more than 90 days but within one year.

Quick assets are used to calculate the quick ratio, which is a key metric used to assess a company's ability to pay its short-term obligations. The quick ratio is calculated by dividing quick assets by current liabilities.

Inventories are excluded from quick assets because they are less liquid and take longer to be converted into cash.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.