An equity-indexed annuity (EIA) allows investors to earn returns based on the performance of a specified stock market index, such as the S&P 500, NASDAQ, or Dow Jones Industrial Average. EIAs are also referred to as fixed-indexed annuities, because they combine features of both fixed and variable annuities. The underlying investment of an EIA is typically a fixed-income security, such as a bond, with a return that is tied to the performance of an equity index. EIAs are designed to provide investors with a way to participate in potential stock market gains, while also providing downside protection. This is achieved through a combination of a guaranteed minimum return, typically 1-3%, and the potential for higher returns based on the performance of the underlying index. EIAs offer a level of security to investors who are concerned about market volatility or the potential for losses in traditional equity investments. EIAs can also be used as a retirement savings vehicle, providing investors with a steady income stream in retirement. EIAs are often compared to other investment options, such as traditional fixed annuities, variable annuities, and mutual funds. Traditional fixed annuities offer a fixed rate of return that is typically lower than the potential returns offered by EIAs. Variable annuities offer the potential for higher returns than traditional fixed annuities but also come with higher fees and greater market risk. Mutual funds are another investment option that offers the potential for higher returns but also come with greater market risk and no downside protection. The structure of an EIA can be broken down into three key components: premium payments, accumulation period, and annuity payout phase. Premium payments are the initial amount of money that an investor pays to purchase an EIA. The premium payments are used to fund the underlying fixed-income security that provides the guaranteed minimum return. The accumulation period is the period of time during which the investor's premium payments accumulate and earn interest. The accumulation period typically lasts 5-10 years, followed by the annuity payout phase. The annuity payout phase is the period of time during which the investor begins receiving payments from the EIA. The payments can be structured as a lump sum payment or a series of payments over a set period of time. The amount of the payments is determined by the EIA crediting method and the terms of any riders or options selected by the investor. EIAs offer investors various index options, including popular indices like the S&P 500, NASDAQ, and Dow Jones Industrial Average. The index participation rate is the percentage of the index's return that is credited to the investor's account. For example, if the index participation rate is 80%, and the underlying index returns 10%, the investor would receive a credited return of 8%. The index cap rate is the maximum amount of return that can be credited to the investor's account, regardless of the actual performance of the underlying index. For example, if the index cap rate is 7%, and the underlying index returns 10%, the investor would only receive a credited return of 7%. EIAs offer several different crediting methods to determine how the investor's account is credited with interest during the accumulation period. The most common crediting methods include point-to-point, monthly sum, monthly average, and high-water mark methods. The point-to-point method credits the investor's account based on the performance of the underlying index from the beginning of the accumulation period to the end of the period. The credited return is calculated by subtracting the beginning index value from the ending index value and then multiplying the difference by the index participation rate. The monthly sum method credits the investor's account based on the sum of the monthly index returns during the accumulation period. The credited return is calculated by adding the monthly index returns and then multiplying the sum by the index participation rate. The monthly average method credits the investor's account based on the average of the monthly index returns during the accumulation period. The credited return is calculated by adding the monthly index returns and then dividing the sum by the number of months in the accumulation period. The resulting average is then multiplied by the index participation rate. The high-water mark method credits the investor's account based on the highest index value achieved during the accumulation period. The credited return is calculated by subtracting the beginning index value from the highest index value and then multiplying the difference by the index participation rate. EIAs offer a variety of riders and options that can be added to the contract to provide additional benefits or protection to the investor. Some of the most common riders and options include guaranteed minimum withdrawal benefit (GMWB), guaranteed lifetime withdrawal benefit (GLWB), death benefit options, income riders, and long-term care riders. A GMWB rider guarantees that the investor will receive a minimum level of income from the EIA during the annuity payout phase, regardless of the actual performance of the underlying index. The rider typically includes a set percentage of the premium payments that can be withdrawn annually, and the payments continue for a set period of time. A GLWB rider provides the investor with a guaranteed stream of income for life, regardless of the actual performance of the underlying index. The rider typically includes a set percentage of the premium payments that can be withdrawn annually, and the payments continue for the life of the investor. EIAs offer different death benefit options allowing investors to pass on their EIA investment to their heirs. The most common death benefit options include the return of premium, return of premium plus interest, and stepped-up death benefit. An income rider provides the investor with a guaranteed stream of income during the annuity payout phase, regardless of the actual performance of the underlying index. The rider typically includes a set percentage of the premium payments that can be withdrawn annually, and the payments continue for a set period of time. A long-term care rider provides the investor coverage for long-term care expenses, such as nursing home care or home health care. The rider typically provides a daily benefit amount that can be used to cover the cost of long-term care, and the benefits continue for a set period of time. While EIAs offer a level of security to investors, they also come with several risks and considerations that should be carefully considered before investing. EIAs typically come with surrender charges, which are fees that are charged if the investor withdraws money from the contract before the end of the accumulation period. The surrender charges can be substantial and can last for several years, so investors should carefully consider their liquidity needs before investing in an EIA. EIAs are still subject to market risk, despite their downside protection. If the underlying index performs poorly, the investor may not receive any credited return during the accumulation period, and the annuity payout phase may result in lower payments than expected. EIAs are typically backed by the financial strength of the insurance company that issues the contract. If the insurance company were to become insolvent or unable to meet its obligations, the investor's investment might be at risk. EIAs are not liquid investments, and investors may face significant fees or surrender charges if they need to withdraw money from the contract before the end of the accumulation period. Investors should consider their liquidity needs and financial goals carefully before investing in an EIA. EIAs are tax-deferred investments, which means that the investor does not pay taxes on the earnings until they are withdrawn from the contract. However, withdrawals before age 59 ½ may be subject to a 10% penalty, and investors should consult with a tax professional to understand the tax implications of investing in an EIA. Selecting the right EIA requires careful consideration of personal financial goals, evaluation of EIA providers, comparison of EIA products, and working with a financial advisor. Investors should assess their personal financial goals, risk tolerance, and liquidity needs before investing in an EIA. EIAs may be suitable for investors who are looking for a level of security and downside protection but may not be suitable for investors who are seeking higher returns or have a need for liquidity. Investors should evaluate EIA providers based on their financial strength, reputation, and track record. It is important to select a financially stable provider with a history of successfully managing annuity contracts. Investors should compare EIA products based on the key components of the contract, including premium payments, accumulation period, annuity payout phase, index options, crediting methods, and riders and options. It is important to select an EIA that meets personal financial goals and provides the necessary level of downside protection and potential for growth. Investors should work with a financial advisor who is knowledgeable about EIAs and can provide guidance on selecting the right product, evaluating providers, and assessing personal financial goals. EIAs are regulated by several different entities, including the National Association of Insurance Commissioners (NAIC), state insurance departments, the Financial Industry Regulatory Authority (FINRA), and consumer protection and transparency requirements. The NAIC is a regulatory organization that develops model laws and regulations for insurance products, including EIAs. The NAIC works to protect consumers by ensuring that insurance products are safe, reliable, and affordable. State insurance departments regulate insurance products at the state level, including EIAs. State insurance departments are responsible for enforcing state-specific insurance laws and regulations and ensuring that insurance companies are financially sound and able to meet their obligations. FINRA is a regulatory organization that oversees the securities industry, including EIAs. FINRA protects investors by ensuring that securities products are sold fairly and transparently and that financial professionals adhere to high ethical and professional standards. EIAs are subject to consumer protection and transparency requirements, including disclosure requirements related to fees, surrender charges, and other costs associated with the contract. Investors should carefully review the disclosure documents provided by the EIA provider and consult with a financial advisor to ensure they fully understand the costs and risks associated with investing in an EIA. Equity-indexed annuities (EIAs) are a type of annuity contract that offers investors the opportunity to participate in potential stock market gains while providing downside protection. EIAs are complex investment products that require careful consideration of personal financial goals, risk tolerance, and liquidity needs. Investors should work with a financial advisor to select the right EIA and ensure that it meets their needs. While EIAs offer a level of security to investors, they also come with several risks and considerations that should be carefully considered before investing. As with any investment, investors should approach EIAs as part of a diversified portfolio and carefully consider the costs and risks associated with the contract. It is important to work with a financial advisor or insurance broker who is knowledgeable about EIAs to assess personal financial goals, evaluate providers, and compare products. What Is Equity-Indexed Annuity (EIA)?

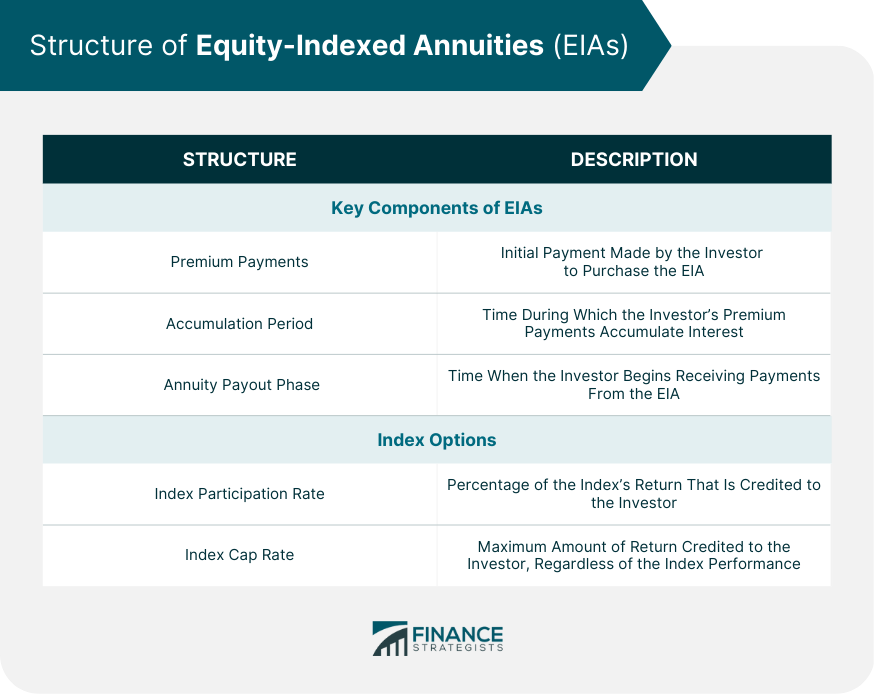

Structure of Equity-Indexed Annuities

Key Components of EIAs

Premium Payments

Accumulation Period

Annuity Payout Phase

Index Options

Index Participation Rate

Index Cap Rate

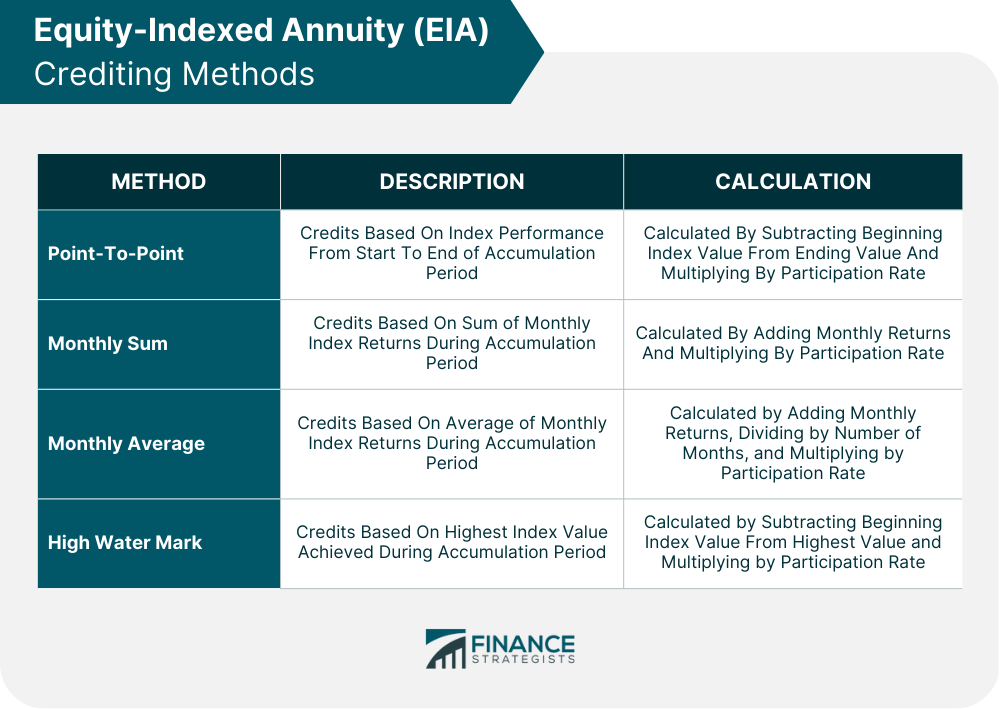

Equity-Indexed Annuity (EIA) Crediting Methods

Point-To-Point Method

Monthly Sum Method

Monthly Average Method

High Water Mark Method

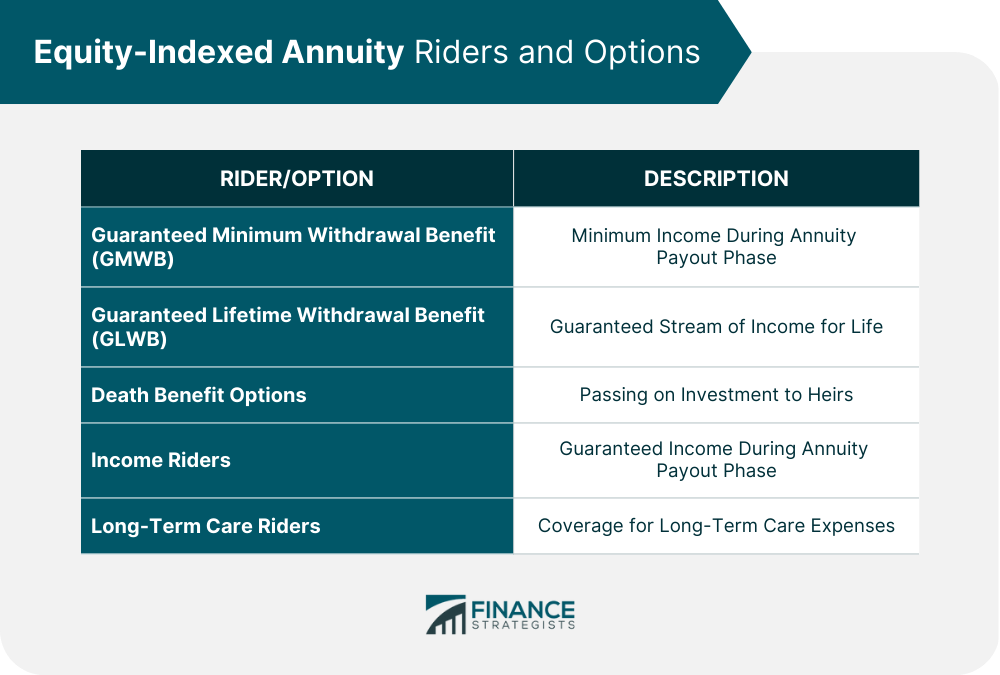

EIA Riders and Options

Guaranteed Minimum Withdrawal Benefit (GMWB)

Guaranteed Lifetime Withdrawal Benefit (GLWB)

Death Benefit Options

Income Riders

Long-Term Care Riders

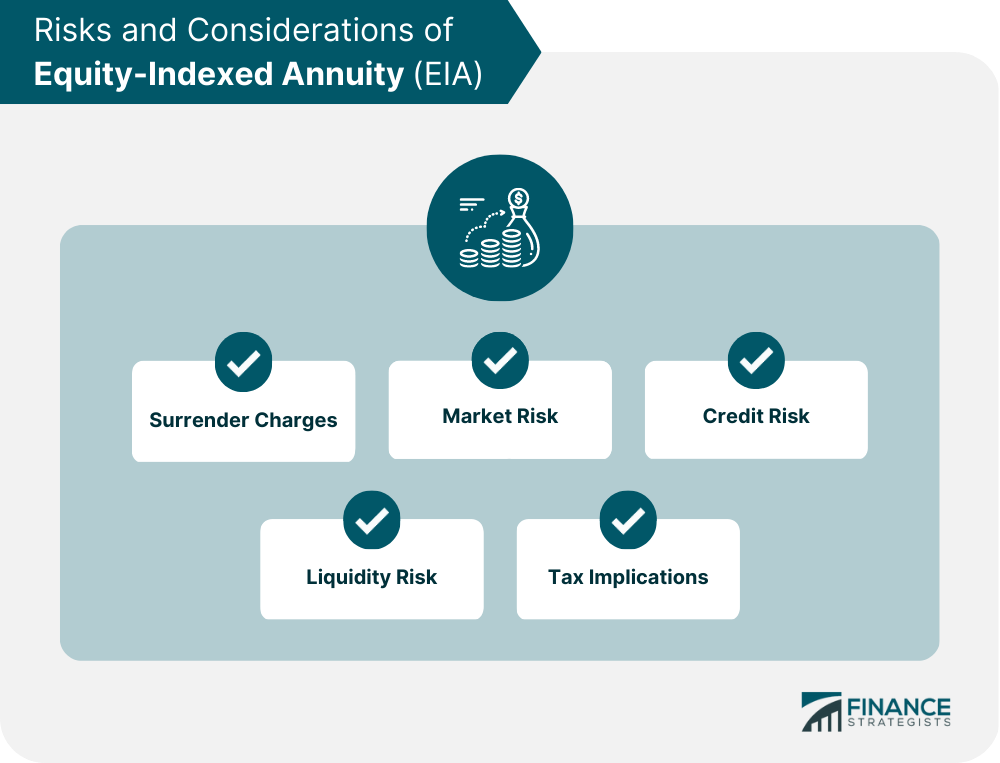

Risks and Considerations of Equity-Indexed Annuity (EIA)

Surrender Charges

Market Risk

Credit Risk

Liquidity Risk

Tax Implications

Selecting the Right Equity-Indexed Annuity (EIA)

Assessing Personal Financial Goals

Evaluating EIA Providers

Comparing EIA Products

Working With a Financial Advisor

Regulation of Equity-Indexed Annuities (EIA)

National Association of Insurance Commissioners (NAIC)

State Insurance Departments

Financial Industry Regulatory Authority (FINRA)

Consumer Protection and Transparency Requirements

Final Thoughts

Equity-Indexed Annuity (EIA) FAQs

Equity-indexed annuities (EIAs) are a type of annuity contract that allows investors to earn returns based on the performance of a specified stock market index while providing downside protection.

The key components of EIAs include premium payments, accumulation period, annuity payout phase, index options, index participation rate, index cap rate, and EIA crediting methods.

Some risks associated with EIAs include surrender charges, market risk, credit risk, liquidity risk, and tax implications. It is important to consider personal financial goals and liquidity needs carefully before investing in an EIA.

Investors should assess personal financial goals, evaluate EIA providers, compare EIA products, and work with a financial advisor who is knowledgeable about EIAs to select the right product that meets their needs.

EIAs are regulated by several entities, including the National Association of Insurance Commissioners (NAIC), state insurance departments, the Financial Industry Regulatory Authority (FINRA), and consumer protection and transparency requirements.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.