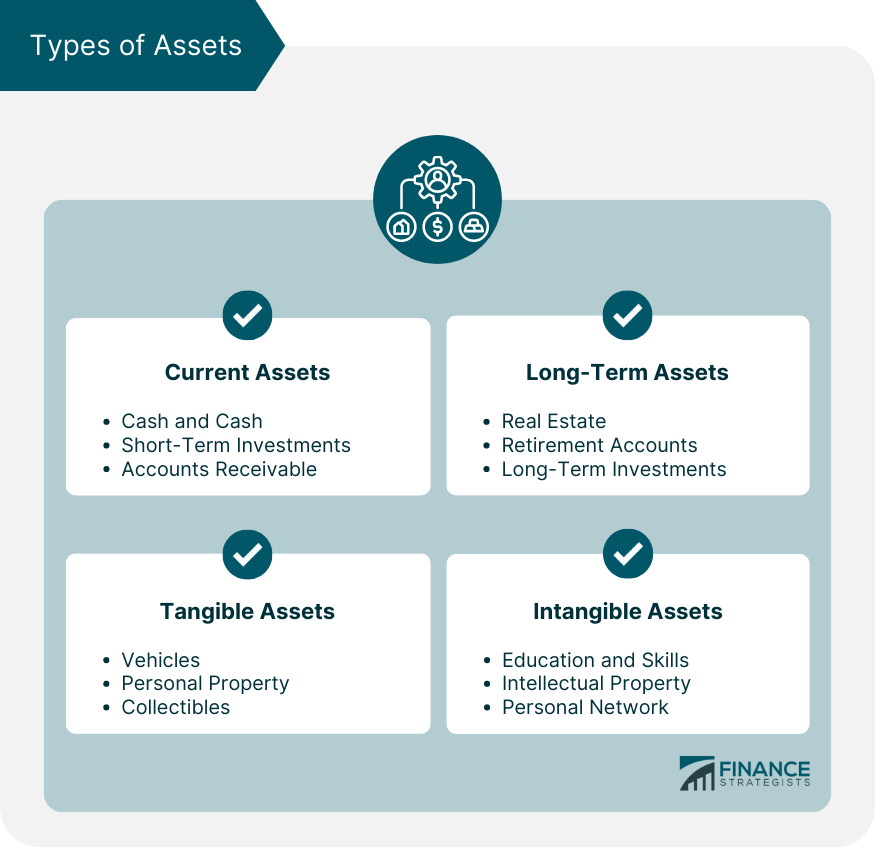

A personal balance sheet is a financial document that provides a snapshot of an individual's financial position at a specific point in time. It lists all of an individual's assets and liabilities, with the difference between the two representing their net worth. The purpose of a personal balance sheet is to help individuals assess their financial health and make informed decisions regarding their finances. It is important because it provides a clear overview of one's financial situation, helping to identify areas for improvement and opportunities for growth. The key components of a personal balance sheet are assets, liabilities, and net worth. These elements work together to provide a comprehensive understanding of an individual's financial position and are essential for effective financial planning and management. Assets are everything an individual owns that has monetary value. There are various types of assets, which can be broadly categorized into current assets, long-term assets, tangible assets, and intangible assets. Cash and cash equivalents include currency, checking and savings account balances, and other highly liquid assets that can be easily converted into cash. These assets provide immediate access to funds and are crucial for covering short-term expenses. Short-term investments are financial instruments that typically mature within one year. Examples include certificates of deposit, money market funds, and treasury bills. These investments are considered relatively low-risk and can provide a source of income or capital growth. Accounts receivable represent money owed to an individual by others, such as outstanding invoices or loans given to friends and family. These assets are expected to be collected within a short period and can contribute to an individual's overall financial resources. Real estate refers to land, residential properties, and commercial properties owned by an individual. Real estate can be a significant source of wealth, providing long-term appreciation, rental income, and potential tax benefits. Retirement accounts, such as 401(k)s, IRAs, and pension plans, are long-term assets designed to provide financial security during retirement. These accounts often benefit from tax advantages and can grow over time through compound interest and investment returns. Long-term investments are financial instruments held for more than one year, such as stocks, bonds, and mutual funds. These investments can generate income and capital gains over time, contributing to an individual's overall wealth. Vehicles, including cars, motorcycles, boats, and recreational vehicles, are tangible assets that can be used for transportation or leisure. While vehicles typically depreciate over time, they can still contribute to an individual's net worth. Personal property encompasses items such as furniture, electronics, and appliances that have a monetary value. These assets can be sold or used as collateral for loans and contribute to an individual's financial resources. Collectibles include items like art, antiques, stamps, and coins that have value due to their rarity, age, or cultural significance. These assets can appreciate in value over time and contribute to an individual's overall wealth. Education and skills are intangible assets that represent an individual's knowledge, abilities, and expertise. These assets can lead to increased earning potential, job security, and career advancement opportunities. Intellectual property includes assets such as patents, trademarks, copyrights, and trade secrets that have a monetary value. These assets can generate income through licensing agreements, royalties, or sales and contribute to an individual's net worth. A personal network consists of an individual's relationships with friends, family, colleagues, and other professional connections. This intangible asset can provide valuable support, advice, and opportunities, ultimately impacting an individual's financial success and overall well-being. Liabilities are financial obligations or debts that an individual owes to others. They can be broadly categorized into current and long-term liabilities, impacting an individual's net worth and financial stability. Credit card debt is a form of unsecured debt that results from using credit cards to make purchases or cover expenses. High-interest rates can make credit card debt challenging to manage, and paying it down is essential for improving one's financial health. Short-term loans are debts that must be repaid within a relatively short period, typically within a year. Examples include payday loans and personal loans. Managing these debts is important to avoid costly fees and maintain a healthy credit score. Accounts payable represent amounts owed to others for goods or services, such as utility bills, medical expenses, or taxes. Timely payment of these liabilities is crucial for maintaining good credit and avoiding late fees or penalties. Mortgage loans are secured debts used to finance the purchase of real estate. While these loans can help individuals build equity and provide potential tax benefits, managing the monthly payments is vital for maintaining financial stability. Student loans are debts incurred to finance education and can be either government-backed or private. These loans often have relatively low-interest rates but can be a significant financial burden, making it essential to develop a repayment strategy. Car loans are secured debts used to finance the purchase of vehicles. Managing these loans is essential for maintaining ownership of the vehicle, building equity, and improving one's overall financial position. Net worth is the difference between an individual's total assets and total liabilities. It serves as a key indicator of a person's financial health, providing insight into their overall financial stability and progress toward financial goals. To calculate net worth, first, add up the total value of all assets, including cash, investments, real estate, and personal property. Next, add up the total amount of all liabilities, such as credit card debt, loans, and mortgages. Finally, subtract the total liabilities from the total assets to determine net worth. Several factors can influence an individual's net worth, including income, spending habits, investment performance, and life events such as marriage, divorce, or inheritance. By understanding these factors, individuals can make informed decisions to improve their financial situation and increase their net worth. Tracking net worth over time is important for monitoring financial progress, identifying trends, and assessing the effectiveness of financial strategies. Regularly updating and reviewing one's net worth can help individuals stay accountable to their financial goals and make necessary adjustments to stay on track. Saving and investing are crucial strategies for increasing assets and building wealth. By consistently setting aside a portion of income and investing in various financial instruments, individuals can benefit from compound interest and potential capital gains. Diversifying investments involves spreading funds across different asset classes, industries, and geographic regions. This strategy helps to reduce risk and maximize potential returns, ultimately contributing to a stronger personal balance sheet. Enhancing human capital involves investing in education, skills, and personal development. By improving one's knowledge and abilities, individuals can increase their earning potential, job security, and career advancement opportunities, all of which can positively impact their net worth. Effective debt management strategies include consolidating debts, negotiating lower interest rates, and creating a debt repayment plan. These approaches can help individuals reduce their liabilities, save on interest payments, and improve their overall financial health. Refinancing involves replacing existing loans with new loans that have more favorable terms, such as lower interest rates or extended repayment periods. Refinancing can help individuals reduce their monthly payments, save on interest costs, and pay off debts more quickly. Creating and following a budget can help individuals control their spending and identify areas for cost reduction. Individuals can decrease their liabilities and improve their personal balance sheet by minimizing expenses and prioritizing debt repayment. Personal finance software can help individuals track their assets and liabilities, manage their budgets, and monitor their net worth. These tools can simplify financial management and provide valuable insights for improving one's financial situation. Spreadsheets and templates are customizable tools that can be used to create and maintain a personal balance sheet. These resources allow individuals to organize their financial data, perform calculations, and analyze their financial position. Financial advisors and planners are professionals who can provide personalized advice and guidance on managing assets, reducing liabilities, and improving one's personal balance sheet. These experts can help individuals develop and implement effective financial strategies. Online resources and communities offer valuable information, tools, and support for managing personal finances. Websites, blogs, forums, and social media groups can provide tips, advice, and encouragement for individuals seeking to improve their personal balance sheet. Personal balance sheets play a critical role in financial planning by providing a clear and comprehensive view of an individual's financial position. Understanding one's assets and liabilities allows for better decision-making, goal-setting, and overall financial management. Maintaining a healthy personal balance sheet offers numerous benefits, including increased financial security, reduced stress, and greater opportunities for wealth accumulation. A strong balance sheet can also contribute to better credit scores and improved borrowing power. Achieving and maintaining a healthy personal balance sheet requires a commitment to ongoing financial growth and stability. This involves regularly reviewing and adjusting financial strategies, as well as adapting to changes in personal circumstances and market conditions. Seeking the guidance of a financial advisor can be an invaluable step toward improving one's personal balance sheet. These professionals can offer tailored advice and support to help individuals navigate their financial journey and achieve their long-term goals.What Is a Personal Balance Sheet?

Assets

Current Assets

Cash and Cash Equivalents

Short-term Investments

Accounts Receivable

Long-term Assets

Real Estate

Retirement Accounts

Long-term Investments

Tangible Assets

Vehicles

Personal Property

Collectibles

Intangible Assets

Education and Skills

Intellectual Property

Personal Network

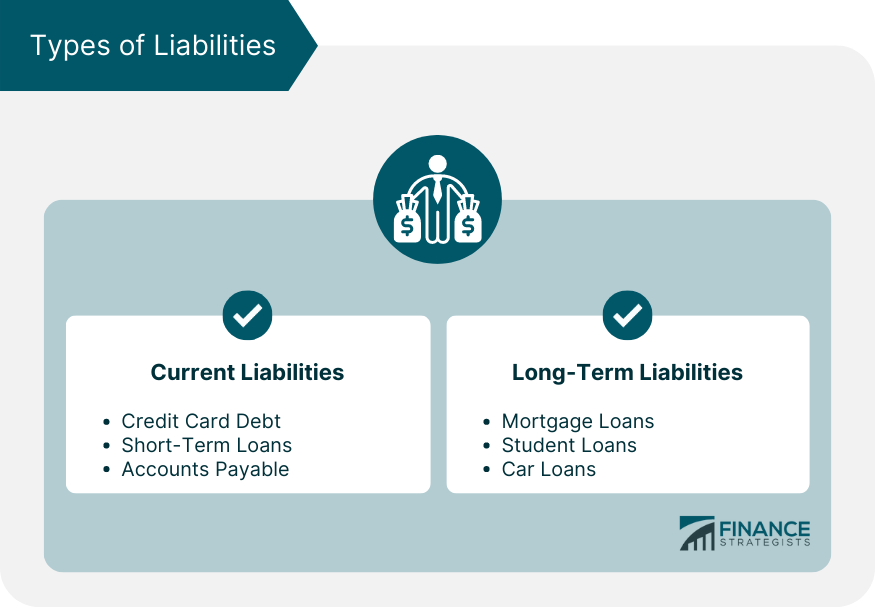

Liabilities

Current Liabilities

Credit Card Debt

Short-term Loans

Accounts Payable

Long-term Liabilities

Mortgage Loans

Student Loans

Car Loans

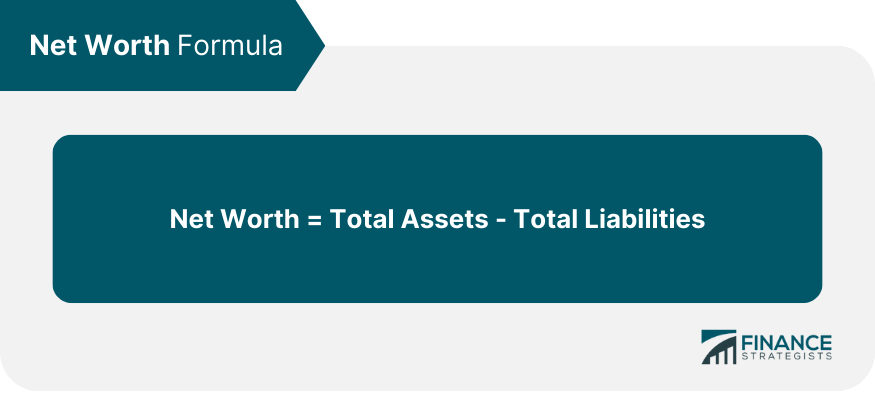

Net Worth

How to Calculate Net Worth

Factors Influencing Net Worth

Importance of Tracking Net Worth Over Time

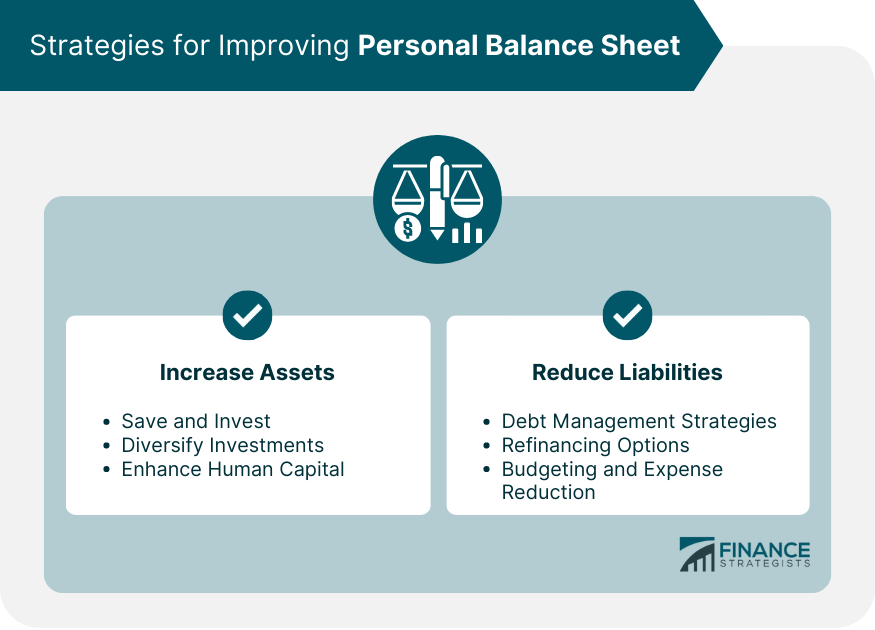

Strategies for Improving Personal Balance Sheet

Increasing Assets

Saving and Investing

Diversifying Investments

Enhancing Human Capital

Reducing Liabilities

Debt Management Strategies

Refinancing Options

Budgeting and Expense Reduction

Tools and Resources for Personal Balance Sheet Management

Personal Finance Software

Spreadsheets and Templates

Financial Advisors and Planners

Online Resources and Communities

Final Thoughts

Personal Balance Sheet FAQs

A personal balance sheet is a financial document that provides a snapshot of your financial position at a specific point in time by listing your assets and liabilities. It is important because it helps you assess your financial health, identify areas for improvement, and make informed decisions regarding your finances.

You can improve your personal balance sheet by increasing your assets through saving, investing, diversifying investments, and enhancing human capital. Additionally, focus on reducing your liabilities by implementing debt management strategies, exploring refinancing options, and practicing budgeting and expense reduction.

There are various tools and resources available for managing your personal balance sheet, including personal finance software, spreadsheets and templates, financial advisors and planners, and online resources and communities. These tools can help simplify financial management and provide valuable insights for improving your financial situation.

It's recommended to update and review your personal balance sheet at least once a year or whenever there's a significant change in your financial situation. Regularly tracking your assets, liabilities, and net worth can help you stay accountable to your financial goals and make necessary adjustments to stay on track.

A financial advisor can provide personalized advice and guidance on managing your assets, reducing your liabilities, and improving your personal balance sheet. They can help you develop and implement effective financial strategies tailored to your unique financial situation and long-term goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.