A blockchain is a decentralized and distributed digital ledger that records transactions across multiple computers so that any involved record cannot be altered retroactively without the alteration of all subsequent blocks. This transparent and secure structure makes blockchain an appealing backbone for a variety of applications. Creating a blockchain involves defining the structure of the blocks, where each block usually contains data (for example, transactions), the hash of the block (a unique identifier), and the hash of the previous block. The process also includes implementing a method for adding new blocks and for validating the integrity of the blockchain. The purpose of creating a blockchain may vary. It could be for creating a new cryptocurrency, like Bitcoin or Ethereum. Other applications include decentralized finance (DeFi), supply chain monitoring, voting systems, and secure sharing of medical records, to name a few. By creating a blockchain, one aims to establish a transparent, immutable, and decentralized network that enhances trust and security. The first step in creating a blockchain is to determine its purpose. Ask questions such as, what problem is the blockchain meant to solve? Or how will it improve existing processes? Your answers will guide your blockchain's design and functionality. Consensus mechanisms are protocols that ensure all nodes in a blockchain network agree on the information added to the blockchain. Popular consensus mechanisms include Proof-of-Work (PoW), Proof-of-Stake (PoS), and Delegated Proof-of-Stake (DPoS). The choice depends on the network's needs for security, speed, and energy efficiency. This phase involves outlining the structural design of your blockchain, such as whether it will be a single chain of blocks or multiple chains, and deciding on the transaction processing model (like UTXO or account/balance model). Parameters such as block size, block time, reward per block, and network difficulty adjustments need to be defined. These parameters impact the performance and security of your blockchain. A block in the blockchain contains a list of transactions, a timestamp, and a reference to the previous block. It also contains a unique identifier called a hash. During this step, the format of the block and its ability to store the necessary data is established. A blockchain is valid only if the blocks are linked correctly and the transactions within each block are valid. Implementing checks to ensure chain validity includes designing proof-of-work or proof-of-stake systems, cryptographic hashing, and digital signatures. The genesis block, or the first block in the blockchain, is hardcoded into the software. It sets a precedent for the rest of the chain, and its creation signals the launch of your blockchain. A crucial decision in creating a blockchain is whether it will be public, where anyone can participate, or private, with restricted participation. This decision impacts the blockchain's transparency, security, speed, and potential applications. Compliance with regulations is a key consideration in any technology implementation, especially with blockchain. Since blockchain often deals with sensitive data, ensuring compliance with data protection laws is vital. The ability to handle an increasing number of transactions is a major consideration in blockchain design. Performance enhancements like sharding, off-chain transactions, and second-layer solutions can help overcome scalability issues. Security is paramount in the blockchain. Measures like cryptographic hashing, digital signatures, and consensus mechanisms help maintain data integrity and protect against fraudulent activities. Blockchain's inherent structure makes it nearly impossible to alter data once it's been added. This gives it a high level of data integrity. The decentralized and immutable nature of blockchain makes it highly transparent. Every participant can verify the transactions on the blockchain, promoting trust among users. Thanks to its unique design, blockchain is highly secure against hacking and fraud. Transactions need to be agreed upon by consensus before being added to the blockchain, and once they are added, they cannot be altered or deleted. Blockchain operates on a peer-to-peer network, reducing the need for central authorities or intermediaries. This promotes efficient transactions and empowers individual participants. Creating a blockchain requires advanced technical knowledge in areas like cryptography, distributed systems, and consensus mechanisms. This can make it a challenging endeavor. Due to the technical expertise required, the cost of developing a blockchain can be significant. Moreover, continuous maintenance and upgrades add to these costs. Blockchain technology often faces regulatory scrutiny and uncertainty. Navigating these legal complexities can pose a challenge to blockchain development. As mentioned earlier, scalability can be a significant hurdle for blockchains. As the network grows, maintaining speed and efficiency can become more difficult. Creating a blockchain involves several key steps, including defining its purpose, selecting a consensus mechanism, structuring the blockchain, setting parameters, and establishing blocks and chain validity. A crucial decision is whether to create a public or private blockchain, with considerations around regulatory compliance, scalability, performance, and security. The decentralized, transparent, and secure nature of blockchain offers potential benefits, including enhanced data integrity, increased transparency, improved security, and decentralization. Despite these benefits, challenges include technical complexity, high development costs, regulatory uncertainty, and scalability issues. The creation process requires a careful balance of these factors, aiming to leverage the unique strengths of blockchain technology while overcoming potential obstacles. This holistic approach to creating a blockchain can unlock its potential to transform industries and processes in a secure, decentralized, and efficient manner.Blockchain Overview

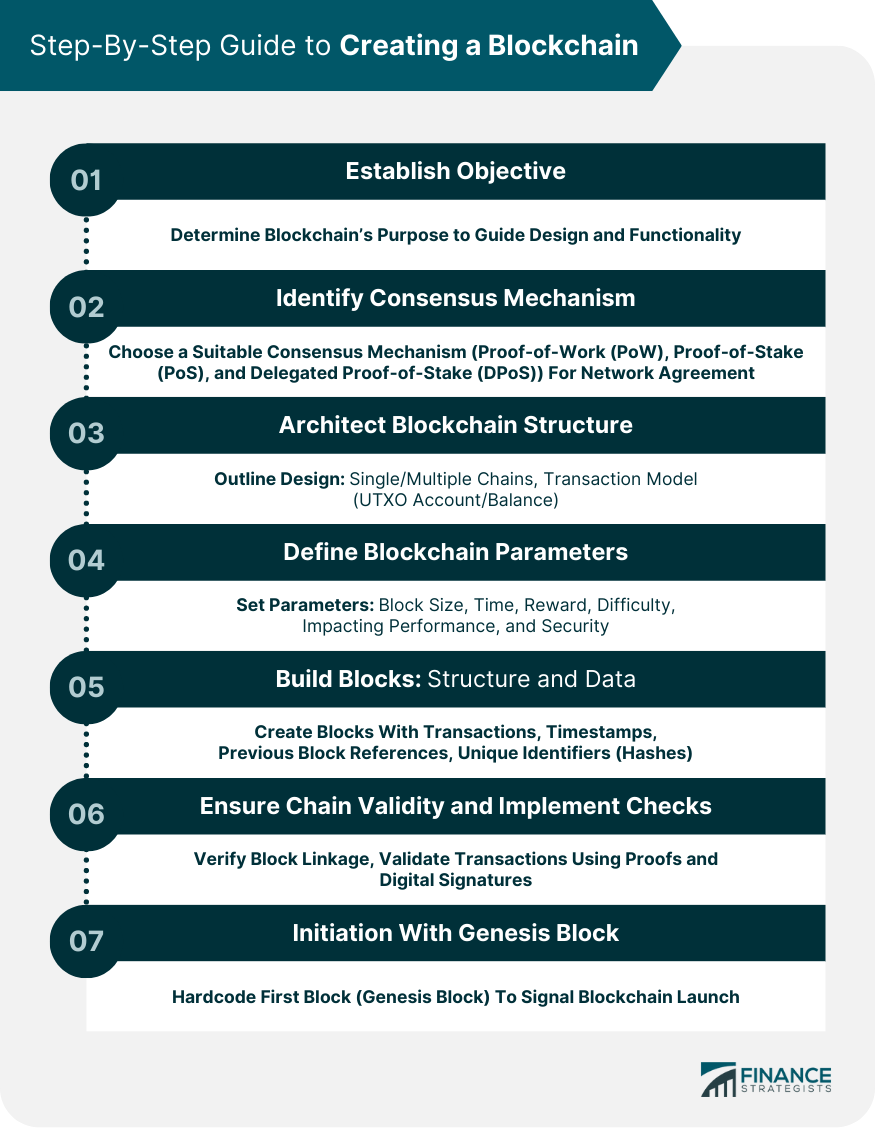

Step-By-Step Guide to Creating a Blockchain

Establish the Blockchain's Objective

Identify a Suitable Consensus Mechanism

Architect the Blockchain Structure

Define Blockchain Parameters

Build the Blocks: Structure and Data

Ensure Chain Validity and Implement Checks

Initiation With the Genesis Block

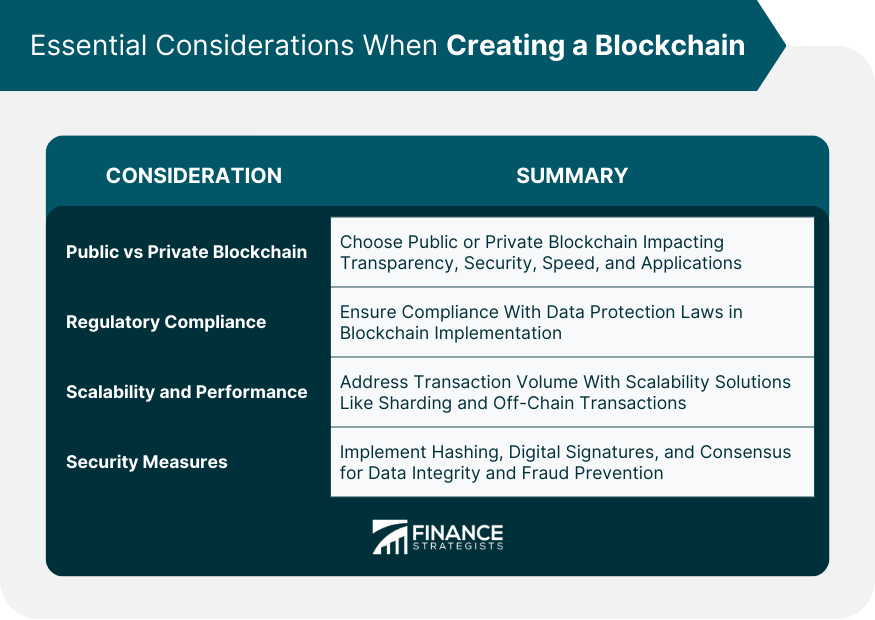

Essential Considerations When Creating a Blockchain

Public vs Private Blockchain

Regulatory Compliance

Scalability and Performance

Security Measures

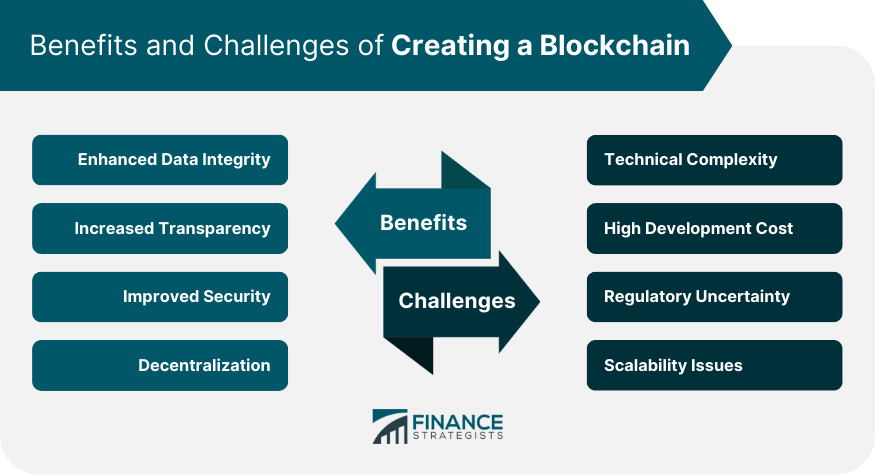

Benefits of Creating a Blockchain

Enhanced Data Integrity

Increased Transparency

Improved Security

Decentralization

Challenges in Creating a Blockchain

Technical Complexity

High Development Cost

Regulatory Uncertainty

Scalability Issues

Final Thoughts

How to Create a Blockchain FAQs

A consensus mechanism is a protocol used in blockchain networks to achieve agreement on the data added to the blockchain. It's important because it ensures that all nodes in the network agree on the validity of transactions, thereby maintaining the integrity and security of the blockchain.

A public blockchain is open to anyone who wants to participate, while a private blockchain restricts participation to invited members only. The choice between public and private can impact the blockchain's transparency, speed, security, and potential applications.

Challenges in creating a blockchain include technical complexity requiring expertise in areas like cryptography and distributed systems, high development costs, regulatory uncertainty due to the emerging nature of blockchain technology, and scalability issues as the network grows.

Blockchain provides enhanced data integrity, increased transparency, improved security, and decentralization. It allows for the verification of transactions and reduces the need for intermediaries, promoting efficient transactions and building trust among participants.

The genesis block, also known as the first block in the blockchain, is hardcoded into the blockchain software. It sets the precedent for the rest of the chain, and its creation marks the launch of a new blockchain.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.