Return on assets (ROA) ratio is a metric used to evaluate how efficiently a company is able to generate profit with the assets it has available. It measures the percentage of how much income a company's net operating profit, after taxes, has earned annually on average over three years from all the business operations and investments. ROA shows what happened with a firm's historically acquired resources. It gives an idea as to how efficient the management is at using its assets to generate earnings. Expressed as a percentage, a higher ROA indicates a more efficient use of company resources. ROA is an indicator of performance that incorporates the company's asset base. ROA provides information about how efficiently a company uses its assets to generate earnings. It is calculated by dividing a company's net profit for a period by the value of the company's total assets as follows: Since ROA is expressed in percentage, the result of dividing the net profit by the average total assets should be multiplied by 100. ROA is most useful when comparing two companies within the same industry. This is because the assets that are required to do business in different industries can be vastly different from one another, making it hard to appropriately compare, say, an airline and a law firm. For example, say an investor wanted to compare two competing ice cream stores. Company A has $5 million in net income and $20 million in assets. Company B has $2 million in net income and $5 million in assets. At first glance, Company A might seem like the better investment since it has a higher net income. However, Company A's ROA is only 25%, whereas Company B has a ROA of 40%. This shows that Company B is able to use its assets more effectively to generate profit, and so is likely the better investment. ROA is very useful in differentiating between competing companies and can be used to compare similar companies within the same industry. Both ROA and ROE are good measures of performance since both measures how a company utilizes its assets. ROA looks at the use of assets to generate earnings. The ROA ratio gives a better picture of how efficiently a company is utilizing its assets since it accounts for a company's debt. If the ROA is increasing over time, it means that the company has been using its assets more efficiently to produce income. ROE focuses on common equity only. It does not account for the company's debt, leaving out the liabilities. If ROE is increasing over time it means that the company has been using a smaller percentage of its assets to produce income. ROA shows how efficiently a company is using its assets, while the debt-to-equity ratio provides more information on how well a company can pay off its liabilities. Higher ROA ratios indicate that more profit has been generated from the assets. Lower ROA ratios indicate that less profit has been generated from the assets. This can mean that management is not as efficient at utilizing its assets to generate income, or that it is taking on more liabilities than necessary to produce income. Both ROA and profit margin can be used to show how efficient a company is in terms of its assets and expenses. ROA focuses on total net income while profit margin concentrates on net income after taxes. There are two popular limitations of Return of Assets Ratio. If ROA is calculated for companies in different industries, it will not be very meaningful since ROAs vary widely among industries and groups of companies within the same industry. ROA shows how well a company is currently utilizing its assets but does not take into consideration the conditions under which the assets are being used. Another limitation is that ROA is not very useful in explaining why ROA increased or decreased. This is because ROA is calculated based on historical data, not future projections. The disadvantages of ROA include the following: Since ROA shows how efficiently a company is utilizing its assets to generate earnings, ROA can be used for comparison purposes of the same industry. ROA can also be used to predict future earnings. ROA is important, but ROA does have its limitations, such as not including the use of debt. ROA should be used in conjunction with other financial ratios, such as ROE and profit margin, for a better indication of performance efficiency.Define ROA Ratio in Simple Terms

Importance of Return on Assets Ratio

Calculating ROA

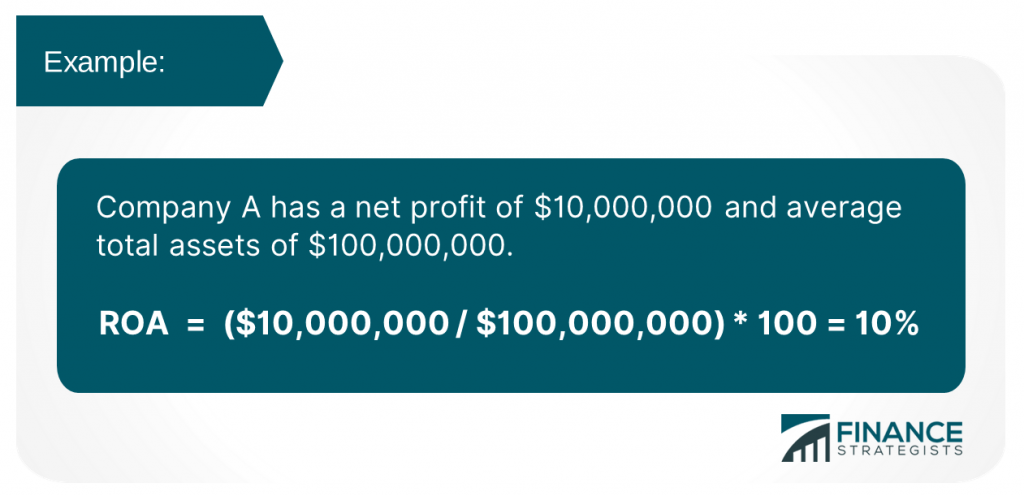

ROA Example

What Are the Benefits of Using ROA as a Measure of Performance?

Return on Assets (ROA) vs Return on Equity (ROE)

ROA

ROE

The Importance of Calculating ROA With Other Ratios, Such as Debt-To-Equity and Profit Margin

ROA vs Debt-to-Equity

ROA vs Profit Margin Ratio

Limitations of ROA Ratio

Affected by Type of Industry

Does Not Factor in How Long a Company Has Been Generating Earnings

Does Not Explain Its Increase or Decrease

What Are the Disadvantages of ROA as a Measure for Performance?

The Bottom Line

Return on Assets (ROA) Ratio FAQs

ROA stands for Return on Assets.

Return on assets, or ROA, is a metric used to evaluate how efficiently a company is able to generate profit with the assets it has available.

Return on Assets is calculated by divided a company's net income by its total assets.

ROA is most useful when comparing two companies within the same industry. This is because the assets that are required to do business in different industries can be vastly different from one another, making it hard to appropriately compare, say, an airline and a law firm.

Expressed as a percentage, a higher ROA indicates a more efficient use of company resources.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.