Tax diversification in retirement is a financial planning strategy that involves spreading retirement savings and investments across accounts that are subject to different tax rules. The idea is to create a diversified portfolio of assets that receive different tax treatments, with the aim of optimizing tax efficiency and providing greater flexibility in managing income and taxes during retirement. This strategy can help retirees minimize their overall tax liability and maximize their after-tax income. Tax brackets are the divisions within a tax system that determine the applicable tax rate based on an individual's income level. Understanding tax brackets is essential for tax-efficient retirement planning. Tax-deferred accounts, such as traditional IRAs and 401(k)s, allow investors to contribute pre-tax dollars, which grow tax-free until withdrawals are made in retirement. These accounts are a key component of tax diversification strategies. Tax-exempt accounts, such as Roth IRAs and Roth 401(k)s, are funded with after-tax dollars, and qualified withdrawals are tax-free. Incorporating these accounts into retirement planning can improve tax diversification. Taxable accounts, such as brokerage accounts and savings accounts, are funded with after-tax dollars, and their earnings are subject to taxation. Proper management of these accounts is crucial for tax-efficient retirement planning. A Roth IRA conversion involves transferring funds from a traditional IRA to a Roth IRA, with taxes due on the converted amount. Conversions can help retirees achieve better tax diversification by creating tax-free income sources in retirement. By strategically withdrawing from both tax-deferred and taxable accounts, retirees can balance their tax burden while maintaining a steady income stream. This approach helps optimize tax efficiency during retirement. Municipal bonds provide interest income that is typically exempt from federal income tax and, in some cases, state and local taxes. Including municipal bonds in a retirement portfolio can enhance tax diversification and generate tax-free income. Gifting strategies involve transferring assets to family members or donating to charity to help reduce taxable income and lower the overall tax burden. Implementing these strategies can optimize tax diversification in retirement planning. An individual's current tax bracket influences the tax diversification strategies they should employ, as different income levels may require unique approaches to minimize tax liabilities and maximize income during retirement. Estimating future tax rates is crucial for effective tax diversification in retirement planning, as changes in tax laws and rates can significantly impact the tax efficiency of a retirement income strategy. The length of an investor's time horizon – the time between their initial investment and when they plan to retire – affects the choice of tax diversification strategies, as longer time horizons offer more opportunities for tax-efficient growth. Legacy and estate planning goals can impact tax diversification strategies, as retirees may need to balance tax efficiency with their desire to leave assets to heirs or support charitable causes. Tax diversification provides retirees with a range of options for accessing their retirement savings. By having a mix of taxable, tax-deferred, and tax-free accounts, retirees can strategically choose which accounts to withdraw from based on their financial needs and tax situation in any given year. This flexibility allows retirees to respond to changes in their personal circumstances, market conditions, and tax laws. By strategically managing withdrawals from different types of accounts, retirees can potentially minimize their overall tax liability. For example, in a year when a retiree's taxable income is relatively low, they might choose to withdraw from a tax-deferred account (such as a traditional IRA) to take advantage of lower tax rates. In a year when taxable income is higher, they might choose to withdraw from a tax-free account (such as a Roth IRA) to avoid increasing their tax burden. Tax diversification gives retirees greater control over their income streams in retirement. For example, if a retiree needs additional income for a large expense, they can choose to withdraw from a taxable account and pay capital gains tax (which may be lower than ordinary income tax rates). This can be a better option than taking a larger distribution from a tax-deferred account and paying higher income taxes. Additionally, retirees can manage their income to stay within certain tax brackets or avoid triggering taxes on Social Security benefits. Tax diversification can lead to long-term tax savings by allowing retirees to manage their tax exposure over the course of their retirement. By carefully planning withdrawals from different accounts, retirees can spread out their tax liability over time, potentially resulting in lower overall taxes paid. This can be especially beneficial if tax rates increase in the future, as retirees can shift more of their withdrawals to tax-free accounts to avoid higher taxes. Focusing too heavily on tax-deferred accounts can lead to a substantial tax burden in retirement, as required minimum distributions and other withdrawals may push retirees into higher tax brackets. Disregarding the possibility of future tax rate changes can result in suboptimal tax diversification strategies, as retirees may not be prepared for the impact of tax law revisions on their retirement income. Failing to account for required minimum distributions (RMDs) from tax-deferred accounts can lead to increased tax liabilities in retirement, as RMDs can push retirees into higher tax brackets and affect their overall tax diversification. Tax diversification in retirement is a strategy that allocates retirement assets across various accounts with distinct tax treatments. The goal is to enhance tax efficiency, increase flexibility in managing retirement income and taxes, and reduce overall tax liability to boost after-tax income. A comprehensive approach to retirement planning that considers tax diversification alongside other financial goals is essential for maximizing wealth preservation and ensuring a comfortable retirement. Tax diversification plays a vital role in achieving financial goals by optimizing tax efficiency, reducing tax liabilities, and providing flexibility in managing retirement income streams. Consulting with a financial professional can help retirees develop and implement tax diversification strategies tailored to their unique financial circumstances and goals.What Is Tax Diversification in Retirement?

Key Concepts in Tax Diversification

Tax Brackets

Tax-Deferred Accounts

Tax-Exempt Accounts

Taxable Accounts

Strategies for Tax Diversification in Retirement

Roth IRA Conversions

Strategic Withdrawals from Tax-Deferred and Taxable Accounts

Utilizing Municipal Bonds for Tax-Exempt Income

Gifting Strategies to Reduce Tax Burden

Factors Affecting Tax Diversification in Retirement

Individual's Current Tax Bracket

Anticipated Tax Rates During Retirement

Investment Time Horizon

Legacy and Estate Planning Considerations

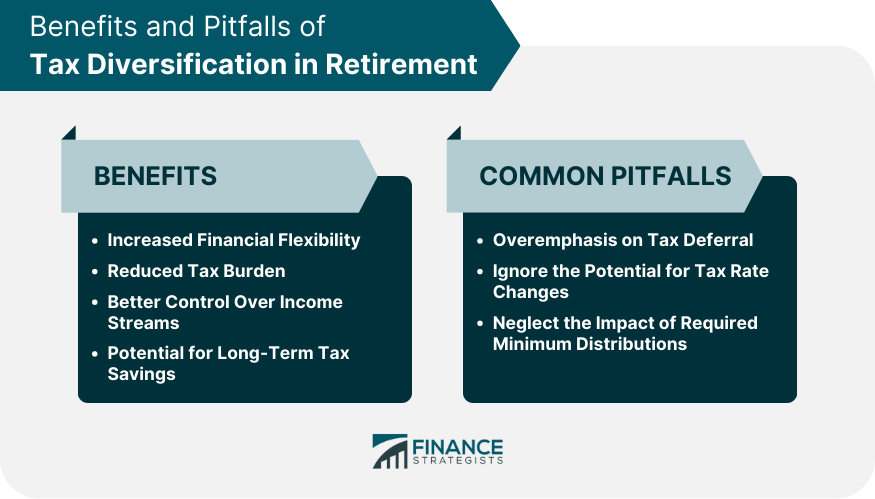

Benefits of Tax Diversification in Retirement

Increased Financial Flexibility

Reduced Tax Burden

Better Control Over Income Streams

Potential for Long-Term Tax Savings

Common Pitfalls and Misconceptions on Tax Diversification in Retirement

Overemphasis on Tax Deferral

Ignoring the Potential for Tax Rate Changes

Neglecting the Impact of Required Minimum Distributions

Final Thoughts

Tax Diversification in Retirement FAQs

Tax diversification in retirement refers to strategically allocating assets and income streams across various tax categories to optimize tax efficiency during retirement. It is important because it helps retirees preserve wealth, minimize tax liabilities, and maintain a more predictable income stream.

Tax-deferred accounts, such as traditional IRAs and 401(k)s, and tax-exempt accounts, like Roth IRAs and Roth 401(k)s, provide different tax treatment for contributions and withdrawals. Using both types of accounts can help retirees create a balanced and tax-efficient income stream during retirement, optimizing tax diversification.

Strategies to improve tax diversification in retirement include Roth IRA conversions, strategic withdrawals from tax-deferred and taxable accounts, utilizing municipal bonds for tax-exempt income, and implementing gifting strategies to reduce the overall tax burden.

Factors to consider when creating a tax diversification plan for retirement include the individual's current tax bracket, anticipated tax rates during retirement, investment time horizon, and legacy and estate planning considerations.

Yes, seeking professional advice can help retirees develop and implement customized tax diversification strategies that consider their unique financial circumstances and goals, leading to a more tax-efficient retirement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.