Reducing debt before retirement is essential for financial stability during your golden years. By paying off debt before retirement, you minimize financial obligations and maximize your retirement income, allowing for a more comfortable and enjoyable retirement. Entering retirement with minimal debt reduces financial stress and provides greater flexibility in budgeting. It allows for increased savings, investment opportunities, and a higher standard of living, all while reducing reliance on social security or pension income. Understanding the various types of debt is crucial for effective debt reduction. Common forms of debt include mortgages, credit card debt, student loans, personal loans, and auto loans. Each type of debt has different interest rates and repayment terms, which must be considered in your debt reduction strategy. Mortgage debt is a long-term loan taken out to purchase a home. Mortgages typically have lower interest rates compared to other forms of debt, but can span over 15 to 30 years. Reducing this debt can increase home equity and lower monthly expenses in retirement. Credit card debt is a high-interest, revolving type of debt that can quickly accumulate if not managed properly. Reducing credit card debt is a priority in pre-retirement planning, as it can significantly impact your overall financial health. Student loan debt is a common form of debt for higher education expenses. Federal student loans often have lower interest rates and more flexible repayment options than private loans. Paying off student loans before retirement can reduce monthly financial obligations. Personal loans are unsecured loans used for various purposes such as debt consolidation, home improvement, or emergency expenses. They typically have fixed interest rates and repayment terms. Reducing personal loan debt is essential to minimize financial obligations during retirement. Auto loans are secured loans used to purchase vehicles. Interest rates and terms vary based on credit score and loan duration. Paying off auto loans before retirement can help reduce monthly expenses and improve cash flow. To effectively reduce debt, start by making a comprehensive list of all your outstanding debts. Include details such as interest rates, outstanding balances, and minimum monthly payments to gain a clear understanding of your debt situation. After listing all your debts, calculate the total outstanding balance. This figure provides a benchmark for measuring progress in debt reduction and helps prioritize which debts to pay off first. Knowing the interest rates and minimum payments of each debt is essential for creating an effective debt reduction plan. High-interest debts should be prioritized, as they cost more over time and can hinder your ability to save for retirement. Calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income. A high ratio indicates a greater financial burden, and reducing this ratio is crucial for achieving financial stability in retirement. The avalanche method involves paying off debts with the highest interest rates first while making minimum payments on other debts. This strategy saves money on interest payments and helps eliminate high-interest debt more quickly. Focusing on the high-interest debt first can save significant amounts of money in the long run. Reducing these debts minimizes overall interest payments, allowing for greater contributions to retirement savings and quicker debt repayment. Debt consolidation loans combine multiple high-interest debts into a single loan with a lower interest rate. This simplifies debt management and can lower monthly payments, making it easier to pay off debt and save for retirement. Balance transfer credit cards offer low or zero interest rates for a promotional period, allowing you to transfer high-interest credit card debt and save on interest payments. This can expedite debt repayment and reduce the overall cost of paying off credit card debt. Mortgage refinancing involves replacing your existing mortgage with a new loan, typically at a lower interest rate or with better terms. This can lower monthly payments, freeing up funds to pay off other high-interest debts or increase retirement savings. Taking on a side hustle or part-time work can provide additional income to help pay off debt more quickly. This extra income stream can be dedicated entirely to debt reduction, accelerating your progress toward a debt-free retirement. Reducing discretionary spendings, such as dining out, entertainment, and vacations, can free up funds for debt repayment. By prioritizing essential expenses and minimizing non-essential spending, you can allocate more money toward debt reduction and retirement savings. Selling unused or unnecessary assets, such as a second car or unneeded household items, can generate additional funds for debt repayment. This not only helps reduce debt but also declutters your life and simplifies your financial situation. Using windfalls, such as tax refunds or work bonuses, to pay off debt can help accelerate debt reduction. By allocating these unexpected funds towards debt repayment, you can make significant progress in achieving a debt-free retirement. Inheritance or other unexpected income sources can be used to pay off debt more quickly. Utilizing these funds strategically can help you reach your pre-retirement debt reduction goals and increase your financial stability in retirement. A key element in successful pre-retirement debt reduction is creating and maintaining a realistic budget. Begin by tracking all sources of income and expenses to gain a clear understanding of your financial situation and identify areas where adjustments can be made. Allocate a portion of your income towards debt reduction in your budget. Ensure that this allocation is both aggressive and realistic, striking a balance between paying off debt quickly and maintaining a manageable lifestyle. Regularly review and adjust your budget as your financial situation changes. This allows you to stay on track with your debt reduction goals and ensure that your budget continues to align with your changing needs and priorities. An emergency fund provides a financial cushion for unexpected expenses, such as medical bills or home repairs. Having an emergency fund helps prevent the need to rely on high-interest debt, protecting your progress towards pre-retirement debt reduction. It is recommended to save at least 3 to 6 months' worth of living expenses in your emergency fund. This amount provides a sufficient buffer to cover unforeseen expenses without compromising your debt reduction or retirement savings goals. Maximizing contributions to employer-sponsored retirement plans, such as 401(k)s or 403(b)s, is essential for building retirement savings. These plans often include employer matching contributions, which can significantly boost your retirement savings and reduce your reliance on debt. Contributing to an individual retirement account (IRA), such as a traditional or Roth IRA, can provide additional retirement savings opportunities. These accounts offer tax advantages and investment options that can help grow your retirement savings and reduce your reliance on debt in retirement. Consistently review and update your debt reduction plan to ensure that it remains effective and in line with your financial goals. This allows you to make adjustments as needed and stay on track toward achieving pre-retirement debt reduction. Acknowledge and celebrate your progress as you reach debt reduction milestones. This helps maintain motivation and provides a sense of accomplishment, encouraging you to continue working towards your pre-retirement debt reduction goals. Share your debt reduction goals with friends, family, or financial advisors to create a support network. Their encouragement, advice, and accountability can be invaluable in helping you stay motivated and focused on achieving your pre-retirement debt reduction objectives. Pre-retirement debt reduction offers long-term benefits, such as increased financial stability, reduced stress, and greater flexibility in retirement. By minimizing debt before retirement, you can enjoy a higher standard of living and increased financial independence. Reducing debt before retirement is essential for achieving financial independence and peace of mind during your golden years. A debt-free retirement allows you to focus on enjoying your newfound freedom without the burden of financial obligations. Consider seeking the assistance of professional retirement planning services to help you develop and implement a comprehensive pre-retirement debt reduction strategy. These experts can provide personalized guidance and support to help you achieve your financial goals and enjoy a comfortable, debt-free retirement.What Is Pre-Retirement Debt Reduction?

Understanding Your Debts

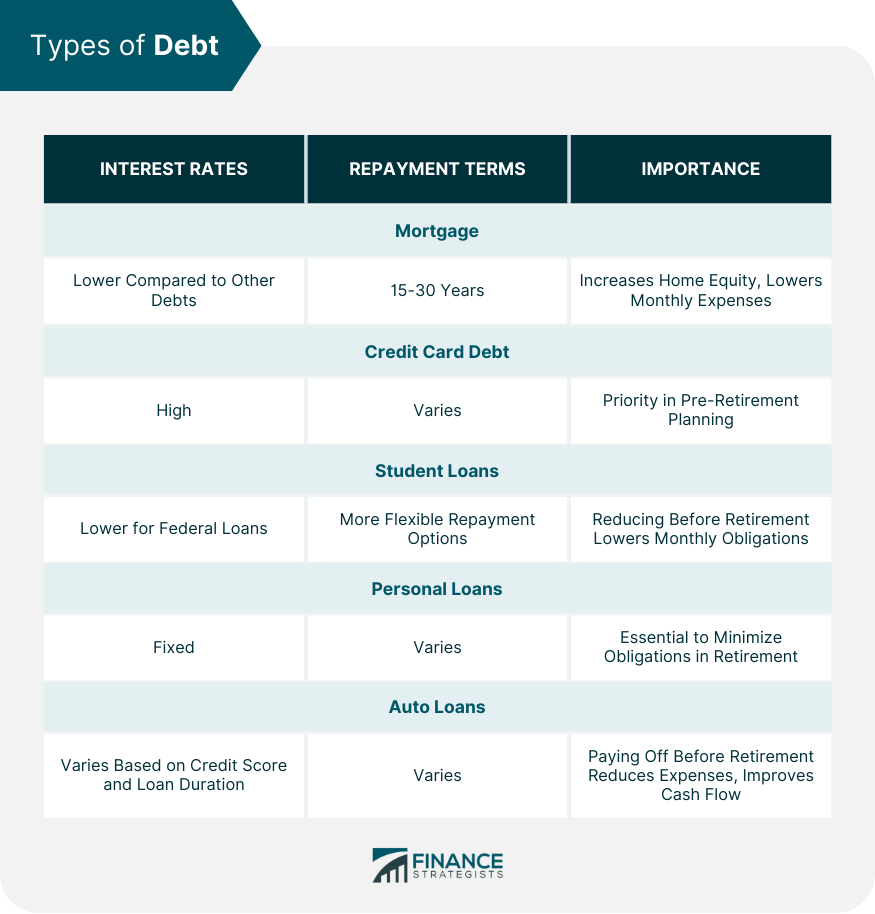

Types of Debt

Mortgage

Credit Card Debt

Student Loans

Personal Loans

Auto Loans

Analyzing Your Debt Situation

Listing All Debts

Calculating Total Debt

Identifying Interest Rates and Minimum Payments

Assessing Your Debt-to-Income Ratio

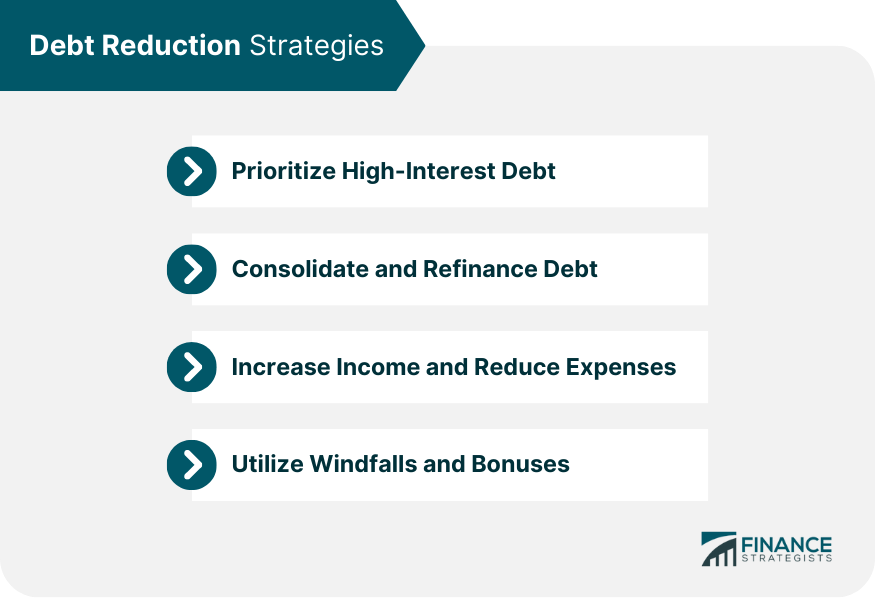

Debt Reduction Strategies

Prioritizing High-Interest Debt

Avalanche Method

Benefits of Tackling High-Interest Debt First

Consolidating and Refinancing Debt

Debt Consolidation Loans

Balance Transfer Credit Cards

Mortgage Refinancing

Increasing Income and Reducing Expenses

Side Hustles and Part-Time Work

Cutting Discretionary Spending

Selling Unused Assets

Utilizing Windfalls and Bonuses

Applying Tax Refunds and Work Bonuses Towards Debt

Inheritance and Other Unexpected Income

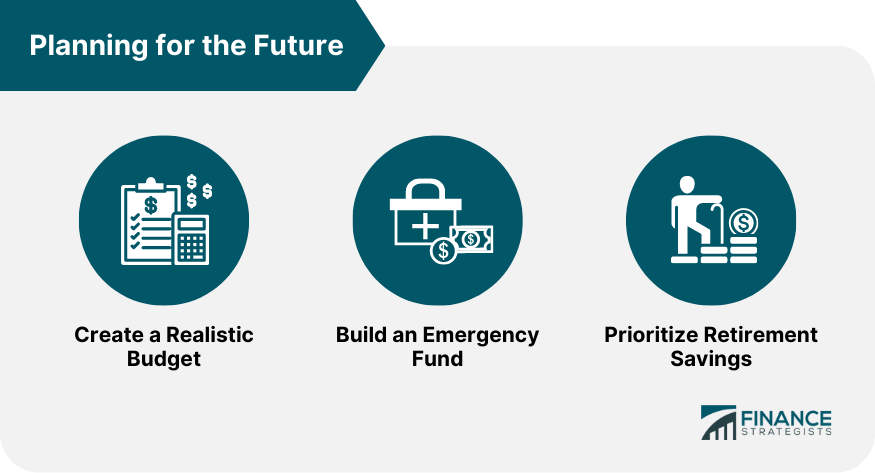

Planning for the Future

Creating a Realistic Budget

Tracking Income and Expenses

Allocating Funds Towards Debt Reduction

Adjusting Budget as Needed

Building an Emergency Fund

Importance of Having a Financial Cushion

Recommended Amount to Save

Prioritizing Retirement Savings

Taking Advantage of Employer-Sponsored Plans

Contributing to Individual Retirement Accounts (IRAs)

Monitoring Progress and Staying Motivated

Regularly Reviewing and Updating Your Debt Reduction Plan

Celebrating Milestones and Achievements

Seeking Support from Friends, Family, or Financial Advisors

Final Thoughts

Pre-Retirement Debt Reduction FAQs

Pre-retirement debt reduction is crucial because it minimizes financial obligations, maximizes retirement income, and allows for a more comfortable and enjoyable retirement. By reducing debt before retirement, you can achieve greater financial stability and independence during your golden years.

To prioritize your debts, start by listing all your outstanding balances, interest rates, and minimum payments. Focus on high-interest debt first, such as credit card debt, as it can significantly impact your overall financial health. Consider using the avalanche method, which involves paying off debts with the highest interest rates first while making minimum payments on other debts.

Effective pre-retirement debt reduction strategies include prioritizing high-interest debt, consolidating and refinancing debt, increasing income and reducing expenses, and utilizing windfalls and bonuses. Combining these strategies can help accelerate debt repayment and improve your financial situation before retirement.

To balance debt reduction and retirement savings, create a realistic budget that allocates funds towards both goals. Maximize contributions to employer-sponsored retirement plans and individual retirement accounts (IRAs) while aggressively paying off high-interest debt. Regularly review and adjust your budget to ensure it aligns with your changing financial needs and priorities.

To stay motivated and monitor your progress, regularly review and update your debt reduction plan, celebrate milestones and achievements, and seek support from friends, family, or financial advisors. Sharing your goals and progress with a support network can provide encouragement, advice, and accountability, helping you stay focused on achieving pre-retirement debt reduction.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.