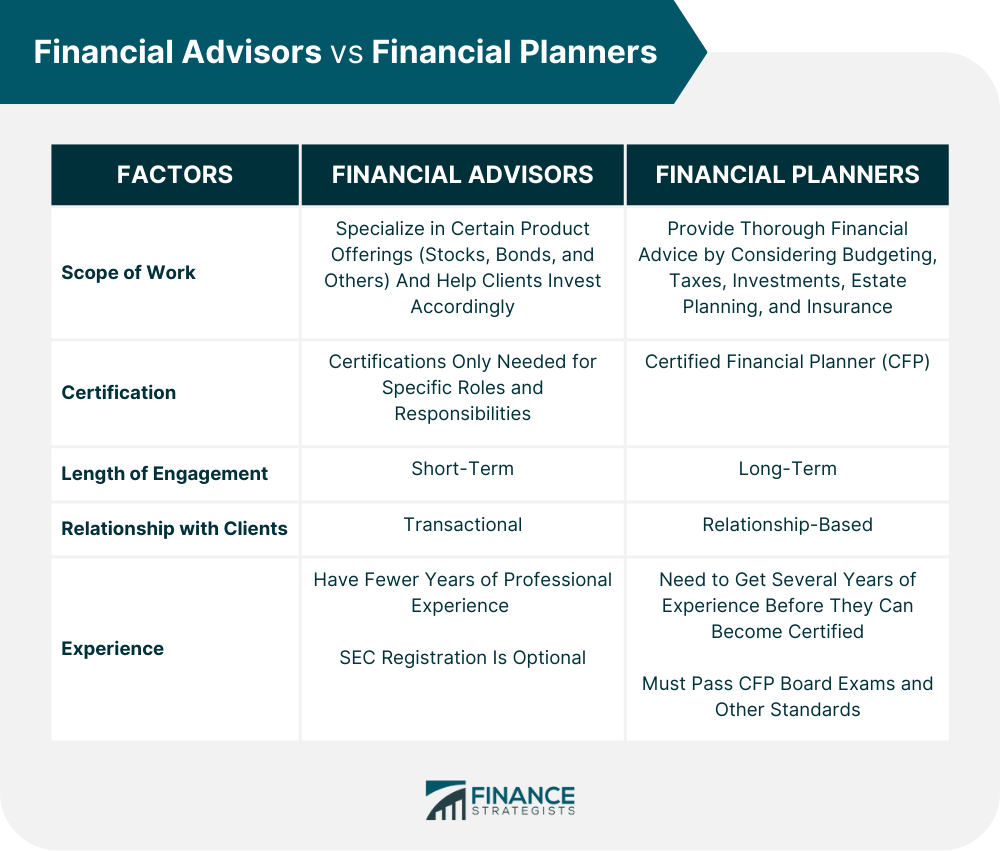

Financial advisors are professionals who help clients manage their money. Financial planners are a type of financial advisor that help clients strategize their finances to meet their long-term financial goals. A financial advisor may assist in specific and immediate financial matters like the management of investments, the sale or purchase of stocks, or the development of an estate and tax plan. The term financial advisor refers to a broader category that includes brokers, money managers, insurance agents, and bankers. A financial planner is a specialist who assists individuals and businesses in developing long-term financial strategies. They often help establish a budgeting, saving, investing, and retirement plan. In the financial services business, a fiduciary must prioritize clients' interests while making investment choices on their behalf. Financial planners have fiduciary obligations, whereas not all financial advisors are fiduciary. Have a financial question? Click here. A financial advisor is a professional who advises clients on financial matters, personal finances, and investments. They operate by providing a wide range of advice, including investment management, tax preparation, estate planning, portfolio management, and insurance products. A financial advisor typically focuses on a single issue. They do not consider the big picture. Instead, they take a restricted view of the question and only advise you on what you have asked. For example, you could wish to know how to invest a lump sum for the long term. A financial advisor will evaluate your alternatives and recommend your best investment strategy without considering if it is a wise decision in the long term. Financial advisors tend to put emphasis on financial products because they usually get paid if they promote a particular product. However, some also charge a flat fee. A financial planner will assess your financial condition involving adding up your income, estimating expenses, creating a budget, managing debt load, savings and investment inventory, and the like. Further, such assessment is compared with short- and long-term financial goals, which are both essential to financial security. They specialize in developing a comprehensive strategy to assist clients in achieving long-term objectives. In many circumstances, they will assist in managing your investments, but this is seldom the case. A financial planner may also specialize in certain areas, such as retirement planning or education planning. In addition to helping provide long-term wealth management solutions, a good financial planner will also provide ongoing assessment of a client's changing goals and life circumstances. When it comes to financial advice, clients often have difficulty distinguishing the role of a financial advisor from that of a financial planner. While both provide valuable services, significant differences should be considered when choosing the right professional. The scope of work for a financial advisor and a planner is the primary difference between them. A financial advisor may specialize in specific product offerings, such as stocks or bonds, and help clients invest accordingly. On the other hand, a financial planner provides advice by looking at all aspects of an individual’s finances, including budgeting, taxes, investments, estate planning, and insurance. A Certified Senior Advisor (CSA) is an example of a financial advisor accreditation provided by ANSI National Accreditation Board (ANAB). Other professional credentials available for financial advisors are Behavioral Financial Advisor (BFA) and Certified Retirement Professional Advisor (CRPA). Meanwhile, financial planners may need different certifications based on their expertise. The Certified Financial Planner (CFP) designation is one of the most widely recognized titles among financial professionals. The National Commission for Certifying Agencies (NCCA) provides this accreditation. Individuals who have earned this title have demonstrated a mastery of various financial planning topics and ethical practices. Other credentials available are Chartered Senior Financial Planner (CSFP), Registered Financial Planner (RFP), Master Financial Planner (MFP) and others. The comprehensive list of credentials and designations can be found in the Financial Industry Regulatory Authority (FINRA). Financial advisors typically work with clients on an ongoing basis, providing advice and assistance as needed. On the other hand, financial planners often take on a more project-based approach. They may help a client devise a retirement plan or manage a business's sale, but their role will end once those objectives have been met. The relationship between financial advisors and clients can be more transactional, as they typically provide advice on specific products. In contrast, financial planners tend to develop closer relationships with their clients since they offer broader advice on all aspects of their finances. Financial advisors may have fewer years of professional experience since the licensing requirements to become an advisor are less stringent than those for a financial planner. Financial planners may also have additional education or training in law, accounting, or tax preparation. A financial advisor can be most helpful for people who go through major life events like marriage, divorce, or the onset of a serious illness or disability. Financial advisors can cater to these specific and urgent financial matters to help clients be on track. On the other hand, financial planners are ideal for those who want to strategize on long-term financial matters. These professionals help clients see the bigger picture of their finances as a whole. For those with specific or limited financial concerns, an advisor may suffice. Still, a certified financial planner could be the better choice for those with more complex situations or multiple goals to consider. Ultimately, the primary benefit of using either professional is having expert advice to help protect investments and reach desired objectives. Choosing the right financial advisor or planner can be daunting. Here are some tips to help you make an informed decision: Determine Your Financial Needs. Consider the type of financial advice you need and the services you require to narrow your search. Check Their Background. Research any potential advisors or planners before engaging them. Check their credentials and qualifications and regulatory bodies' disciplinary actions against them. Learn About Their Fee Structures. It is important to be aware of all costs associated with working with these professionals so that you can make an informed decision. Consider a Fiduciary. Working with a fiduciary planner provides additional protection and assurance that your money will be managed responsibly. Use the Right Search Tools. Numerous online tools are available to help you find and compare qualified advisors and planners. Interview Multiple Financial Advisors and Financial Planners. Ask a financial advisor about experience, qualifications, fee structures, and any disciplinary actions. There are two important professionals who provide financial guidance, a financial advisor and a financial planner. A financial advisor generally offers investment insight and products such as stocks, bonds, and mutual funds. A financial planner provides broader services that help you create an overall plan for your long-term money goals. This can include investment management but also planning for retirement, taxes, and estate planning. Both advisors and planners may do some of the same things. Still, depending on your particular goals, you may need to consult a professional who can provide services beyond just stock portfolio guidance. Choosing the right financial advisor or planner requires careful consideration. Be sure to do your due diligence and research potential professionals, compare their credentials and fees, consider a fiduciary relationship, and interview multiple advisors or planners before making any decisions. This will ensure that you find the best professional to meet your financial needs and goals.Financial Advisor vs Financial Planner: An Overview

What Is a Financial Advisor?

What Is a Financial Planner?

Differences Between Financial Advisors & Financial Planners

Scope of Work

Certification

Length of Engagement

Relationship with Clients

Experience

When Do You Need a Financial Advisor or a Financial Planner?

Tips for Choosing a Financial Advisor and a Financial Planner

Final Thoughts

Financial Advisor vs Financial Planner FAQs

A Financial Advisor is someone who provides general advice on investments, while a Financial Planner specializes in developing comprehensive financial plans that consider all aspects of an individual's financial goals and objectives.

A Financial Advisor can help you identify your financial goals, create an action plan to reach those goals, and provide guidance on how best to manage your investments.

When selecting a Financial Advisor, it is important to research their qualifications and experience as well as how they are compensated. It is also important to ensure that the Advisor has your best interests in mind and will work with you to protect your financial security.

A Financial Planner’s main objective is to create a comprehensive plan tailored to an individual’s financial needs and objectives. This includes analyzing the individual’s current financial situation, developing a strategy to reach their goals, and monitoring progress over time.

A Financial Planner can be beneficial for anyone looking to establish a comprehensive financial plan that takes into account all aspects of their finances. It is important to research the qualifications and experience of any Financial Planner you are considering working with and make sure that their services match your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.