A Certificate of Deposit (CD) is a type of time deposit offered by banks and credit unions. When you purchase a CD, you agree to deposit a fixed sum of money for a specific time period, known as the term. The financial institution, in return, guarantees a certain interest rate throughout the term. At the end of the term, you receive your initial deposit along with the interest accrued. CDs are a valuable tool for savers who wish to earn more on their funds than a typical savings account, without taking on the risk associated with other investments. However, one significant downside to CDs is that they often come with penalties for early withdrawal, making them less flexible than other savings options. The Federal Deposit Insurance Corporation (FDIC) is an independent agency established by the U.S government to maintain stability and public confidence in the nation's financial system. The FDIC provides insurance coverage for deposits up to $250,000 per depositor, per FDIC-insured bank, per ownership category. This insurance is pivotal for consumer protection, ensuring that even in the event of a bank failure, consumers' funds up to the insured limit are not lost. FDIC insurance extends to CDs just as it does to other banking products like checking and savings accounts. If an FDIC-insured bank or credit union fails, your CD investments are protected up to the $250,000 limit. However, it's worth noting that FDIC does not insure investment products that are not deposits, such as mutual funds, stocks, or bonds. So, while the principal and interest in your CDs are safe, any losses on non-deposit investments are not covered. FDIC insured CDs can be purchased from any FDIC-insured bank or savings association. Many credit unions also offer CDs that are insured by the National Credit Union Administration (NCUA), a similar federal insurer for credit unions. Online platforms also facilitate CD purchases, providing an avenue for comparison and selection of the best rates across multiple institutions. Purchasing a CD is a straightforward process. You can open a CD account online, over the phone, or in person at a financial institution. You'll need to determine the term length for your CD and the amount you want to deposit. Remember, it's always important to read the fine print and understand any fees, penalties, or rules associated with the CD. This refers to the period during which your money will be locked in the CD. The term can range from a few months to several years. Typically, longer terms offer higher interest rates. However, it also means your money will be inaccessible for a longer period without incurring a penalty. It's important to select a term length that aligns with your financial goals and liquidity needs. This is the rate at which your money will grow while in the CD. Higher interest rates are more beneficial for the depositor, as they result in greater earnings. Comparing rates from different institutions can help you find the most competitive option. However, it's crucial to consider this factor in conjunction with the term length. CDs often come with a penalty if you withdraw your money before the end of the term. These penalties can be steep enough to eat into your principal, not just your earned interest. Therefore, before investing, you should be confident that you won't need to access the funds prematurely. It's essential to ensure that the financial institution offering the CD is insured by the Federal Deposit Insurance Corporation (FDIC). This insurance protects your deposit up to $250,000 in the event that the institution fails. The FDIC only insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category. This means if your total deposits at a single bank, including the CD, exceed this limit, the excess won't be insured. It's crucial to be mindful of this limit when purchasing a CD, especially if you already have other accounts at the same institution. FDIC insured CDs are one of the safest investments available. As long as your total deposits, including CDs, at any single FDIC-insured institution are $250,000 or less, your investment is entirely secure. This safety makes CDs an attractive option for risk-averse investors or those looking for a stable component within their broader investment portfolio. CDs come with a fixed interest rate for the term of the deposit. Even if market rates fluctuate, the interest on your CD remains consistent. This stability of returns provides predictability, allowing for precise financial planning, particularly valuable in times of economic uncertainty. The FDIC insures up to $250,000 per depositor, per insured bank, for each account ownership category. This limit is inclusive of all the depositor's accounts, including checking, savings, and CDs at an insured bank. Understanding these limits is crucial to ensure you don't exceed them, as deposits above the $250,000 limit are not covered by the FDIC. CDs are designed to be held until the term ends. If you need to withdraw your money before the term concludes, you'll likely face a penalty. These penalties can significantly reduce your earned interest and might even dip into your initial deposit. Hence, it's important to consider your liquidity needs before investing in a CD. While CDs offer stable returns, there's a risk that the rate of inflation could surpass your CD's interest rate. In such a scenario, the purchasing power of your money could decrease over time. For example, if inflation is at 3% and your CD only offers a 2% return, the real value of your investment is essentially diminishing, a factor worth considering, particularly for long-term CDs. CDs come with various term lengths, from just a few months to several years. Typically, longer terms offer higher interest rates, but they also require you to lock up your money for a more extended period. Understanding your financial needs and liquidity requirements can guide you in selecting the most appropriate term length. A straightforward way to maximize your FDIC coverage is by distributing your deposits across several FDIC-insured banks. The $250,000 coverage applies per depositor, per bank, so having accounts in different banks effectively expands your coverage. This method allows you to safeguard a more significant amount without sacrificing the security FDIC insurance provides. Exploiting different ownership categories is another strategy to extend your FDIC coverage. The FDIC provides separate coverage for different categories of ownership, such as single accounts, joint accounts, revocable trust accounts, and certain types of retirement accounts. By having different types of accounts, even within the same bank, you can multiply your coverage. It's essential to manage this carefully, ensuring you don't exceed the coverage limit in any category at any single bank. FDIC insured CDs present a secure and stable investment opportunity that offers predictable returns with a guaranteed rate of interest for a specific term. Despite certain limitations, such as potential early withdrawal penalties and inflation risk, they are particularly suitable for those with a risk-averse financial outlook or those seeking a consistent, reliable element in their broader investment portfolio. Additionally, strategic deployment of funds across different banks and account types can help maximize the coverage of FDIC insurance. As such, when considering your financial future, the purchase of an FDIC-insured CD can be a savvy move. To get started, reach out to a reputable banking institution today to discuss CD options that align with your specific financial goals. Taking this step can give you peace of mind knowing that your hard-earned money is secure and working for you.Certificate of Deposit (CD) Overview

Understanding FDIC Insured CDs

Role of FDIC Insurance

How FDIC Insurance Applies to CDs

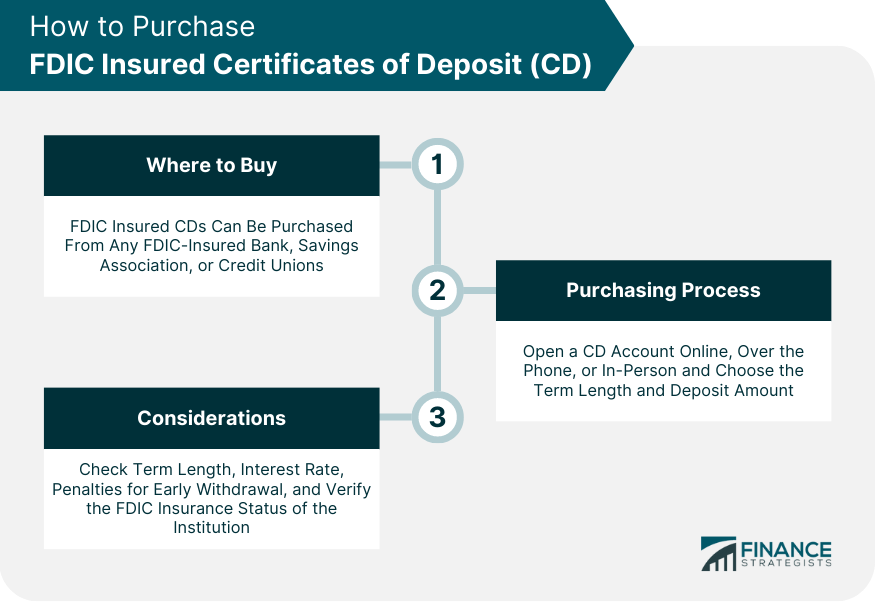

How to Purchase FDIC Insured CDs

Where to Buy

Purchasing Process

Key Factors to Consider Before Buying

Term Length

Interest Rate

Early Withdrawal Penalties

FDIC Insurance

Insurance Limit

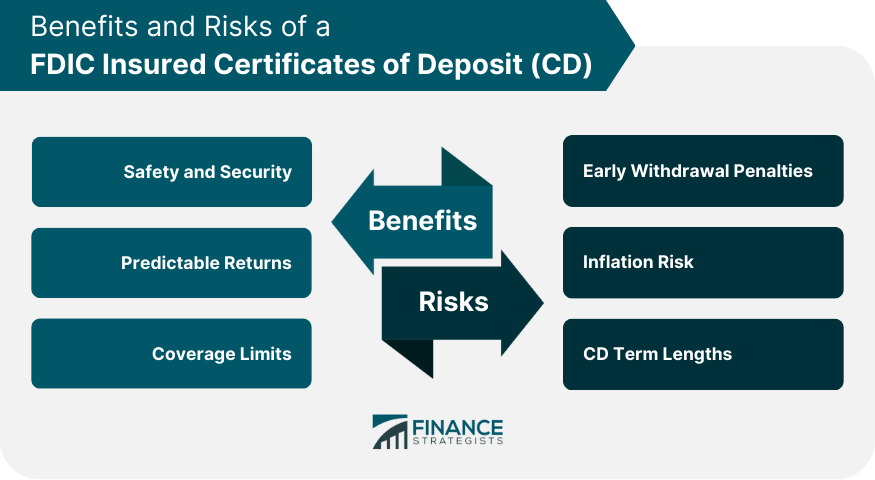

Benefits of FDIC Insured CDs

Safety and Security

Predictable Returns

Coverage Limits

Risks and Considerations for FDIC Insured CDs

Early Withdrawal Penalties

Inflation Risk

CD Term Lengths

Tips for Maximizing FDIC Coverage

Spreading Deposits Across Multiple Banks

Using Different Ownership Categories

Final Thoughts

Understanding FDIC Insured CDs FAQs

An FDIC insured CD is a time deposit with a fixed term at a bank insured by the Federal Deposit Insurance Corporation, ensuring up to $250,000 protection.

FDIC insured CDs offer predictable returns, safety, and security. They are a risk-free investment as the FDIC covers up to $250,000 per depositor, per bank.

FDIC insured CDs can be purchased at any FDIC-insured bank, savings association, or credit unions with similar protection. They can be bought in-person or online.

Risks include early withdrawal penalties and potential inflation risk. If withdrawn before maturity, penalties may apply, and high inflation could surpass the return rate.

Maximize FDIC coverage by spreading your deposits across multiple banks and using different ownership categories, as each bank and category carries separate coverage.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.