Churning refers to the practice of excessive trading in a client's investment account, primarily for the purpose of generating commissions for the financial advisor or investment broker. This unethical activity not only violates regulatory rules but also erodes investor trust in the financial industry. This is because a client's account may incur high trading costs and commissions as a result of churning, ultimately eroding the value of their investments. It is important for investors to be aware of the signs of churning, including excessive trading activity, high trading costs, and lack of transparency or communication from their financial advisor or investment broker. By being vigilant and conducting due diligence, investors can avoid falling victim to this unethical practice. For investors, it is crucial to be aware of churning as it can have a significant negative impact on their investments. The excessive trading can erode portfolio returns, resulting in a lower overall investment performance. Additionally, the frequent buying and selling of securities can incur unnecessary fees and taxes, further reducing the returns. On the other hand, financial professionals must also understand churning to maintain ethical business practices. Engaging in churning can lead to legal consequences such as fines, penalties, and even damage to their reputation. Therefore, having a clear understanding of what constitutes churning and avoiding such practices is crucial for maintaining a strong and ethical reputation in the industry. There are several types of churning, each with unique characteristics and implications. This section discusses churning in brokerage accounts, mutual funds, and insurance policies. Excessive trading and unsuitable investments are two forms of churning in brokerage accounts. Excessive trading occurs when a broker executes an unusually high number of trades, while unsuitable investments involve recommending products that do not align with a client's risk tolerance. Market timing and late trading are two types of churning specific to mutual funds. Market timing involves frequent buying and selling of mutual fund shares to exploit short-term price fluctuations, while late trading is the illegal practice of submitting orders after the market has closed to take advantage of late-breaking news. Twisting and replacing are two forms of churning in insurance policies. Twisting refers to the act of convincing a policyholder to replace their existing policy with a new one from the same insurer, while replacing involves switching to a new policy from a different insurer, often without fully disclosing the implications. Churning is governed by various regulatory bodies and legal frameworks, including the SEC, FINRA, and state securities regulators. This section discusses the role of these entities in addressing churning and the relevant regulations. The Securities and Exchange Commission (SEC) is responsible for enforcing federal securities laws and regulating the securities industry. It investigates and prosecutes instances of churning to protect investors and maintain market integrity. Financial Industry Regulatory Authority (FINRA) is a self-regulatory organization that oversees brokerage firms and their registered representatives. It enforces rules related to churning, and financial professionals found guilty of churning can face sanctions, fines, and other penalties. State securities regulators are responsible for enforcing state securities laws, which often include provisions relating to churning. They work alongside federal regulators to ensure the integrity of the securities industry and to protect investors from fraudulent activities. Investors and financial professionals can take various steps to detect and prevent churning. This section highlights warning signs for investors and best practices for financial professionals. High turnover ratios, excessive fees and commissions, and unexplained performance declines are all warning signs of potential churning. Investors should monitor their accounts regularly and question their financial advisors if they notice any of these red flags. Adhering to Know Your Client (KYC) rules, considering fee-based versus commission-based accounts, and maintaining ongoing communication and monitoring can help financial professionals prevent churning. These best practices ensure that clients' interests are prioritized and that ethical standards are upheld in the financial industry. Churning can have significant financial and legal consequences for both investors and financial professionals. This section examines the impact of churning on investor returns and the potential repercussions for financial professionals. Reduced portfolio returns and increased taxes and fees are two primary financial consequences of churning for investors. Excessive trading can diminish long-term investment returns, while unnecessary taxes and fees can further erode an investor's net worth. Fines and penalties, license suspension or revocation, and reputational damage are potential consequences for financial professionals found guilty of churning. These sanctions serve as a deterrent against unethical practices and reinforce the importance of maintaining high ethical standards in the financial industry. Lessons learned from churning cases, and strategies for recovering losses can provide valuable insights for investors and financial professionals. Analyzing these cases can help to understand the various facets of churning and prevent future occurrences. Churning cases offer valuable lessons for investors and financial professionals. One key lesson is the importance of due diligence. Investors must conduct thorough research before selecting a financial professional to work with. Additionally, financial professionals must conduct a careful analysis of their clients' needs and investment objectives to avoid the temptation of excessive trading to generate commissions. Transparency and communication are also crucial, with financial professionals being honest about the risks and potential costs associated with investment strategies. Investors who have been victims of churning may pursue various strategies to recover their losses, including arbitration, mediation, or litigation. These avenues provide investors with the opportunity to seek compensation and hold unethical financial professionals accountable. Churning is an unethical practice of excessive trading in a client's investment account for the purpose of generating commissions for financial advisors or investment brokers. Churning violates regulatory rules and erodes investor trust in the financial industry. Investors should be aware of the signs of churning to avoid falling victim to this practice. It is also essential for financial professionals to understand churning to maintain ethical business practices and avoid legal consequences. There are different types of churning, including excessive trading, unsuitable investments, market timing, late trading, twisting, and replacing. Regulatory bodies such as the SEC, FINRA, and state securities regulators play a crucial role in addressing churning and enforcing relevant regulations. Investors and financial professionals can take various steps to detect and prevent churning, such as regular monitoring of accounts, adhering to KYC rules, and maintaining ongoing communication and monitoring. The consequences of churning can include reduced portfolio returns, increased taxes and fees, and potential legal and regulatory repercussions for financial professionals. Valuable lessons from churning cases, such as due diligence, transparency, and communication, can help prevent future occurrences of churning. Strategies for recovering losses, such as arbitration, mediation, or litigation, can provide investors with the opportunity to seek compensation and hold unethical financial professionals accountable.What Is Churning?

Importance of Understanding Churning

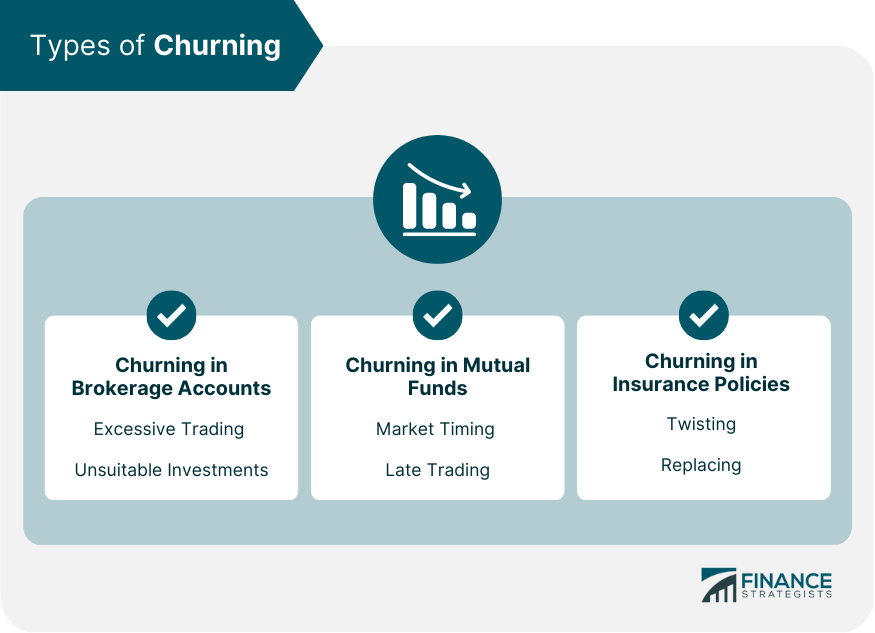

Types of Churning

Churning in Brokerage Accounts

Churning in Mutual Funds

Churning in Insurance Policies

Legal and Regulatory Framework

Securities and Exchange Commission (SEC) Regulations

Financial Industry Regulatory Authority (FINRA) Rules

State Securities Regulators

Detecting and Preventing Churning

Warning Signs for Investors

Best Practices for Financial Professionals

Consequences of Churning

Financial Impact on Investors

Legal and Regulatory Repercussions for Financial Professionals

Preventing and Addressing Churning

Lessons Learned From Churning Cases

Strategies for Recovering Losses

Conclusion

Churning FAQs

Churning is the practice of excessively buying and selling securities in a client's account to generate commissions for the broker.

Churning can result in high fees and losses for investors, as well as damage to the broker's reputation and potential legal consequences.

There are two types of churning: excessive trading churning, which involves frequent buying and selling, and volume churning, which involves trading in high volumes.

Churning can be detected by analyzing the frequency and volume of trades, as well as the cost-to-equity ratio of the account.

To prevent churning, investors should monitor their account activity, choose a reputable broker, and report any suspicious activity to regulatory authorities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.