The Employee Retention Tax Credit is an incentive established by the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) to help employers retain staff despite losing revenue during the pandemic. In 2020, eligible businesses qualified for a $5,000 per-employee tax credit. This amount was increased to $7,000 per employee every quarter, covering the first three quarters of 2021. The ERTC is entirely refundable and is applied to the employer's contribution to payroll taxes. To address the financial worries of many applicants, the Internal Revenue Service (IRS) also devised a program that allows qualified businesses to retroactively apply for this benefit. Throughout the pandemic, the ERTC guidelines have evolved with the release of new policies from the government. Below is a summary of some of the crucial changes made: Under this law, qualified employers could claim a credit equal to 50% of eligible wages paid between March 13, 2019, and December 31, 2020. The wage cap limit is up to $10,000, meaning a maximum of $5,000 credit may be claimed per employee for 2020. Unfortunately, companies that took out loans under the Paycheck Protection Program (PPP) were not eligible for the ERTC. Furthermore, businesses were subdivided into those with 100 or fewer employees and those with more than 100 employees. For the former, they could include all employees' wages in their computation. Meanwhile, only the wages of non-working staff due to the decline or suspension of business operations could be included for the latter. This second law extended ERTC into early 2021. This time, even employers who previously applied for PPP loans could now avail of the ERTC. The wage cap limit of $10,000 remained the same, but the credit increased to 70% of qualifying wages per quarter for the year. This change meant employers might claim a maximum of $7,000 credit for each employee per quarter. The limitation on the number of employees also increased. Thus, businesses with 500 or fewer employees could now include the wages of all employees in their computation. This act further extended the ERTC to the end of 2021. The wage cap limit and the credit rate remained the same. An additional directive was announced for recipients of either the Restaurant Revitalization Fund (RRF) or the Shuttered Venue Operators Grant (SVOG). They were advised not to use funds from these other programs to fulfill the wages already covered by the ERTC. This initiative moved up the end of ERTC by one quarter. Thus, most businesses could claim ERTC only up to the 3rd quarter of 2021. However, recovery start-up businesses were allowed to continue until the end of the year. They were also eligible for a credit of up to $50,000 for the third and fourth quarters. A business qualifies for the ERTC if they meet either of the criteria indicated by the IRS below: This criterion covers businesses whose operations were fully or partially suspended due to an executive order from an appropriate government body—limiting commerce, travel, or group meetings due to COVID-19. In 2020, these businesses must have experienced at least a 50% decline in gross receipts when comparing the current calendar period with the same one in 2019. Meanwhile, in 2021 these businesses must have experienced the same situation, only with a decline of at least 20% this time. If this test is failed, an alternative option for 2021 allows employers to compare the previous quarter's gross receipts to those of the same quarter in 2019 to determine if there is a reduction of 20% or greater. Claims are limited to businesses that meet either the government order test or the reduced gross receipts test. Government entities and sole proprietors are not eligible for the ERTC. However, self-employed persons who have staff on payroll may qualify. There was a change in the amount these businesses can claim from 2020 to 2021. In 2020 the credit rate was equal to 50% of the amount of the qualifying wages issued from March 13 to December 31. The wage limit was capped at $10,000, with a maximum credit of $5,000 per employee annually. For 2021, the credit was increased to 70% of the qualifying wages paid from January 1 to September 30. The wage limit was still at $10,000, with a maximum credit of $7,000 per employee per quarter. Below is a summary of the significant changes in the ERTC guidelines from 2020 to 2021. To claim the ETRC, eligible companies must indicate their total qualifying wages and related health insurance expenses for each quarter on their tax returns using Form 941. The credit is subtracted from the employer's part of the Social Security tax and Medicare tax. The excess is refundable if the total credit exceeds what they typically pay for both these taxes. In anticipation of claiming the credit, businesses may retain some funds for employment taxes equivalent to the ERTC without incurring a penalty instead of depositing them. Only employers with less than 500 full-time employees can obtain ERTC advance payments using IRS Form 7200. Although ERTC is no longer applicable for the 2022 tax year and onwards, qualified businesses may file for a retroactive refund using Form 941-X. This document adjusts taxes filed within either two years from the payment date or three years from the original tax return. Based on this timeline, some companies could still claim their retroactive refund up to the 2024 tax year, due on April 15, 2025. The IRS Notice 2021-20 stipulates guidelines for employers who wish to claim the ERTC. Most of this circular repeats FAQs that were published on their website. It also offers guidance to employers who received a PPP loan on how they can retroactively claim the employee retention tax credit. Several examples (Q&A No. 57) have been included to help illustrate the process. ERTC-qualified wages mentioned in the PPP loan forgiveness application may only be applied if more expenses than necessary were included in the calculation. However, eligible costs may not be retroactively added to the loan forgiveness application if the sole purpose is to claim the employee retention tax credit. The Employee Retention Tax Credit is an incentive initially established by the CARES Act to lessen the impact of COVID-19 and help businesses retain staff. The ERTC is entirely refundable and is applied to the employer's contribution of payroll taxes. To address the financial worries of many applicants, the Internal Revenue Service also devised a program that allows qualified businesses to apply for this benefit retroactively. An employer can be eligible for the ERTC if they meet either the government order test or the reduced gross receipts test. Policies for ERTC processing and available claims have undergone several changes from 2020 to 2021. Learning about these differences can make the application process easier for qualified employers.What Is the Employee Retention Tax Credit (ERTC)?

ERTC Background

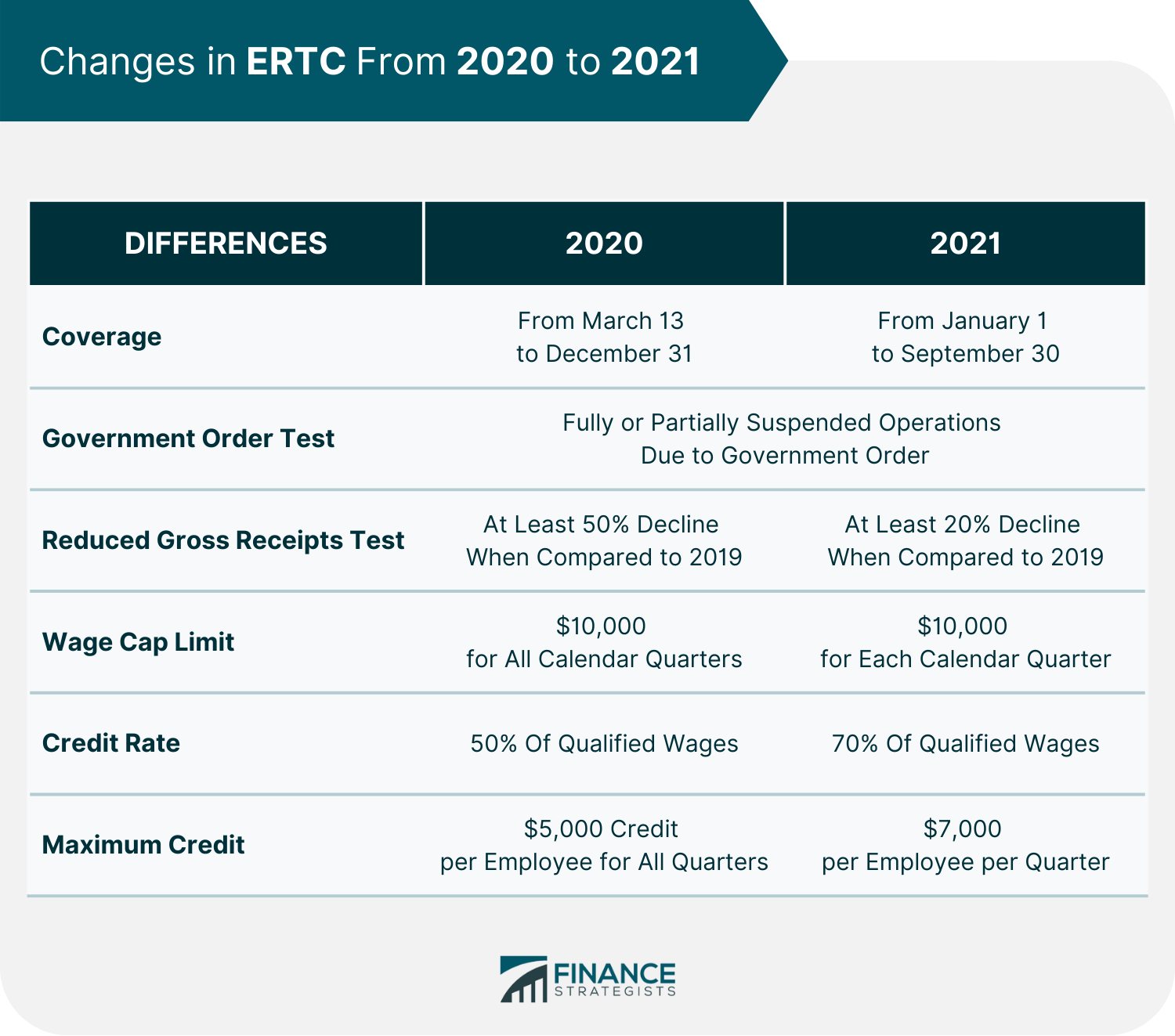

CARES Act 2020

Consolidated Appropriations Act 2021

American Rescue Plan Act 2021

Infrastructure Investment and Jobs Act

Eligibility for ERTC

Government Order Test

Reduced Gross Receipts Test

ERTC Claimable Amount

For 2020

For 2021

Filing for ERTC Claims

IRS New Guidelines for ERTC

The Bottom Line

Employee Retention Tax Credit (ERTC) FAQs

The Employee Retention Tax Credit (ERTC) is an incentive that encourages businesses to keep their employees despite the economic effects of the COVID-19 pandemic. Depending on the time period, qualified companies may take a tax credit of up to $7,000 per employee every quarter.

The purpose of ERTC is to help businesses keep their employees by providing a tax credit. The credit enables businesses to offset the cost of wages paid to employees during specific periods of the pandemic.

Businesses must have either experienced a significant decline in gross receipts or experienced government-imposed shutdowns, whether partially or entirely, to qualify for the ERTC.

The wage limit is consistently capped at $10,000. In 2020, qualified employers may claim up to 50% of qualifying wages for a maximum credit of $5,000 per employee annually. For 2021, it was increased to 70% for a full credit of $7,000 per employee per quarter.

Eligible companies must submit their total qualifying salaries and related health insurance expenditures for each quarter using Form 941. The credit is subtracted from the employer's portion of the Social Security tax and Medicare tax. Any excess is refundable if the credit surpasses the usual amount employers pay for this tax.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.