The Welfare and Pension Plans Disclosure Act (WPPDA) is a U.S. federal law enacted to safeguard workers' rights in employer-sponsored pension and welfare plans. The act mandates comprehensive disclosure of information regarding the operation and management of such plans. It covers a variety of pension plans, including defined benefit, defined contribution, profit-sharing, and stock bonus plans. The WPPDA requires plan administrators to periodically provide documents like summary plan descriptions, annual reports, and any plan modifications to participants and beneficiaries. These documents inform participants about their rights, benefits, and responsibilities under the plan. The impact of the WPPDA has been significant, enhancing transparency and accountability in the management of pension and welfare plans, thereby contributing to the financial security of millions of American workers. The enforcement and administration of WPPDA are overseen by three main regulatory authorities: the Department of Labor (DOL), the Internal Revenue Service (IRS), and the Pension Benefit Guaranty Corporation (PBGC). One of the key welfare plans covered by the WPPDA includes those providing medical, surgical, or hospital care benefits. This includes plans that offer comprehensive health coverage, as well as those that provide specific health benefits like dental or vision care. The WPPDA mandated full transparency of the terms of these plans and their financial conditions. The WPPDA also encompassed welfare plans that provided benefits in cases of sickness, accident, or disability. These plans, often referred to as disability insurance, offer income protection to employees who become unable to work due to an illness or injury. Another type of welfare plan covered by the WPPDA is unemployment benefit plans. These plans provide financial support to employees who lose their jobs without fault of their own. They are designed to help mitigate the financial stress of job loss until the employee finds new employment. The WPPDA also applied to other specified benefits, such as vacation benefits, daycare facilities, scholarship funds, prepaid legal services, or any benefits described in section 302(c) of the Labor Management Relations Act. The WPPDA applies to both defined benefit and defined contribution pension plans, including but not limited to: Traditional pension plans, also known as defined benefit plans, are employer-sponsored retirement plans. Under this plan, the employer guarantees a specific benefit amount to employees upon retirement. 401(k) plans are popular retirement savings vehicles offered by many employers. These plans are defined contribution plans, which means that the retirement benefit is determined by the contributions made and the investment performance of individual accounts. Employees can contribute a portion of their salary to their 401(k) account on a pre-tax basis, reducing their taxable income. Profit-sharing plans are retirement plans that allow employers to share a portion of their profits with employees. Employers make contributions to the plan based on the company's profitability. The contributions are typically allocated among employees based on factors such as salary or years of service. Employee Stock Ownership Plans (ESOPs) are unique retirement plans that enable employees to become partial owners of the company they work for. Under an ESOP, the company contributes its stock or cash to a trust, which holds the assets on behalf of the employees. The Summary Plan Description is a critical document under the WPPDA. It provides a comprehensive overview of the welfare or pension plan, including benefits, eligibility criteria, and methods for calculating those benefits. It should be written in a language easily understood by the average plan participant. Form 5500 is a mandatory annual report submitted to the Department of Labor. It provides detailed financial information about the plan, including its assets, liabilities, income, and expenses. It may also include data on the plan's insurance contracts and investment activities. The Summary Annual Report is a narrative summary of the plan's Form 5500. It provides a simplified overview of the financial status of the plan. The SAR must be distributed to all plan participants and beneficiaries annually. Under the WPPDA, plan administrators must make available key plan documents upon request. These include trust agreements, contracts, collective bargaining agreements, and other instruments under which the plan is established or operated. These documents allow participants to better understand their rights and the plan's obligations. Non-compliance with WPPDA requirements can lead to severe consequences for plan administrators, including civil and criminal penalties. Failure to provide the required disclosures or furnish requested documents can result in fines or imprisonment. Additionally, plan participants may seek legal remedies, such as suing for benefits due, obtaining injunctions, or recovering damages caused by a fiduciary's breach of duty. Ensuring adherence to WPPDA regulations is crucial to protect both plan participants and administrators from potential legal and financial repercussions. The DOL plays a crucial role in the enforcement and administration of WPPDA through its Employee Benefits Security Administration (EBSA). EBSA oversees compliance with WPPDA requirements, conducts investigations, and imposes penalties for non-compliance. The IRS is responsible for ensuring that pension plans comply with the tax-related provisions of WPPDA and the Internal Revenue Code (IRC). This includes verifying that plans maintain their tax-qualified status and adhere to contribution limits and other requirements. The PBGC is a government agency that provides insurance for defined benefit pension plans. Its role in WPPDA enforcement includes monitoring plan funding levels and taking action to protect plan participants and beneficiaries in case of plan termination or insolvency. WPPDA ensures that employees and beneficiaries have access to essential information about their welfare and pension plans, allowing them to make informed decisions about their benefits. Additionally, the act provides legal recourse for plan participants and beneficiaries in case of non-compliance by employers and plan administrators. WPPDA promotes transparency and accountability, empowering employees and beneficiaries with the information they need to understand their benefits and make informed decisions. This, in turn, can lead to increased satisfaction and confidence in their welfare and pension plans. WPPDA encourages employers and plan administrators to maintain organized, well-documented plans, fostering trust between employees and their benefit providers. While compliance with WPPDA requirements may entail additional administrative responsibilities, the benefits of transparency and accountability ultimately outweigh the costs. WPPDA plays a vital role in upholding transparency and accountability in the management of welfare and pension plans. By mandating disclosure requirements and imposing penalties for non-compliance, the act ensures that employers and plan administrators prioritize the best interests of plan participants and beneficiaries. ERISA is a federal law enacted in 1974 that sets minimum standards for welfare and pension plans in the private sector. While WPPDA focuses on disclosure requirements, ERISA addresses a broader range of issues, including fiduciary responsibilities, funding requirements, and participant rights. WPPDA and ERISA work together to protect the interests of employees and beneficiaries in the realm of employee benefit plans. The IRC governs the tax treatment of welfare and pension plans, including the tax-qualified status of pension plans and the tax-exempt status of certain welfare plan benefits. WPPDA and the IRC intersect in the regulation of pension plans, ensuring that plans adhere to tax-related requirements and maintain their tax-qualified status. The ACA, enacted in 2010, is a comprehensive healthcare reform law that affects the provision of health insurance and healthcare services in the United States. WPPDA and the ACA intersect in the area of health and welfare plans, with both laws working together to protect plan participants and beneficiaries by ensuring transparency, accessibility, and affordability of health benefits. As the employee benefits landscape continues to evolve, it is essential to periodically review and update WPPDA to address emerging trends and challenges. Potential amendments to the act may focus on enhancing disclosure requirements, streamlining reporting processes, and strengthening enforcement mechanisms. Several trends and challenges in the employee benefits space have implications for the future of WPPDA. These include the rise of gig economy workers and their access to benefits, the increasing complexity of pension plans, and the growing prevalence of financial wellness programs as part of employee benefit packages. Advancements in technology have the potential to transform the enforcement and administration of WPPDA. Digital tools can streamline the process of generating and distributing disclosure documents, facilitate the monitoring of plan compliance, and enhance communication between regulatory authorities, employers, and plan participants. The Welfare and Pension Plans Disclosure Act (WPPDA) is a pivotal piece of legislation in the U.S. ensuring transparency and protection for participants in various pension plans, including defined benefit, defined contribution, profit-sharing, and stock bonus plans. The act imposes stringent disclosure requirements on plan administrators, mandating them to furnish critical documents like summary plan descriptions, annual reports, and notices of plan changes. This comprehensive disclosure framework allows participants to stay informed about their rights, benefits, and obligations. The WPPDA has had a profound impact, fundamentally enhancing accountability and openness in pension and welfare plan administration. This transparency assures the financial security of American workers and inspires confidence in these plans. The WPPDA's influence extends beyond its immediate provisions, serving as a cornerstone for subsequent legislative efforts aimed at bolstering retirement security.Definition of Welfare and Pension Plans Disclosure Act

Types of Welfare Plans Covered by WPPDA

Health Insurance Plans

Disability Insurance Plans

Unemployment Benefits

Severance Pay Plans

This extensive coverage ensured that a variety of employee welfare plans were held to the same transparency and disclosure standards.Types of Pension Plans Covered by WPPDA

Traditional Pension Plans

401(k) Plans

Profit-Sharing Plans

Employee Stock Ownership Plans (ESOPs)

Disclosure Requirements for Welfare and Pension Plans Under WPPDA

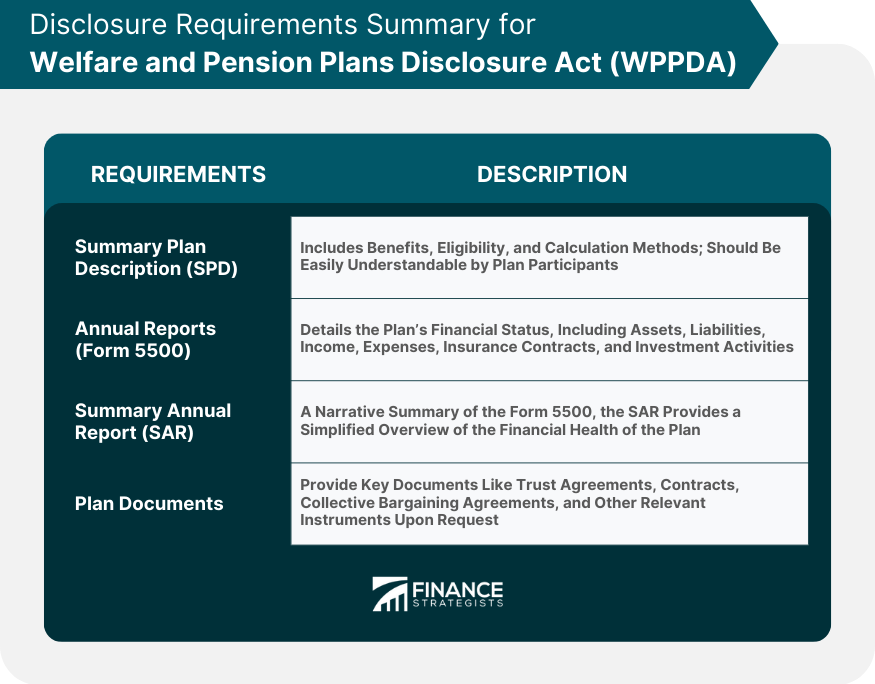

Summary Plan Description (SPD)

Annual Reports (Form 5500)

Summary Annual Report (SAR)

Plan Documents

Penalties for Non-compliance With WPPDA Requirements

WPPDA Enforcement and Administration

Department of Labor (DOL)

Internal Revenue Service (IRS)

Pension Benefit Guaranty Corporation (PBGC)

Employee Rights and Protections Under WPPDA

Impact of Welfare and Pension Plans Disclosure Act

Effects on Employees and Beneficiaries

Effects on Employers and Plan Administrators

WPPDA's Role in Promoting Transparency and Accountability

Relationship Between WPPDA and Other Relevant Laws

Employee Retirement Income Security Act (ERISA)

Internal Revenue Code (IRC)

Affordable Care Act (ACA)

Future Developments and Challenges in WPPDA

Potential Amendments and Updates to WPPDA

Emerging Trends and Challenges in Welfare and Pension Plans

Impact of Technology on WPPDA Enforcement and Administration

Conclusion

Welfare and Pension Plans Disclosure Act FAQs

The Welfare and Pension Plans Disclosure Act (WPPDA) is a U.S. federal law that was enacted in 1958. Its purpose is to ensure that employee benefit plans are properly funded, adequately insured, and accurately disclosed to participants.

The WPPDA applies to employee benefit plans that provide pension benefits or welfare benefits, including health plans, disability plans, and life insurance plans.

Under the Welfare and Pension Plans Disclosure Act (WPPDA), there were several disclosure requirements designed to ensure transparency and accountability in the administration of welfare and pension plans: Summary Plan Description (SPD), Annual Reports (Form 5500), Summary Annual Report (SAR), and Plan Documents.

The DOL is responsible for enforcing the WPPDA. It has the authority to investigate complaints, conduct audits, and impose penalties for noncompliance.

Employers who fail to comply with the WPPDA can be subject to civil penalties, including fines and injunctions. In extreme cases, employers may face criminal penalties for knowingly providing false or misleading information to plan participants.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.