Section 409A of the Internal Revenue Code (IRC) is a federal law governing Nonqualified Deferred Compensation (NQDC) plans. Enacted in 2004, it aims to ensure that deferred compensation is taxed appropriately and fairly. Compliance with Section 409A is crucial for both employers and employees to avoid severe tax penalties and other negative consequences. Section 409A applies to various types of NQDC plans, including traditional deferred compensation arrangements, equity-based awards such as stock options and restricted stock units, and certain severance arrangements. It covers both formal and informal plans and agreements that provide for the deferral of compensation, regardless of whether they are written or unwritten. The 409A regulations encompass a wide range of compensation arrangements, including salary deferral arrangements, bonus plans, long-term incentive plans, supplemental executive retirement plans (SERPs), and change in control agreements. Additionally, certain types of non-employee compensation, such as director fees, may also be subject to 409A compliance. Section 409A does not apply to qualified retirement plans, such as 401(k) plans and pension plans, as they are subject to separate IRC provisions. Additionally, some arrangements, like short-term deferrals and certain stock option grants, may be exempt from Section 409A if they meet specific requirements. Section 409A requires that deferral elections be made before the year in which the compensation is earned, except for new hires and certain performance-based compensation. The regulations specify permissible distribution events, such as separation from service, death, disability, a specified time, a change in control event, or the occurrence of an unforeseeable emergency. Section 409A generally prohibits the acceleration of payment timing, except in limited circumstances and under specific conditions. If a "specified employee" of a publicly traded company separates from service, their deferred compensation must be subject to a mandatory six-month delay before distribution. The regulations contain various anti-abuse rules designed to prevent manipulation of the timing and form of payments. Many compliance issues arise from plan documents that do not meet the requirements of Section 409A. Employers should ensure that their plan documents contain appropriate provisions and language to comply with the regulations. Operational failures occur when an employer fails to follow the terms of a compliant plan document. Employers must consistently and accurately administer their plans to avoid operational failures. Stock options and other equity awards must be granted with an exercise price no less than the fair market value (FMV) of the underlying stock on the grant date. Failure to use an appropriate valuation method can result in non-compliance with Section 409A. A certain change in control events, such as mergers or acquisitions, can trigger 409A compliance issues if not properly addressed in plan documents. Severance agreements are subject to Section 409A if they provide deferred compensation. Employers should carefully structure these agreements to comply with the regulations. Companies must comply with the requirements set forth in Section 409A to avoid penalties and consequences. Here is a checklist of key components to consider when ensuring compliance: Companies must establish procedures for employees to make deferral elections for compensation subject to Section 409A. These procedures must be in writing, and the employee's election must be made before the beginning of the year in which the compensation would be earned. Companies must establish rules for when distributions will be made to employees for compensation that is subject to Section 409A. These rules must be in writing, and the distribution must occur according to a fixed schedule or a specified event. Companies must establish procedures for employees to make subsequent deferral elections for compensation subject to Section 409A. These procedures must be in writing, and the employee's election must be made at least 12 months before the date of the first scheduled payment. Companies must establish rules for valuing the compensation subject to Section 409A, which may require the use of an independent appraiser. Valuations must be done in good faith and must be reasonable. Companies must provide employees with written disclosures regarding their rights and obligations under Section 409A. This includes information on how deferral elections work, when distributions will be made, and the consequences of non-compliance. Companies must maintain accurate records of their compliance with Section 409A. These records should include documentation of deferral elections, distribution schedules, valuations, and disclosures. Employers should periodically review their plan documents to ensure ongoing compliance with Section 409A. Training employees responsible for administering NQDC plans can help prevent operational failures and other compliance issues. Establishing and maintaining internal controls can help employers monitor and manage 409A compliance effectively. Consulting with legal, accounting, and valuation experts who can provide valuable insights and assistance in ensuring 409A compliance. Employers should stay informed about any updates to Section 409A regulations and related legislation to maintain compliance. IRS Correction Programs: The Internal Revenue Service (IRS) offers various correction programs, such as the Voluntary Compliance Program (VCP), to help employers correct 409A violations and minimize penalties. Self-Correction Methods: In some cases, employers may be able to correct 409A violations using self-correction methods, such as amending plan documents or adjusting payment schedules. Consequences of Noncompliance: Noncompliance with Section 409A can result in significant tax penalties for employees, including immediate taxation of deferred amounts, a 20% additional tax, and potential interest charges. Reporting Requirements: Employers must report and withhold taxes related to 409A noncompliance as required by the IRS. 409A compliance is essential for organizations that offer nonqualified deferred compensation plans, as it helps them avoid significant tax penalties and other negative consequences for both employers and employees. Adherence to Section 409A of the Internal Revenue Code involves understanding and complying with key provisions, addressing common compliance issues, and implementing best practices such as regular plan document reviews, employee training, and robust internal controls. Employers should also monitor changes in regulations and legislation, remain aware of potential legislative changes, and consider the impact of emerging technologies on compliance efforts. By staying proactive and informed, organizations can effectively manage their deferred compensation arrangements and maintain compliance with Section 409A.409A Compliance Overview

Scope of Section 409A

Applicability to Nonqualified Deferred Compensation Plans

Inclusion of Various Types of Compensation Arrangements

Exceptions and Exemptions

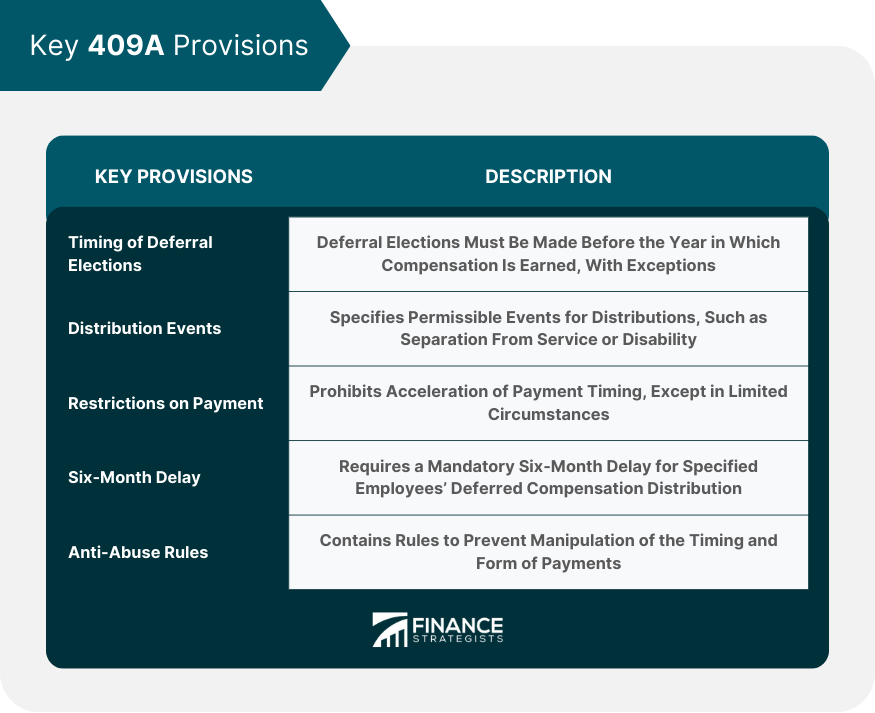

Key 409A Provisions

Timing of Deferral Elections

Distribution Events

Restrictions on Acceleration of Payments

Six-Month Delay for Specified Employees

Anti-Abuse Rules

Common 409A Compliance Issues

Non-Compliant Plan Documents

Operational Failures

Incorrect Valuation of Equity Awards

Change in Control Events

Severance Agreements

Compliance Checklist for Companies

Deferral Elections

Distribution Rules

Subsequent Deferral Elections

Valuation Rules

Disclosure Requirements

Recordkeeping

Best Practices for 409A Compliance

Regularly Review Plan Documents

Conduct Employee Training

Implement Robust Internal Controls

Engage External Experts for Guidance

Monitor Changes in Regulations and Legislation

Correcting 409A Violations

Bottom Line

409A Compliance FAQs

409A compliance refers to adhering to the rules and regulations set forth under Section 409A of the Internal Revenue Code, which governs nonqualified deferred compensation plans. Ensuring 409A compliance is crucial for employers and employees to avoid significant tax penalties and other negative consequences related to the deferral and distribution of compensation.

Various types of compensation arrangements are subject to 409A compliance, including salary deferral arrangements, bonus plans, long-term incentive plans, supplemental executive retirement plans (SERPs), change in control agreements, equity-based awards such as stock options and restricted stock units, and certain severance arrangements.

Employers can maintain 409A compliance by regularly reviewing plan documents, conducting employee training, implementing robust internal controls, engaging external experts for guidance, and monitoring changes in regulations and legislation related to Section 409A.

Noncompliance with Section 409A can result in severe tax penalties for employees, including immediate taxation of deferred amounts, a 20% additional tax, and potential interest charges. Employers may also face reputational damage, loss of key talent, and increased scrutiny from regulators.

Yes, employers can correct 409A violations using the IRS correction programs, such as the Voluntary Compliance Program (VCP), or through self-correction methods, such as amending plan documents or adjusting payment schedules. However, it is essential to consult with legal, accounting, and valuation experts to ensure that corrections are made appropriately and in compliance with Section 409A.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.