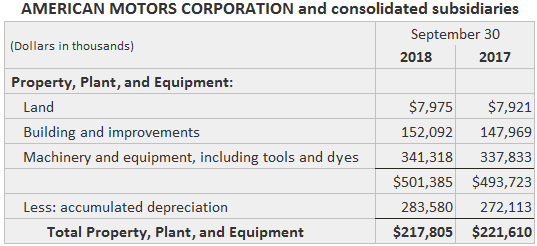

The term operating assets is used to identify the broad category of long-lived assets that are used to produce goods or services. This group includes not only tangible assets (often known as property, plant, equipment, or fixed assets) but also those that exist only as intangible rights (such as trademarks, patents, and goodwill). The category excludes assets that are held as investments and current assets and various miscellaneous items, such as long-term receivables and deferred charges. The acquisition and holding of operating assets influence short-run solvency somewhat negatively. This is because they require a long-term commitment of cash in order to provide their optimal use. Nevertheless, management is often willing to make this kind of long-term commitment because the assets are intended to boost earning power by improving the firm’s ability to provide goods and services. Long-run solvency is consequently strengthened through improved earning power. There are many types of information about operating assets that may be useful to the readers of financial statements. First, disclosures of the value committed by the firm to these assets help statement readers assess the potential earning power of the firm provided by its productive resources. The GAAP are presently structured such that the preferable amount to report is the assets’ book value, which is that portion of the original cost that has not yet been allocated to a period as an expense. Many participants have argued that a more direct measure of the assets’ current value should be used; also supplemental disclosure of estimates of those amounts, as well as the book value adjusted for inflation. The GAAP calls for the classification of operating assets on the balance sheet into appropriate categories based on tangibility or intangibility, their basic nature (such as land, buildings, and equipment), and the line of business in which they are used. The figure below shows American Motors Corporation’s balance sheet disclosure of operating assets. When completing a solvency assessment, companies disclose information about specific claims held against company assets by creditors through collateral agreements. In the event of insolvency, these claims entitle the holder to take possession of the asset or to receive cash from its sale. The current value disclosures required the objective of providing useful information for solvency assessments. An important accounting objective is the measurement of the expense incurred in the process of using an operating asset. Finally, the statement of changes in financial position (SCFP) presents information about the amount of working capital generated during a period by the sale of operating assets, as well as the amount used to acquire it. Since disposals are beyond the primary activities of the firm, information about the proportionate amount of the total funds provided by this source is helpful in assessing solvency. Acquisitions are representative of commitments to future activity and growth, and so information about their amounts is also important for assessing the firm’s future solvency and earning power.Operating Assets: Definition

Operating Assets: Explanation

Accounting Objectives

Example

Operating Assets FAQs

This group includes not only tangible assets (often called property, plant, equipment, or Fixed Assets) but also those that exist only as intangible rights (such as trademarks, patents, and goodwill). The category excludes assets that are held as investments and will be disposed of in the near future.

Intangible assets (usually called “intangibles”) represent legal or contractual rights to something other than physical resources. The most common forms are patents, copyrights, franchises, goodwill, trademarks and trade names. Intangible assets can be bought or sold just like tangible assets.

Operating assets account for 80% of all business’s year-end balance sheets.

No, non-operating assets are usually not disclosed unless they exceed one percent of total assets.

If you have an asset that does not generate revenue for your company, then it is considered to be a non-operating asset. For example, leasehold improvements are non-operating assets because they are expenses used to increase the value of the property on which they sit. Equity's basic purpose is to represent ownership in an entity (i.e., stock).

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.