Noncurrent or long-term assets are those assets a company owns that are not expected to be converted into or used as cash within one year.

They typically have a life of more than one year and are not intended for resale. They are recorded in the balance sheet at their acquisition cost.

In order to line up the cost of using the asset with the length of time it generates revenue, noncurrent assets are capitalized rather than expensed in the year they are acquired.

This means that their costs are spread out, either through depreciation, amortization, or depletion, over their estimated useful lives.

Examples of noncurrent assets include equipment, furniture and fixtures, real estate, patents, trademarks, and long-term investments.

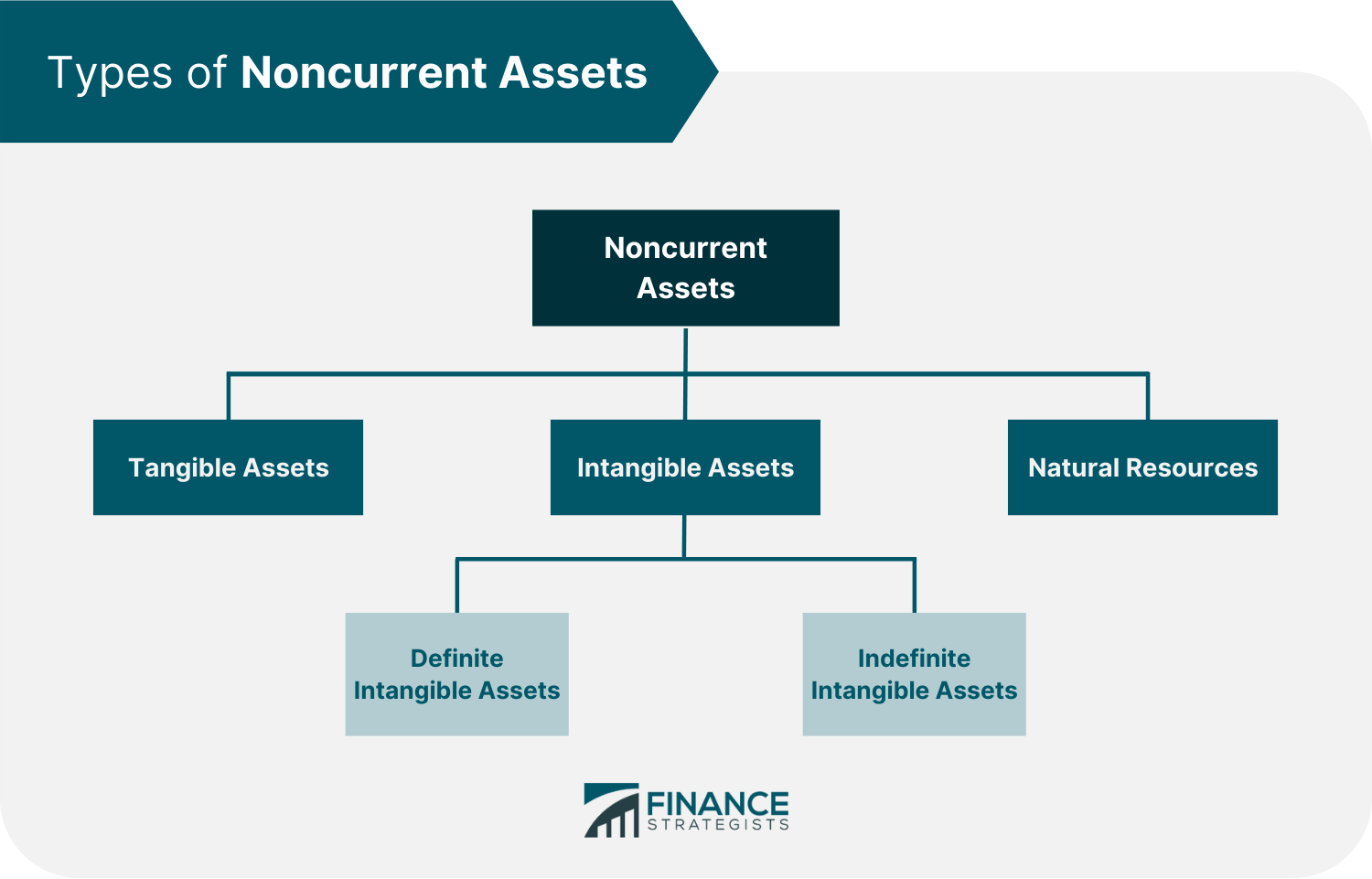

Types and Examples of Noncurrent Assets

There are three main types of noncurrent assets. These are tangible assets, intangible assets, and natural resources.

Tangible Assets

Tangible assets are physical properties that a company owns. They are necessary to the core business operations and are valued at their acquisition cost less accumulated depreciation.

However, tangible assets such as land may be revalued at their current market value.

Some major examples of tangible assets include:

Machinery and equipment

Real estate and associated improvements

Computers and software

Manufacturing tools

Vehicles

Furniture and fixtures

Intangible Assets

Intangible assets are those without a physical form but provide economic value. They may have a definite or indefinite useful life but cannot be seen, touched, or physically measured.

Businesses can create their own intangible assets, or they can acquire them through purchase or license.

Some examples of intangible assets include patents, goodwill, intellectual property, copyright, and trademarks.

Intangible assets can be classified into definite and indefinite tangible assets.

Definite Intangible Assets

A definite intangible asset has a limited useful life and only stays with the company for the duration stipulated in agreements or contracts.

For example, a business may purchase a patent with a life of 20 years, and the original creator of the said patent will remain the owner of the said patent.

Indefinite Intangible Assets

An indefinite intangible asset does not have a finite useful life and can provide benefits to the company as long as the company continues to exist.

An example of an indefinite intangible asset is goodwill. Goodwill is not amortized, but they are assessed each year for impairment which is when its carrying value exceeds the fair value of assets.

Natural Resources

Natural resources are assets that come from the earth, and they include timber, water, oil, and minerals.

They are also called wasting assets because they are used up or depleted when they are consumed.

These assets need to be consumed through extraction from the natural environment.

For instance, a mineral deposit must be mined in order to be used.

It means that these assets must be extracted out of the ground for them to be utilized.

Natural resources are listed on the balance sheet at the cost of extracting them from the ground, plus exploration and development costs, and less accumulated depletion.

Example of Noncurrent Assets

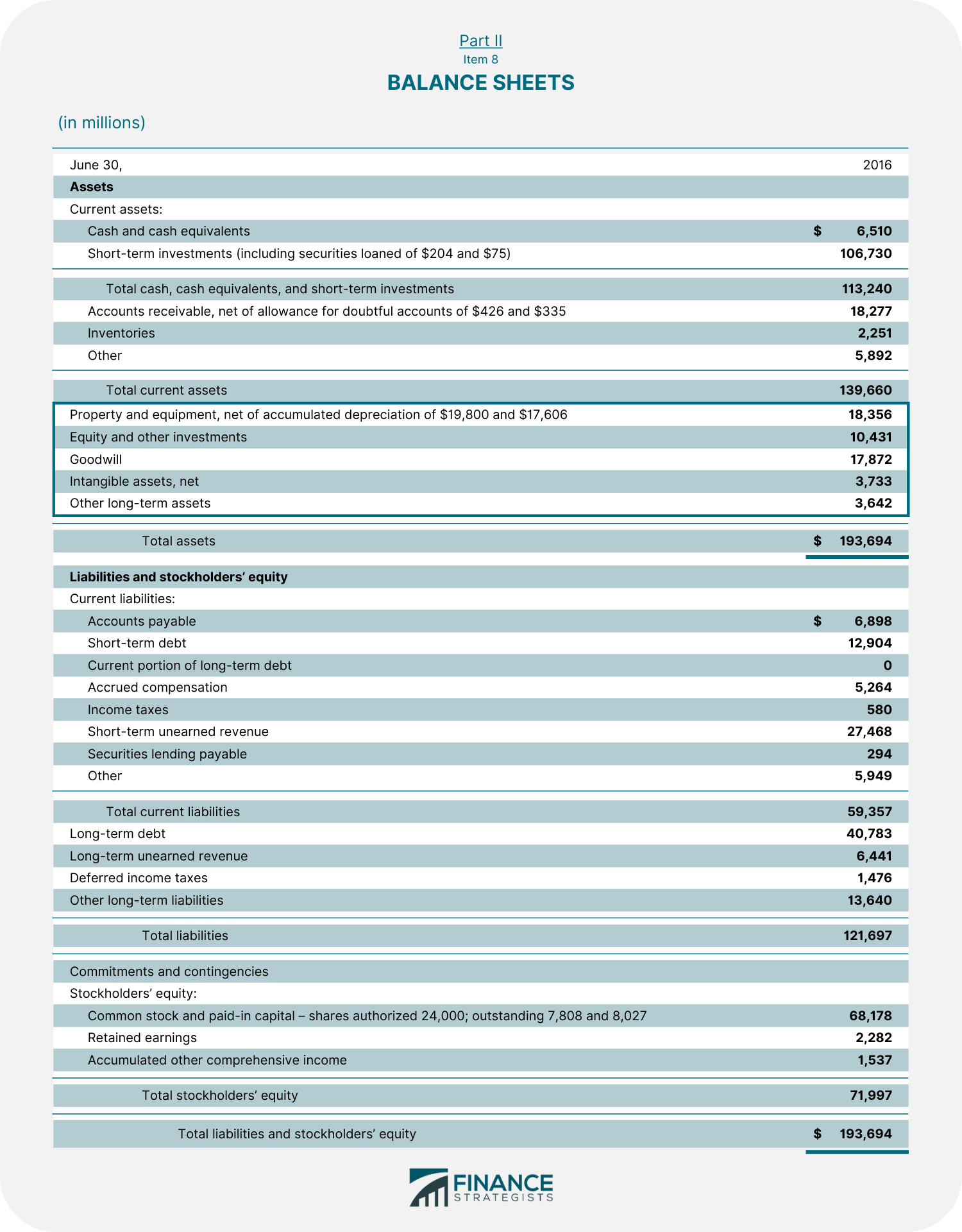

Below is a balance sheet from Microsoft Corporation for the year ended June 30, 2016.

Microsoft recorded total assets of $193,694,000.

Out of this total amount, noncurrent assets were $54,034,000.

A huge part of this amount is from the company’s property and equipment which accounted for nearly 34% of the total noncurrent assets figure.

Other noncurrent assets that the company owns are equity and other investments, goodwill, intangible assets, and other long-term assets.

How to Determine the Value of Noncurrent Assets

Noncurrent assets are reported on the balance sheet of a company at the price that was paid for them, adjusted to any depreciation and amortization that has been charged against them.

This is called the “net book value.”

Noncurrent assets are also subject to revaluation whenever the current market price decreases or increases compared to the book price.

Depending on the guideline used, noncurrent assets may be calculated through either the cost model approach or the revaluation model approach.

IAS 16 details the treatment for PP&E. Per US GAAP, only the cost model approach may be used in the valuation of PP&E.

As for intangible assets, IAS 38 allows for either cost or revaluation models.

A major disparity in accounting for intangible assets between the two standards is that, under IFRS, specific development costs can be capitalized.

Development costs are always expensed under US GAAP, with the exception of certain situations such as accounting for a business acquisition.

Both IFRS and US GAAP provide that research costs are to be expensed.

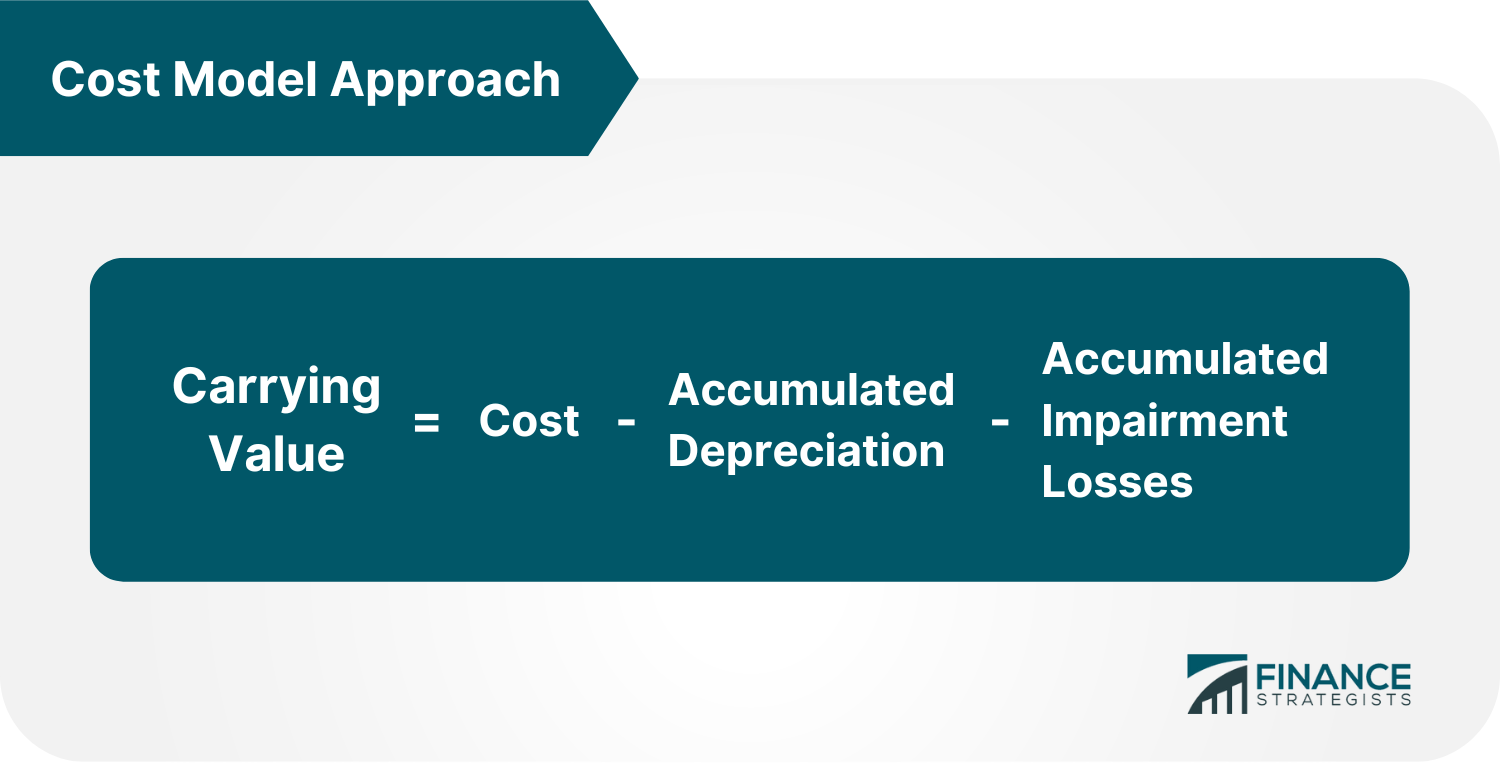

Cost Model Approach

The carrying value of an asset under the cost model is recognized at the net book value or carrying value, which is calculated as cost less accumulated depreciation and impairment losses.

Depreciation expense is the estimated reduction in the value of a fixed asset within a fiscal year.

An impairment loss is recognized when the carrying value of an asset exceeds its recoverable amount.

The recoverable amount is the higher of an asset’s fair value less costs to sell or its value in use.

For example, a company sold its equipment for $5,000 that had been in use for 3 years.

Additionally, it has the following data:

Acquisition cost: $20,000

Useful Life: 5 years

Impairment Loss: $5,000

Using the straight-line depreciation method, depreciation expense is $4,000 each year.

This makes the accumulated depreciation to be $12,000 for the past three years.

Depreciation = Cost of the Asset / Useful Life of the Asset

= $20,000 / 5

= $4,000

Accumulated Depreciation = Yearly Depreciation x Years in Use

= $4,000 x 3

= $12,000

Under the cost model approach, the equipment will be reported for $3,000.

Carrying Value = Cost – Accumulated Depreciation – Accumulated Impairment Losses

= $20,000 – $12,000 – $5,000

= $3,000

Upon sale of equipment for $5,000, the company will report a gain on sale of $2,000.

Gain on Sale = Amount of Property Sold – Carrying Value

= $5,000 – $3,000

= $2,000

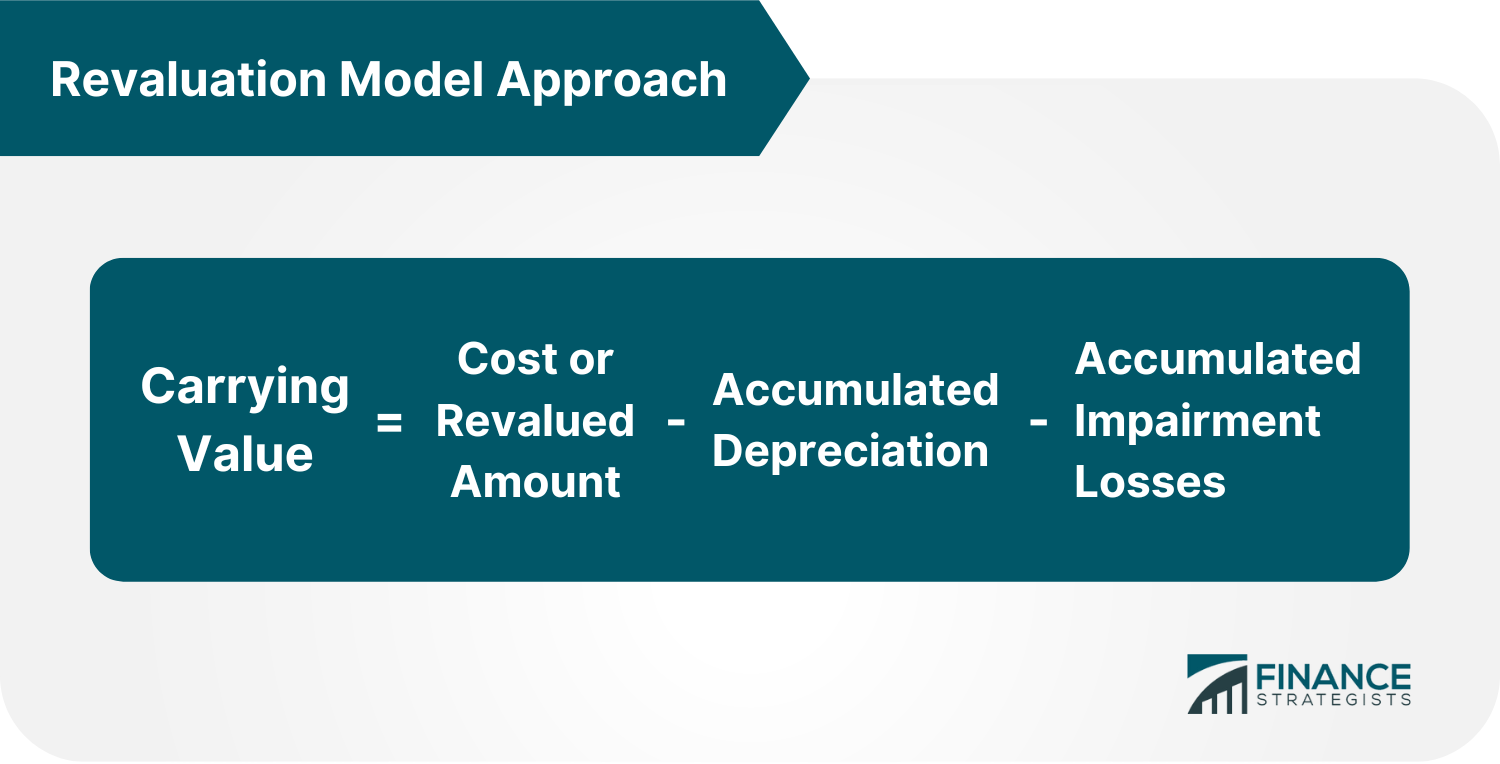

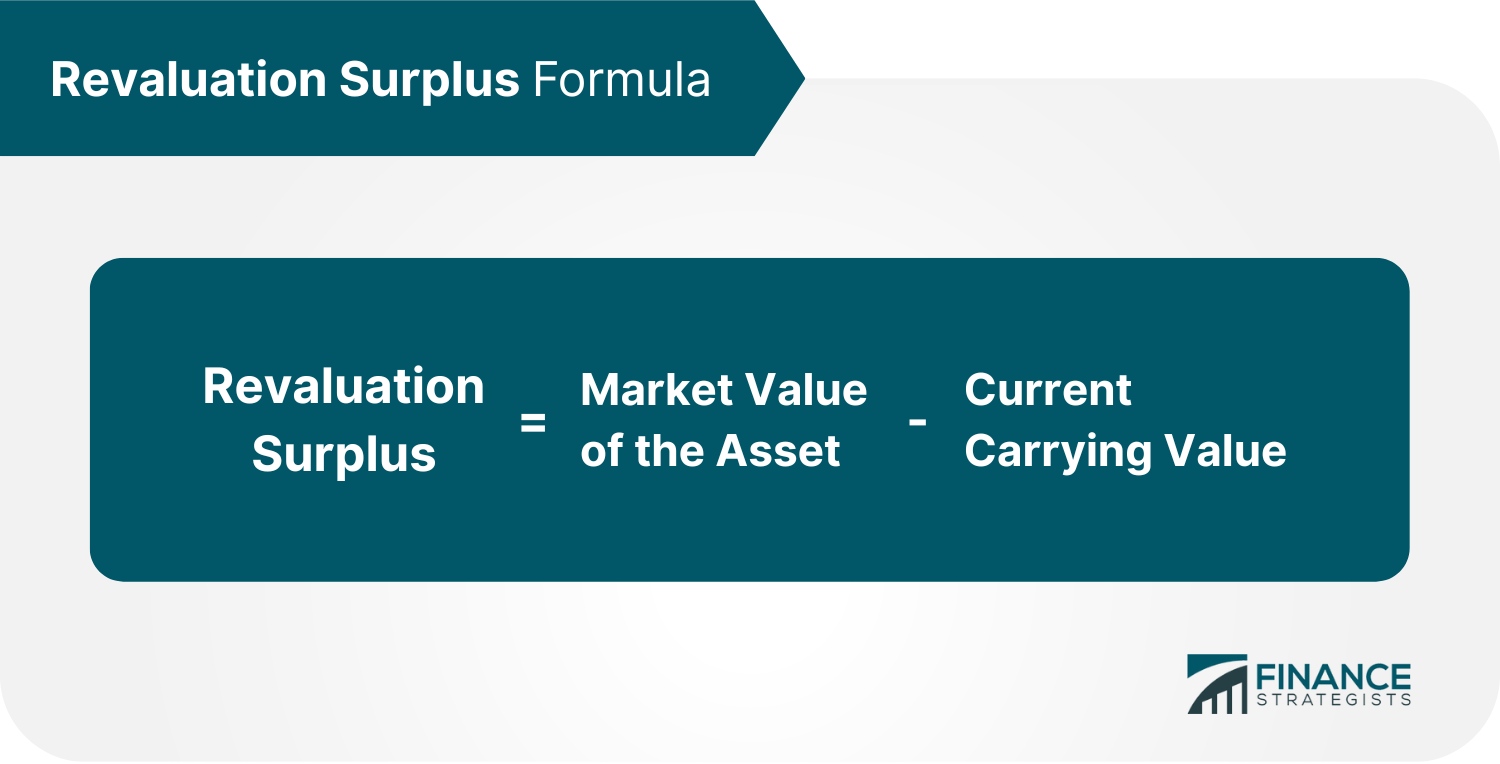

Revaluation Model Approach

The revaluation model carries the revalued amount of asset, which is fair value at the date of revaluation, less any subsequent accumulated depreciation and impairment losses.

Assets here shall be revalued with sufficient regularity, like 3 or 5 years, so that the carrying value of the assets will not so much differ from the fair value.

Because of this, revaluation may either result in a revaluation gain or revaluation loss.

Revaluation gain shall be recorded as other comprehensive income and will be reflected in the shareholder’s equity labeled as “revaluation surplus.”

On the other hand, revaluation loss shall be expensed in the income statement.

If the asset was previously revalued to revaluation surplus, then the decrease in carrying value shall be debited to equity to the extent of reversing such revaluation surplus.

Should there be an excess in revaluation loss, the same shall be expensed in the income statement.

Example 1:

A company’s equipment suffered a revaluation loss of $30,000 taking its book value from $90,000 to $60,000.

Below are its details:

Revalued Amount: $100,000

Accumulated Depreciation: $10,000

Net Book Value: $90,000

Revaluation Surplus: $20,000

Under the revaluation model approach, revaluation loss will be reported as follows:

Other Comprehensive Income: $20,000

Income Statement: $10,000

Example 2:

A company purchased equipment on March 25, 2019 for $20,000. The equipment’s fair market value is $16,000 as of February 28, 2020 and $21,000 as of February 28, 2021.

Under the revaluation model approach, revaluation gain will be reported as follows:

Revaluation gain recognized in the Income Statement (up to the revaluation loss recorded in the previous year) is $4,000.

Revaluation surplus to be recognized in Shareholder’s Equity is $1,000.

Cost Model vs. Revaluation Model

The cost model and revaluation model approach are two different methods of accounting for changes in the value of noncurrent assets.

However, the decision on which method should be used should be at the discretion of the management since they are both accepted standard accounting methods.

The revaluation model is better used when there is a reliable market estimate. This may be done by rigorously inspecting the market prices of similar noncurrent assets to arrive at a reliable value.

A company may use the cost model if they prefer a less complicated and fairly straightforward method of determining the value of its noncurrent assets.

Importance of Noncurrent Assets

Determining the value of the noncurrent assets of a company is important for a number of reasons.

Keeping Track of Assets

Companies need to keep track of their noncurrent assets because they represent a significant portion of the company’s total value.

For example, goodwill and intellectual property rights are considered to be some of the most valuable assets of a company.

As such, it is important for companies to have a clear understanding of the value of their noncurrent assets so that they can make informed decisions about how to best use them.

Risk Identification and Management

Another reason why determining the value of noncurrent assets is important is that it helps companies identify and manage risks associated with these assets.

For instance, if a company’s noncurrent assets are undervalued, it may be at risk of defaulting on its loans or not being able to meet its financial obligations.

On the other hand, if a company’s noncurrent assets are overvalued, it may be paying too much tax on these assets or may be at risk of losing these assets if they are sold.

More Accurate Financial Statements

Determining the value of noncurrent assets is important because it helps create more accurate financial statements.

This is because the value of these assets is used in the calculation of the net worth of a company.

As such, if the value of these assets is not accurately determined, it can lead to a false or misleading portrayal of the financial position of the company.

Further, you can also spot ghost assets, if any, such as stolen, lost, or damaged assets, which can help improve the asset management of your company.

Determining your current assets also helps prevent loss and theft and makes it easier to trace any missing items.

Better Decision-Making

Determining the value of noncurrent assets is important because it helps companies make better decisions about how to use these assets.

For instance, if a company knows that its noncurrent assets are undervalued, it may decide to sell these assets in order to raise capital.

On the other hand, if a company knows that its noncurrent assets are overvalued, it may decide to hold on to these assets and use them as collateral for loans.

In addition, knowing the value of noncurrent assets can also help companies make better decisions about how to invest these assets.

For instance, if a company knows that its land is undervalued, it may decide to invest in this asset by developing it or improving it.

Improved Investor Relations

Finally, determining the value of noncurrent assets is important because it can help improve a company’s relationships with its investors.

This is because investors often use the value of a company’s noncurrent assets when making investment decisions.

As such, if a company’s noncurrent assets are valued accurately, it can help improve the company’s relationships with its investors and potentially attract more investment.

Investors often invest in companies with strong noncurrent assets because they see these companies as being more stable and less risky.

This is because noncurrent assets tend to be more durable and have a longer lifespan than current assets.

Consequently, companies with strong noncurrent assets are often seen as being better able to weather economic downturns.

Noncurrent Assets vs. Current Assets

There are a few key differences between noncurrent assets and current assets.

Noncurrent assets are long-term investments and are not easily converted into cash.

They usually have a lifespan of more than one year.

Noncurrent assets include items such as land, buildings, equity investments, and patents.

Current assets are short-term investments that a company expects to convert into cash within one year.

Current assets include items such as cash, cash equivalents, marketable securities, prepaid expenses, accounts receivable, inventory, and other liquid assets.

Though they have differences, both are vital to a company. Noncurrent assets provide the foundation and long-term stability of a business, while current assets provide day-to-day liquidity.

The Bottom Line

Noncurrent assets are long-term investments that a company expects to convert into cash after more than one year.

It includes assets such as land, furniture, fixtures, buildings, equipment, patents, trademarks, and long-term investments.

There are three types of noncurrent assets, which are tangible, intangible, and natural resources.

Noncurrent assets are not as liquid as current assets because they cannot be easily converted into cash.

To determine the value of a noncurrent asset, companies can use the cost model or revaluation model. Management will decide which method is best based on its preference.

Noncurrent assets are important to a company because they provide the foundation and long-term stability of a business. They are also used to generate revenue and are a source of financing.

Noncurrent Assets FAQs

Noncurrent assets include assets such as land, furniture, fixtures, buildings, equipment, patents, trademarks, and long-term investments.

Noncurrent assets are long-term investments and are not easily converted into cash. They usually have a lifespan of more than one year. Current assets are short-term investments that a company expects to convert into cash within a year.

Noncurrent assets are the same as fixed assets. They are used by a company to produce goods and services and have a useful life of more than a year.

The decision on which method should be used to compute noncurrent assets (cost model vs. revaluation model) should be at the discretion of the management and should be based on its preference.

Noncurrent assets are important to a company because they describe the foundation and long-term stability of a business. They are also used to generate revenue and are a source of financing when the company requires to raise capital.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

Fact Checked

At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications.

They regularly contribute to top tier financial publications, such as The Wall Street Journal, U.S. News & World Report, Reuters, Morning Star, Yahoo Finance, Bloomberg, Marketwatch, Investopedia, TheStreet.com, Motley Fool, CNBC, and many others.

This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible.

Why You Can Trust Finance Strategists

Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year.

We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources.

Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos.

Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

How It Works

Step 1 of 3

01

Ask Any Financial Question

Ask a question about your financial situation providing as much detail as possible. Your information is kept secure and not shared unless you specify.

How It Works

Step 2 of 3

02

Our Team Will Connect You With a Vetted, Trusted Professional

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

How It Works

Step 3 of 3

03

Get Your Questions Answered and Book a Free Call if Necessary

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

Ask Any Financial Question

Ask Any Financial Question

Where Should We Send Your Answer?

Where Should We Send Your Answer?

Just a Few More Details

We need just a bit more info from you to direct your question to the right person.

Tell Us More About Yourself

Is there any other context you can provide?

Pro tip: Professionals are more likely to answer questions when background and context is given. The more details you provide, the faster and more thorough reply you'll receive.

Tell Us More About Yourself

What is your age?

Tell Us More About Yourself

Are you married?

Tell Us More About Yourself

Do you own your home?

Tell Us More About Yourself

Do you have any children under 18?

Tell Us More About Yourself

What is the approximate value of your cash savings and other investments?

Pro tip: A portfolio often becomes more complicated when it has more investable assets. Please answer this question to help us connect you with the right professional.

Tell Us More About Yourself

Would you prefer to work with a financial professional remotely or in-person?

Tell Us More About Yourself

What's your zip code?

Submit to get your question answered.

A financial professional will be in touch to help you shortly.

Part 1: Tell Us More About Yourself

What is your age?

Part 1: Tell Us More About Yourself

Are you married?

Part 1: Tell Us More About Yourself

Do you have any children under 18?

Part 1: Tell Us More About Yourself

Do you own a business?

Part 1: Tell Us More About Yourself

Which activity is most important to you during retirement?

Part 2: Your Current Nest Egg

Do you own your home?

Part 2: Your Current Nest Egg

What is the approximate value of your cash savings and other investments?

Pro tip: A portfolio often becomes more complicated when it has more investable assets. Please answer this question to help us connect you with the right professional.

Part 3: Confidence Going Into Retirement

How comfortable are you with investing?

Part 3: Confidence Going Into Retirement

How confident are you in your long term financial plan?

Part 3: Confidence Going Into Retirement

What is your risk tolerance?

Part 3: Confidence Going Into Retirement

How much are you saving for retirement each month?

Part 3: Confidence Going Into Retirement

How much will you need each month during retirement?

Part 4: Getting Your Retirement Ready

What is your current financial priority?

Part 4: Getting Your Retirement Ready

Do you already work with a financial advisor?

Part 4: Getting Your Retirement Ready

Which of these is most important for your financial advisor to have?

Part 4: Getting Your Retirement Ready

Would you prefer to work with a financial professional remotely or in-person?

Part 4: Getting Your Retirement Ready

What's your zip code?

Part 4: Getting Your Retirement Ready

Where should we send your answer?

Submit to get your retirement-readiness report.

A financial professional will be in touch to help you shortly.

Get In Touch With

Where Should We Send Your Answer?

Great! The Financial Professional Will Get Back To You Soon.

A financial professional will be in touch to help you shortly.

Where Should We Send The Downloadable File?

Great! Hit “Submit” and an Advisor Will Send You the Guide Shortly.

How It Works

Step 1 of 3

01

Create a Free Account and Ask Any Financial Question

Ask a question about your financial situation providing as much detail as possible. Your information is kept secure and not shared unless you specify.

How It Works

Step 2 of 3

02

Learn At Your Own Pace With Our Free Courses

Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals.

Get Started

Step 3 of 3

03

Get Your Questions Answered and Book a Free Call if Necessary

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

To Ensure One Vote Per Person, Please Include the Following Info

Where Should We Send Your Answer?

Great! Thank You for Voting.

A financial professional will be in touch to help you shortly.

Part 1: Tell Us More About Yourself

What is your age?

Part 1: Tell Us More About Yourself

Are you married?

Part 1: Tell Us More About Yourself

Do you have any children under 18?

Part 1: Tell Us More About Yourself

Do you own a business?

Part 1: Tell Us More About Yourself

Which activity is most important to you during retirement?

Part 2: Your Current Nest Egg

Do you own your home?

Part 2: Your Current Nest Egg

What is the approximate value of your cash savings and other investments?

Pro tip: A portfolio often becomes more complicated when it has more investable assets. Please answer this question to help us connect you with the right professional.

Part 3: Confidence Going Into Retirement

How comfortable are you with investing?

Part 3: Confidence Going Into Retirement

How confident are you in your long term financial plan?

Part 3: Confidence Going Into Retirement

What is your risk tolerance?

Part 3: Confidence Going Into Retirement

How much are you saving for retirement each month?

Part 3: Confidence Going Into Retirement

How much will you need each month during retirement?

Part 4: Getting Your Retirement Ready

What is your current financial priority?

Part 4: Getting Your Retirement Ready

Do you already work with a financial advisor?

Part 4: Getting Your Retirement Ready

Which of these is most important for your financial advisor to have?

Part 4: Getting Your Retirement Ready

Would you prefer to work with a financial professional remotely or in-person?

Part 4: Getting Your Retirement Ready

What's your zip code?

Part 4: Getting Your Retirement Ready

Where should we send your answer?

Submit to get your retirement-readiness report.

A financial professional will be in touch to help you shortly.

How It Works

Step 1 of 3

01

Ask Any Financial Question

Ask a question about your financial situation providing as much detail as possible. Your information is kept secure and not shared unless you specify.

How It Works

Step 2 of 3

02

Our Team Will Connect You With a Vetted, Trusted Professional

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

How It Works

Step 3 of 3

03

Get Your Questions Answered and Book a Free Call if Necessary

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

Ask Any Financial Question

Ask Any Financial Question

Where Should We Send Your Answer?

Where Should We Send Your Answer?

Just a Few More Details

We need just a bit more info from you to direct your question to the right person.

Tell Us More About Yourself

Is there any other context you can provide?

Pro tip: Professionals are more likely to answer questions when background and context is given. The more details you provide, the faster and more thorough reply you'll receive.

Tell Us More About Yourself

What is your age?

Tell Us More About Yourself

Are you married?

Tell Us More About Yourself

Do you own your home?

Tell Us More About Yourself

Do you have any children under 18?

Tell Us More About Yourself

What is the approximate value of your cash savings and other investments?

Pro tip: A portfolio often becomes more complicated when it has more investable assets. Please answer this question to help us connect you with the right professional.

Tell Us More About Yourself

Would you prefer to work with a financial professional remotely or in-person?

Tell Us More About Yourself

What's your zip code?

Submit to get your question answered.

A financial professional will be in touch to help you shortly.

Get in Touch With a Financial Advisor

Where Should We Send Your Answer?

Submit Your Info Below and Someone Will Get Back to You Shortly.

Get Faith-Based Legacy Planning

Message

Submit Your Info Below and Someone Will Get Back to You Shortly.