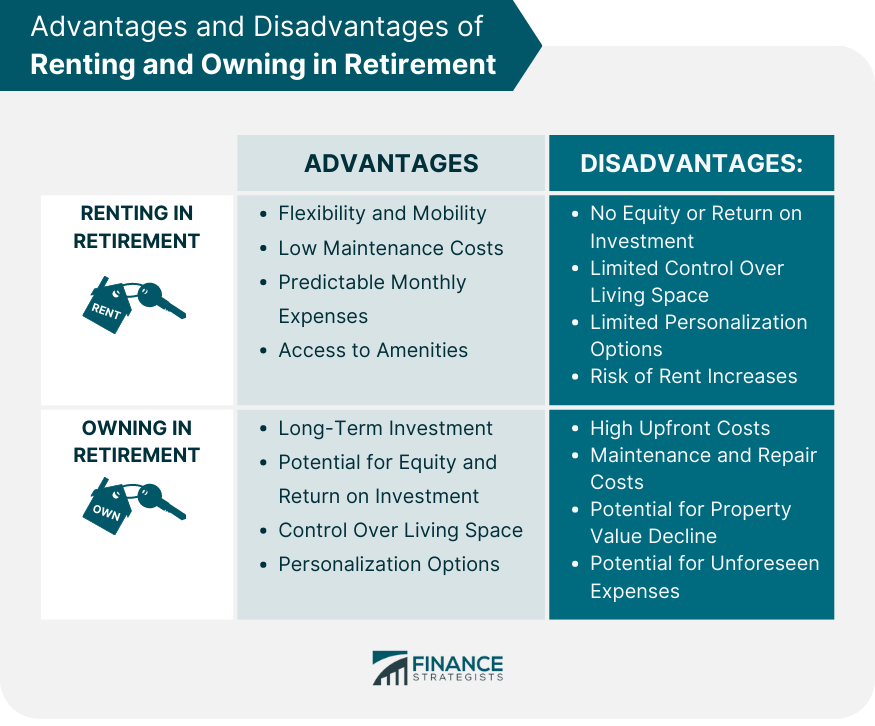

Renting in retirement refers to the act of leasing a living space, such as an apartment or a house, instead of owning it. In this arrangement, the tenant pays rent to the property owner in exchange for the right to live in the property for a specified period, usually on a monthly basis. Owning in retirement refers to the act of purchasing a living space, such as a house or a condo, and paying for it either outright or through a mortgage. In this arrangement, the owner has full control over the property and can make modifications, rent it out, or sell it as they see fit. Choosing between renting and owning a living space in retirement is a significant decision that can impact an individual's financial, emotional, and physical well-being. The decision must consider various factors, such as financial stability, personal preferences, and health needs, to ensure that it aligns with one's goals and lifestyle during retirement. Renting provides retirees with greater flexibility and mobility, as they are not tied down to a specific location or property. This can be especially beneficial for those who plan to travel frequently, move closer to family, or downsize to a smaller living space. Renting typically involves, as the property owner is responsible for repairs and upkeep. This can be advantageous for retirees who prefer to avoid the hassle and expense of maintaining a home, such as lawn care, cleaning, and repairs. Renting provides retirees with predictable monthly expenses, as they only need to pay rent and utilities, without worrying about unexpected repair costs or property tax increases. This can be especially beneficial for those on a fixed income or with limited financial resources. Many rental properties offer amenities, such as swimming pools, fitness centers, and community events, that may not be available or affordable for homeowners. This can provide retirees with access to social activities and recreational opportunities that can enhance their overall quality of life. Renting does not offer retirees the opportunity to build equity or receive a return on investment, as they are not investing in property ownership. This can be a disadvantage for retirees who value long-term financial stability and wealth-building. Renting provides tenants with limited control over their living space, as they must abide by the property owner's rules and restrictions. This can be a disadvantage for retirees who prefer to make modifications or customize their living space to suit their needs and preferences. Renting typically offers limited options for personalization or customization, as tenants must seek permission from the property owner to make changes. This can be a disadvantage for retirees who value individuality and self-expression. Renting carries the risk of rent increases, as property owners may raise the rent over time or at the end of the lease term. This can be a disadvantage for retirees on a fixed income or with limited financial resources, as it can make living expenses more unpredictable and difficult to manage. Owning a property in retirement can serve as a long-term investment, providing retirees with a potentially valuable asset that can appreciate over time. This can be beneficial for retirees who value financial stability and wealth-building. Owning a property offers retirees the opportunity to build equity and receive a return on investment, as property values can increase over time. This can be advantageous for retirees who prioritize long-term financial stability and independence. Owning a property provides retirees with greater control over their living space, as they can make modifications or renovations without seeking permission from a property owner. This can be beneficial for retirees who value individuality and self-expression. Owning a property offers retirees greater options for personalization and customization, as they can make changes to suit their needs and preferences without restriction. This can be beneficial for retirees who prioritize a sense of home and belonging. Owning a property typically involves high upfront costs, such as a down payment, closing costs, and property taxes. This can be a disadvantage for retirees with limited financial resources, as it can make property ownership more difficult or unaffordable. Owning a property requires ongoing maintenance and repair costs, as the owner is responsible for repairs and upkeep. This can be a disadvantage for retirees who prefer to avoid the hassle and expense of maintaining a home. Owning a property carries the risk of a potential property value decline, which can negatively impact the owner's financial stability and equity. This can be a disadvantage for retirees who prioritize long-term financial stability and wealth-building. Owning a property also carries the risk of unforeseen expenses, such as unexpected repairs or property damage. This can be a disadvantage for retirees with limited financial resources or who prefer to avoid financial uncertainty. One of the most critical factors to consider when choosing between renting and owning in retirement is one's financial situation. Retirees must assess their financial stability, resources, and goals to determine whether they can afford to own a property and manage the associated costs. Another essential factor to consider is one's health and mobility. Retirees must assess their ability to maintain a property, such as performing maintenance or cleaning, and determine whether renting or owning best aligns with their physical limitations. Retirees must also consider their future plans and goals, such as traveling, downsizing, or relocating. Renting may be more advantageous for those who plan to move frequently, while owning may be more beneficial for those who prioritize long-term financial stability and independence. Retirees must also consider their lifestyle and personal preferences, such as the importance of individuality, social connections, and recreational opportunities. Renting may offer more flexibility and access to amenities, while owning may offer greater personalization and control over one's living space. Choosing between renting and owning in retirement requires careful consideration of various factors, including financial stability, health and mobility, future plans and goals, and personal preferences. Renting offers greater flexibility and lower maintenance costs, while owning provides potential for long-term investment and greater control over one's living space. Both options carry advantages and disadvantages that retirees must weigh against their individual circumstances and priorities. To make an informed decision between renting and owning in retirement, retirees must assess their financial situation, health and mobility, future plans and goals, and personal preferences. By considering these factors, retirees can determine which option best aligns with their needs and priorities and make a choice that supports their financial, emotional, and physical well-being. Retirees should also regularly assess their living situation and adjust their housing arrangements as their circumstances change or evolve over time. Ultimately, the decision to rent or own in retirement should align with one's goals, values, and lifestyle to ensure a fulfilling and comfortable retirement experience.Overview of Renting and Owning in Retirement

Definition of Renting in Retirement

Definition of Owning in Retirement

Importance of Choosing Between Renting and Owning in Retirement

Advantages of Renting in Retirement

Flexibility and Mobility

Low Maintenance Costs

Predictable Monthly Expenses

Access to Amenities

Disadvantages of Renting in Retirement

No Equity or Return on Investment

Limited Control Over Living Space

Limited Personalization Options

Risk of Rent Increases

Advantages of Owning in Retirement

Long-Term Investment

Potential for Equity and Return on Investment

Control Over Living Space

Personalization Options

Disadvantages of Owning in Retirement

High Upfront Costs

Maintenance and Repair Costs

Potential for Property Value Decline

Potential for Unforeseen Expenses

Factors to Consider When Choosing Between Renting and Owning in Retirement

Financial Situation

Health and Mobility

Future Plans and Goals

Lifestyle and Personal Preferences

Conclusion

Renting vs Owning in Retirement FAQs

Renting in retirement offers greater flexibility, mobility, lower maintenance costs, predictable monthly expenses, and access to amenities.

Owning a home in retirement can lead to high upfront and maintenance costs, potential property value decline, and unforeseen expenses.

Consider factors such as your financial situation, health and mobility, future plans and goals, lifestyle, and personal preferences.

Renting can be a better financial decision than owning in retirement if you have limited financial resources, need to downsize, or prefer not to deal with home maintenance and repairs.

Owning a home in retirement can provide long-term investment opportunities, potential for equity and return on investment, control over living space, and personalization options.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.