An Education IRA, also known as a Coverdell Education Savings Account (ESA), is a type of tax-advantaged savings account in the United States designed to help families save for future educational expenses. The purpose of an Education IRA is to encourage individuals to save for qualified education expenses, including tuition, fees, books, supplies, and certain qualified expenses for primary, secondary, and higher education. Contributions made to an Education IRA are not tax-deductible, but the account grows tax-free, and withdrawals used for qualified education expenses are also tax-free. The Education IRA offers individuals the opportunity to save and invest in educational costs in a way that provides potential tax advantages and financial flexibility, helping to alleviate the financial burden associated with education and promoting educational opportunities for beneficiaries. To establish an Education IRA, the designated beneficiary must be under the age of 18 or a special needs beneficiary. Contributions can be made by individuals, corporations, or other entities, as long as their Modified Adjusted Gross Income (MAGI) does not exceed certain limits set by the IRS. Opening an Education IRA involves the following steps: 1. Select a financial institution or brokerage firm that offers Coverdell ESAs. 2. Complete the necessary application forms and provide the required documentation. 3. Designate a beneficiary and select an account custodian (if not the account holder). 4. Fund the account with an initial contribution. 5. The entire process can take a few days to several weeks, depending on the chosen financial institution and required documentation. The initial contribution to an Education IRA can be any amount up to the annual limit, which is $2,000 per beneficiary. Additional contributions can be made until the beneficiary turns 18. The account must be fully withdrawn or transferred to another eligible beneficiary by the time the original beneficiary turns 30. The maximum annual contribution to an Education IRA is $2,000 per beneficiary. Contributions can be made until the beneficiary turns 18, except for special needs beneficiaries, who have no age limit. The deadline for contributions is generally April 15th of the following tax year. The ability to contribute to an Education IRA is subject to income limitations. For single filers, the contribution limit phases out with a MAGI above $153,000 in 2026. For joint filers, the phase-out range is above $242,000. Account holders with income above these limits are not eligible to make contributions. Contributions to an Education IRA are not tax-deductible. However, the earnings within the account grow tax-free, and distributions for qualified education expenses are not subject to federal income tax. Additionally, some states offer tax benefits for Education IRA contributions. Qualified education expenses for an Education IRA include tuition, fees, books, supplies, equipment, and special needs services required for enrollment or attendance at an eligible educational institution. Room and board costs may also qualify if the beneficiary is enrolled at least half-time. If a distribution from an Education IRA is used for non-qualified expenses, the earnings portion of the distribution is subject to federal income tax and a 10% penalty. However, certain exceptions to the penalty exist, such as the beneficiary receiving a scholarship, attending a U.S. military academy, or becoming disabled or deceased. Assets held in an Education IRA are considered parental assets when calculating the Expected Family Contribution (EFC) for federal financial aid purposes. As a result, the impact on financial aid eligibility is generally minimal compared to other types of assets. While both Education IRAs and 529 Plans offer tax-advantaged savings for education expenses, there are notable differences. The most significant difference is that 529 Plans have much higher contribution limits and are not subject to income restrictions. Also, 529 plans can only be used for post-secondary education expenses, while Education IRAs can be used for both elementary, secondary, and post-secondary education expenses. Unlike Education IRAs or 529 Plans, Uniform Gift to Minors Act (UGMA) and Uniform Transfers to Minors Act (UTMA) accounts are not specifically designed for education savings. While the funds can be used for education expenses, they can also be used for any purpose that benefits the child. However, the assets in UGMA/UTMA accounts are considered the child's assets and can negatively impact financial aid eligibility. Roth IRAs, while primarily intended for retirement savings, can also be used for education expenses. The contributions (but not earnings) can be withdrawn tax and penalty-free for any purpose. However, Education IRAs offer tax-free withdrawal of contributions and earnings for qualified education expenses. An Education IRA can be an integral part of a comprehensive education savings strategy. While its contribution limits are relatively low, its tax advantages and flexibility in eligible expenses make it a valuable complement to other savings vehicles like 529 plans or regular savings accounts. When considering who should contribute to an Education IRA, remember that contributions from a grandparent could potentially impact the beneficiary's eligibility for need-based financial aid. This is because assets held in an account owned by anyone other than the student or their parents are assessed at a higher rate in the federal financial aid formula. Education IRAs can also play a role in estate planning. Contributions to an Education IRA are considered completed gifts and can help reduce the account holder's taxable estate. Furthermore, changing beneficiaries allows the account holder to retain some control over the assets even after they have left their estate. The Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 introduced significant changes to many retirement and education savings accounts, including the Education IRA. One of the key changes is the elimination of the age limit for contributions, allowing contributions to be made beyond the beneficiary's 18th birthday for as long as the account exists. Over the years, there have been several legislative changes impacting the rules and benefits of Education IRAs. Notably, the Economic Growth and Tax Relief Reconciliation Act of 2001 expanded the definition of qualified expenses to include elementary and secondary school costs, effectively increasing the versatility of Education IRAs. An Education IRA, or Coverdell Education Savings Account (ESA), is a significant resource for families aiming to secure their children's educational future. This tax-advantaged account promotes the accumulation of funds for primary and higher education expenses, offering considerable financial benefits. To establish an Education IRA, the beneficiary must be either under 18 or a special needs beneficiary. The process includes selecting a financial institution or brokerage firm, filling out necessary forms, designating a beneficiary, and making an initial contribution. The annual contribution limit is $2,000 per beneficiary, with certain income restrictions. Despite its complexities, the Education IRA serves as a valuable financial tool in preparing for the future educational needs of a child, underlining the necessity of thoughtful planning and informed decision-making in establishing such an account.Definition and Purpose of Education IRA

Establishing an Education IRA

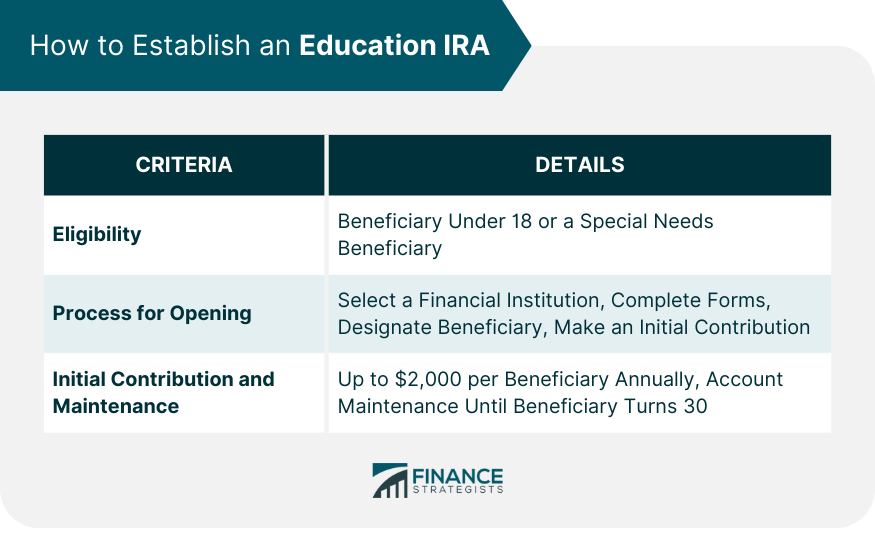

Eligibility Requirements

Process and Timeline for Opening

Initial Contribution and Maintenance

Financial Aspects of Education IRA

Contribution Limits and Deadlines

Impact of Income Level on Contributions

Tax Implications and Benefits

Distribution From Education IRA

Qualified Education Expenses

Non-qualified Distribution

Impact on Financial Aid Eligibility

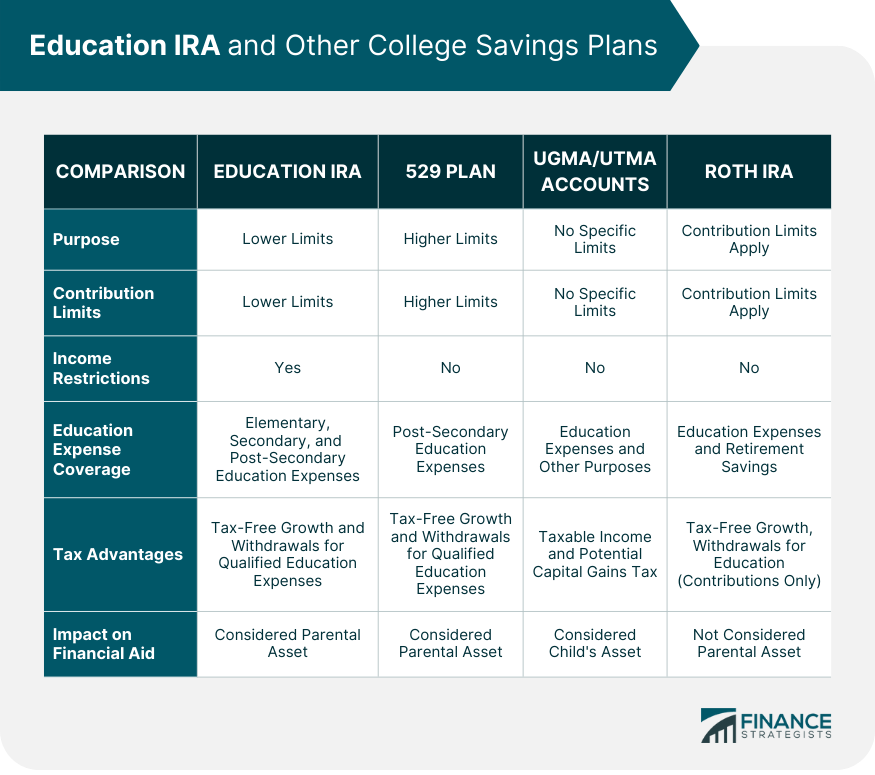

Comparing Education IRA With Other College Savings Plans

Education IRA vs 529 Plan

Education IRA vs UGMA/UTMA Accounts

Education IRA vs Roth IRA

Role of Education IRA in Financial Planning

Incorporating Education IRA into Broader Education Savings Strategy

Considerations for Parents vs Grandparents Contributions

Role in Estate Planning

Changes in Education IRA Regulations

Impact of the SECURE Act on Education IRA

Other Significant Legislative Changes

Final Thoughts

Education IRA FAQs

An Education IRA, also known as a Coverdell Education Savings Account (ESA), is a tax-advantaged investment account designed to help families save for future education expenses. Funds from an Education IRA can be used for a variety of qualified education expenses for elementary, secondary, and post-secondary education.

An Education IRA is similar to a 529 Plan, and Roth IRA in that all offer tax advantages for education savings. However, an Education IRA can be used for both elementary and secondary education expenses, unlike a 529 Plan. Compared to a Roth IRA, an Education IRA allows for tax-free withdrawal of both contributions and earnings for qualified education expenses.

The maximum annual contribution to an Education IRA is $2,000 per beneficiary. The ability to contribute is subject to income limitations - the contribution limit begins to phase out for single filers with a MAGI between $95,000 and $110,000 and for joint filers between $190,000 and $220,000. Account holders with income above these limits are not eligible to make contributions.

The SECURE Act of 2019 introduced significant changes to the Education IRA, including the elimination of the age limit for contributions. This allows contributions to be made beyond the beneficiary's 18th birthday for as long as the account exists.

Successful uses of an Education IRA often involve consistent contributions over a long period, allowing the savings to grow and cover significant education expenses. However, challenges can arise, such as when a beneficiary receives a significant scholarship, potentially leading to penalties for non-qualified distributions. These challenges can often be mitigated with careful planning and by considering the flexibility offered by the Education IRA, such as the ability to change beneficiaries.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.