Non-qualified stock options (NQSOs) are a form of equity compensation granted by companies to their employees, directors, and sometimes contractors or consultants. NQSOs give the option holder the right to purchase company stock at a predetermined price, known as the strike price, after a specified vesting period. Their tax treatment and eligibility rules differ from incentive stock options (ISOs). While both NQSOs and ISOs are used to compensate employees with company stock, there are key differences in their tax implications and eligibility requirements. ISOs receive more favorable tax treatment but have stricter rules regarding who can receive them and how they can be exercised. NQSOs, on the other hand, have fewer restrictions but less favorable tax treatment for the option holder. By aligning the interests of employees with those of the company, NQSOs can help incentivize hard work, loyalty, and long-term commitment to the organization. NQSOs are commonly granted to employees as part of their overall compensation package. They may be awarded based on performance, position, or tenure within the company and can help attract and retain top talent. Board members may also receive NQSOs as a form of compensation for their service to the company. This type of equity award can help align the interests of directors with those of the company's shareholders. In some cases, companies may grant NQSOs to contractors or consultants as a form of payment for their services. This arrangement can be beneficial for both parties, as it allows the company to conserve cash while providing the contractor or consultant with a potentially valuable form of compensation. Granting NQSOs typically requires approval from the company's board of directors. The board will determine the terms of the options, such as the number of shares, strike price, and vesting schedule. Once the board approves the NQSO grant, the company and the option recipient draft and execute option agreements. These agreements outline the specific terms and conditions of the options, including any restrictions on transfer or exercise. The strike price is the predetermined price at which an option holder can purchase company stock when exercising their NQSOs. It is typically set at the stock's fair market value on the date of the grant. The vesting schedule determines when the option holder becomes eligible to exercise their NQSOs. Vesting may occur gradually over time or be subject to specific performance or employment milestones. NQSOs have an expiration date, after which the options can no longer be exercised. This date is typically set several years in the future, providing the option holder with ample time to decide when to exercise their options. A cash exercise involves the option holder paying the strike price in cash to purchase the underlying shares of company stock. The holder then owns the shares outright and can choose to hold or sell them as desired. A cashless exercise allows option holders to exercise their NQSOs without the need for upfront cash. The holder simultaneously exercises the options and sells the acquired shares, using the sale proceeds to cover the strike price cost and any taxes owed. In a stock swap, the option holder exchanges shares of company stock they already own to cover the cost of the strike price. This method allows the holder to exercise their NQSOs without paying cash or selling other assets. Option holders must meet the vesting requirements outlined in their option agreement before exercising their NQSOs. These requirements may include a vesting schedule based on time, performance, or employment milestones. Option holders may be restricted from exercising their NQSOs during company blackout periods, which are times when trading in company stock is prohibited due to insider information or other regulatory concerns. Option holders should consider market conditions when deciding when to exercise their NQSOs, as the potential financial gain is directly tied to the company's stock price. Exercising options when the stock price is high can result in greater profits. There are no taxes due upon the grant or vesting of NQSOs, making them a tax-efficient form of equity compensation at these stages. When NQSOs are exercised, the difference between the strike price and the stock's fair market value (the spread) is considered ordinary income and subject to federal, state, and local income taxes. In addition to income taxes, the spread may be subject to withholding and employment taxes, such as Social Security, Medicare, and unemployment taxes, depending on the option holder's employment status. When the stock acquired through the NQSO exercise is sold, any gain or loss relative to the stock's fair market value at the time of exercise is subject to capital gains tax. This tax rate depends on the holding period and the option holder's income level. To qualify for the lower long-term capital gains tax rate, the option holder must hold the acquired stock for at least one year after the exercise and two years after the grant date. Otherwise, the gain will be subject to the higher short-term capital gains tax rate. Option holders can employ various tax planning strategies to minimize their tax liabilities when exercising NQSOs, such as exercising options in a lower-income year, spreading exercises over multiple years, or donating appreciated stock to charity. NQSOs offer companies greater flexibility in granting options, as they can be awarded to employees, directors, contractors, and consultants without the strict eligibility requirements associated with ISOs. NQSOs provide option holders with the potential for significant financial gain if the company's stock price increases, aligning their interests with those of the company and its shareholders. By offering employees the opportunity to share in the company's success, NQSOs can help retain top talent and motivate employees to work toward the company's goals. The tax implications of NQSOs can result in large tax liabilities for option holders, particularly if they exercise a large number of options or if the company's stock price increases significantly. The issuance of NQSOs can lead to the dilution of shareholder value, as the creation of new shares can reduce the value of existing shares and earnings per share. The value of NQSOs is directly tied to the company's stock price, meaning option holders face the risk of stock price decline, which could render their options worthless or result in a loss upon exercise and sale. The Securities Act of 1933 regulates the offer and sale of securities, including NQSOs. Companies must comply with registration and disclosure requirements unless an exemption applies. The Securities Exchange Act of 1934 governs ongoing reporting requirements for companies with publicly traded securities, including those that grant NQSOs. This legislation requires periodic disclosure of financial and other material information. Under FASB rules, companies must recognize an expense for NQSOs over the vesting period based on the fair value of the options on the grant date. Companies must report NQSO-related expenses in their financial statements, which can impact their reported earnings and financial ratios. NQSOs play a significant role in modern compensation strategies, providing a valuable form of equity-based compensation for employees, directors, and contractors. By offering the potential for financial gain and aligning interests, NQSOs can help companies attract and retain top talent. While NQSOs offer numerous advantages, they also come with potential drawbacks, such as tax liabilities and stock price risks. Companies and option holders must carefully weigh these factors when designing and managing NQSO programs. As the business landscape continues to evolve, it is likely that companies will continue to seek innovative ways to compensate employees, including through equity-based compensation like NQSOs. An experienced advisor can help navigate the various considerations and develop strategies to maximize the potential benefits of NQSOs while minimizing risks and tax liabilities.What Are Non-Qualified Stock Options (NQSOs)?

Granting Non-Qualified Stock Options

Eligible Recipients

Employees

Directors

Contractors and Consultants

Grant Process

Board of Directors Approval

Option Agreements

Key Terms in NQSOs

Strike Price

Vesting Schedule

Expiration Date

Exercising Non-Qualified Stock Options

Exercise Methods

Cash Exercise

Cashless Exercise

Stock Swap

Exercise Timing Considerations

Vesting Requirements

Company Blackout Periods

Market Conditions

Tax Implications of Non-Qualified Stock Options

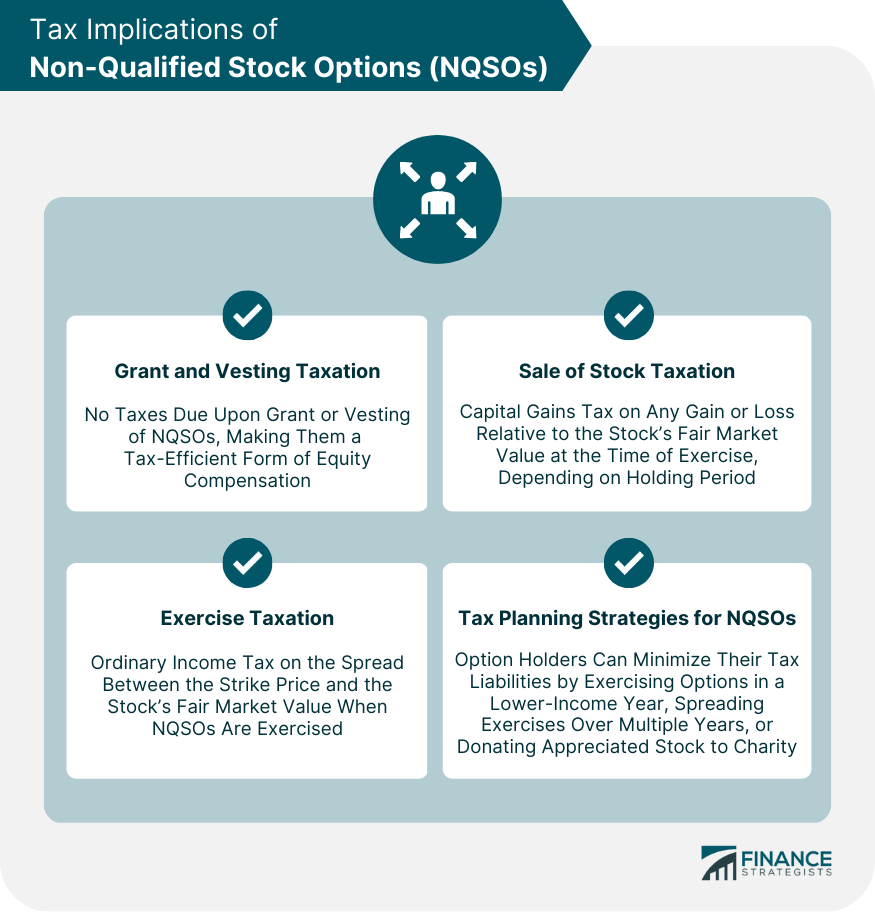

Grant and Vesting Taxation

No Taxes Upon Grant or Vesting

Exercise Taxation

Ordinary Income Tax on the Spread

Withholding and Employment Taxes

Sale of Stock Taxation

Capital Gains Tax

Holding Period Considerations

Tax Planning Strategies for NQSOs

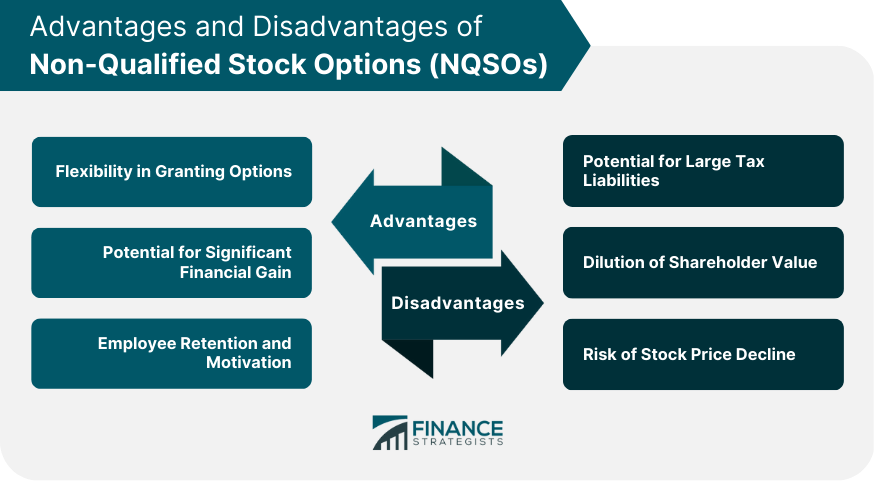

Advantages of Non-Qualified Stock Options (NQSOs)

Flexibility in Granting Options

Potential for Significant Financial Gain

Employee Retention and Motivation

Disadvantages of Non-Qualified Stock Options (NQSOs)

Potential for Large Tax Liabilities

Dilution of Shareholder Value

Risk of Stock Price Decline

Regulatory and Legal Considerations of Non-Qualified Stock Options (NQSOs)

Securities Laws and Regulations

Securities Act of 1933

Securities Exchange Act of 1934

Accounting Implications

Financial Accounting Standards Board (FASB) Rules

Expense Recognition and Reporting

Final Thoughts

Non-Qualified Stock Options (NQSOs) FAQs

Non-Qualified Stock Options (NQSOs) are a type of stock option that allows employees, directors, contractors, and consultants to purchase company shares at a predetermined price. NQSOs differ from Incentive Stock Options (ISOs) in that they do not receive the same preferential tax treatment as ISOs, and they can be granted to a broader range of recipients.

When exercising Non-Qualified Stock Options (NQSOs), the difference between the stock's fair market value and the option's exercise price (the "spread") is treated as ordinary income and subject to income tax and withholding. Upon selling the shares, any further gain or loss is subject to capital gains tax, depending on the holding period.

Advantages of Non-Qualified Stock Options (NQSOs) include flexibility in granting options, potential for significant financial gain, and serving as a tool for employee retention and motivation. Disadvantages include the potential for large tax liabilities, dilution of shareholder value, and risk of stock price decline.

Non-Qualified Stock Options (NQSOs) are subject to securities laws and regulations, including the Securities Act of 1933 and the Securities Exchange Act of 1934. Companies must also adhere to Financial Accounting Standards Board (FASB) rules, recognizing and reporting option-related expenses in their financial statements.

To effectively manage Non-Qualified Stock Options (NQSOs), employees should familiarize themselves with their options' specific terms and conditions, consider the tax implications, and evaluate the best time to exercise their options based on their individual financial situation. It is highly recommended to consult with a financial advisor to develop a personalized strategy for managing NQSOs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.