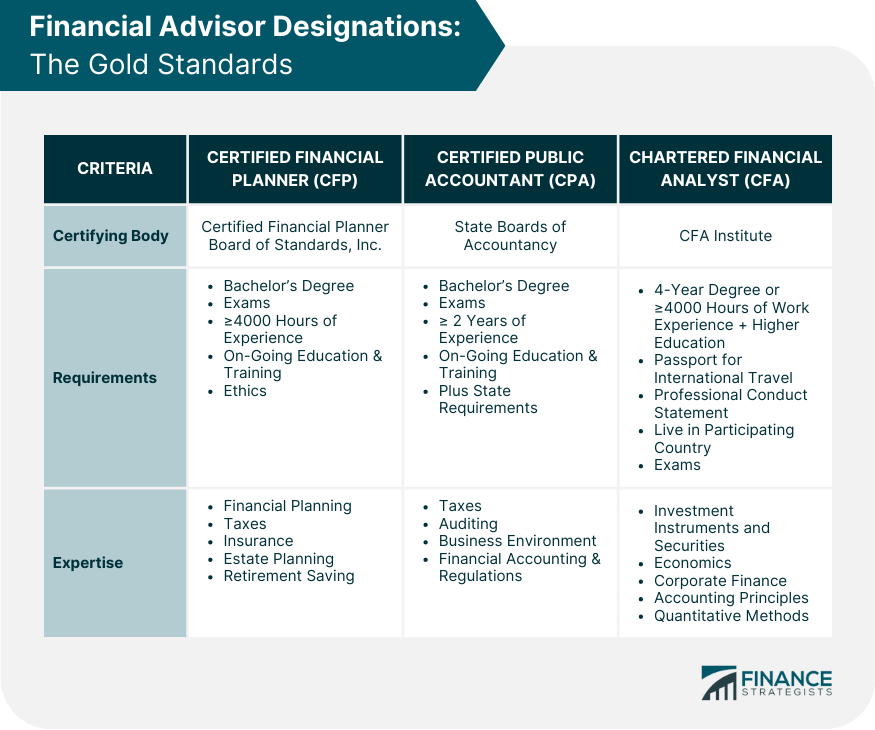

Working with a financial advisor can give you peace of mind, especially regarding long-term financial planning and investing. But not all advisors are created equal: some specialize in particular financial products, while others are experts in specific areas of financial planning. There are staid, experienced types with decades in the business behind them. Others are ambitious, young professionals looking to make a name for themselves. Nonetheless, all competent financial advisors share professional designations, licenses, and qualifications. Do your due diligence and research these different qualifications before choosing a financial advisor. While there are over 160 financial credentials and professional designations available today, the following are the three most widely recognized designations: The CFP is one of the most common professional designations for financial planners in the U.S. It is awarded by the Certified Financial Planner Board of Standards, Inc., a nonprofit organization that promotes competency and ethics in the financial planning industry. Applicants must undergo a rigorous process before certification involving education, exams, experience, and ethics. The CFP designation requires applicants to have a bachelor's degree or higher. They must then complete a significant amount of coursework and pass two exams encompassing financial planning, professional conduct, and regulations. Additionally, applicants must prove that they have accrued at least 4000 hours of apprenticeship under a CFP professional or 6000 hours of direct or indirect financial planning experience. CFPs are also required to pursue ongoing education and training. A CFP designation ensures that an advisor is an expert and updated on the current trends in the financial planning field. The CFP Board also requires holders to abide by fiduciary standards. The CPA designation is awarded by the different State Boards of Accountancy for practice in their particular jurisdictions. Additionally, the American Institute of Certified Public Accountants (AICPA) is the largest body of CPAs in the U.S. While most CPAs focus on tax laws and regulations, they can provide general financial support like record keeping, reporting, auditing, and forecasting for individuals or businesses. The standardized CPA exam covers four areas – auditing and attestation, business environment and concepts, financial accounting and reporting, and regulation. To be able to take the exam, a candidate must have a bachelor’s degree in a finance-related field. It is also generally required to prove at least two years of work experience or training. Other requirements vary by state. Furthermore, while CPAs are not required to be fiduciaries, AICPA’s code of conduct highlights objectivity, integrity, and freedom from conflicts of interest. Individuals usually get their CPA license to render tax services, which also helps when giving financial advice. This designation becomes relevant when dealing with any financial decisions that may trigger a tax event, such as the sale of appreciated stock or bequeathing gifts. The designation of Chartered Financial Analyst is granted by the CFA Institute and is an internationally recognized certification. The CFA Program comprises three levels, each requiring exams that must be taken and passed within 18 months. Candidates must understand investment instruments, economics, corporate finance, accounting principles, quantitative methods, and how securities work. They must have completed a four-year bachelor’s degree or be within 11 months of graduating. Undergraduates may also apply if they have a combination of at least 4000 hours of professional working experience and higher education that highlights leadership, business communications, problem-solving, critical thinking, and adaptability skills. They must live in a CFA Institute participating country, take an English exam, complete a professional conduct statement, and hold a valid passport for international travel. The CFA Institute also expects fiduciary commitments from designation holders. Often CFAs are not client-facing and instead support a financial advisor by determining which assets to purchase and sell from a client’s portfolio. Nonetheless, the wide range of expertise required to achieve this designation also means that CFAs can make great financial advisors. A financial advisor's resumé may additionally include any of the following positions in addition to the ones mentioned above: Enrolled Agents are licensed by the Internal Revenue Service (IRS) to represent taxpayers before the agency. They must either pass a three-part exam that tests their knowledge of taxation and financial matters or have experience as a former IRS employee. EAs must also take 6 hours of ethics training and 72 hours of continuing education every 3 years. The American College of Financial Services provides the CLU designation. CLUs specialize in life insurance. They are experts on the legal aspects of insurance, risk management, estate and retirement planning, taxes, and annuities. This designation requires 3 years of business experience, which can be full-time or a combination of higher education and accrued part-time hours. The Chartered Financial Consultant designation is also from the American College of Financial Services. It requires a high school diploma and 3 years of full-time business experience. Holders specialize in financial, retirement, and estate planning, risk management, income tax strategies, and insurance. The Investment and Wealth Institute awards this designation. It requires a bachelor's degree in accounting, finance, or other related disciplines. CIMAs are skilled in business performance, investment decisions, analytics, portfolio and financial management, and asset valuation. It is offered by the International Foundation of Employee Benefit Plans (IFEBP). CEBS holders help plan and negotiate employee-benefit packages for companies. They specialize in compensation structures, health and disability benefits, and retirement planning. There are no prerequisites to the CEBS. However, holders are required to complete 30 hours of continuing education and training every 2 years. The Institutes administer the CPCU designation. CPCUs are property and casualty (P&C) insurance experts, focusing on risk management, insurance operations and law, and other financial services. Holders can specialize either in commercial or personal P&C insurance. CPCU candidates are required to have 24 months of insurance-related work experience, gained within 5 years before applying for the designation. Alongside professional designations, a financial advisor will generally also hold several licenses. These differ based on the investment products they allow an advisor to sell. All licensure exams are administered by the Financial Industry Regulatory Authority (FINRA). It enables advisors to sell what are called “packaged securities.” These include mutual funds or variable annuities with low investment risk. A Series 6 license does not allow someone to sell individual stocks or bonds, which are considered riskier investments. It allows its holders to sell almost any type of security, including individual stocks, bonds, options, and futures, making it far more comprehensive than the Series 6 license. The only financial products not covered by a Series 7 are commodities and life insurance, which require their own license. A financial advisor must also take the Securities Industry Essentials (SIE) exam as a co-requisite to Series 6 or 7. SIE is considered a co-requisite and can be taken within four years before or after passing the Series 6 or 7 exams. It was introduced because many of the FINRA exams were redundant in the knowledge they tested. The SIE exam measures the foundational material so that other exams can test knowledge specific to the license. It is also called the National Commodities Futures Exam and allows its holders to trade commodities futures. It covers topics such as leverage, derivatives, hedging strategies, and associated laws and regulations. The Series 3 exam does not require applicants to have passed the SIE before sitting for it. The Series 63 exam is also known as the Uniform Securities State Law Examination. It tests knowledge of state-specific regulations on securities and provides a license to operate almost anywhere in the United States. FINRA administers it for the North American Securities Administrators Association (NASAA). The SIE exam is not a prerequisite. The Series 65 exam is for investment advisors. It tests knowledge of the legal and regulatory requirements for managing client investments. A successful applicant can work independently or as an investment advisor representative in a brokerage. Series 65 is also known as the Uniform Investment Adviser Law exam. It is also a NASAA qualification administered by FINRA and does not require applicants to take the SIE. Understanding the different designations and licenses equips you with knowledge of financial advisor specializations. The next step is checking for the specific qualifications of potential advisors. You may use the following tools: The BrokerCheck tool tool is FINRA's public information service for researching brokers, advisors, and their firms. You may search using either a person's name or firm registration number. BrokerCheck shows employment history, licensing information, and designations. It can also be used to check if regulators have ever censured a financial professional in the past. The IAPD tool is maintained by the Securities and Exchange Commission (SEC). It contains background information about registered individual financial advisors and firms. IAPD is a convenient way of reviewing a potential advisor's credentials. It also provides information on disciplinary actions, if any. The SALI tool primarily checks whether a financial advisor has been named in administrative proceedings or court actions. It includes judgments, settlement agreements, and disciplinary action against the advisor. It adds another layer of scrutiny beyond designations and licenses. The designation and license you should look for in a financial advisor will depend on your goals and the specific needs you want to be addressed. If you are looking for advice on a particular aspect of your finances – say tax or life insurance– it is worth looking to the professional bodies which oversee that area. For life insurance, you should look for a financial advisor who has earned a CLU. You may work with a CPA or an EA for taxes. Most people looking for a financial advisor will need general advice across various topics. For that, you should look for an advisor with a CFP designation. An advisor with this accreditation is likely knowledgeable and experienced enough to give you good advice. If you are looking for more specific expertise, any experienced CFP, CPA, or CFA can recommend fellow professionals who specialize in your desired area of financial planning. Remember to use BrokerCheck, IAPD, and SALI to ensure the advisor is qualified and has no disciplinary actions against them. Finally, make sure that the values of your financial advisor align with yours.The Gold Standards

Certified Financial Planner (CFP)

Certified Public Accountant (CPA)

Chartered Financial Analyst (CFA)

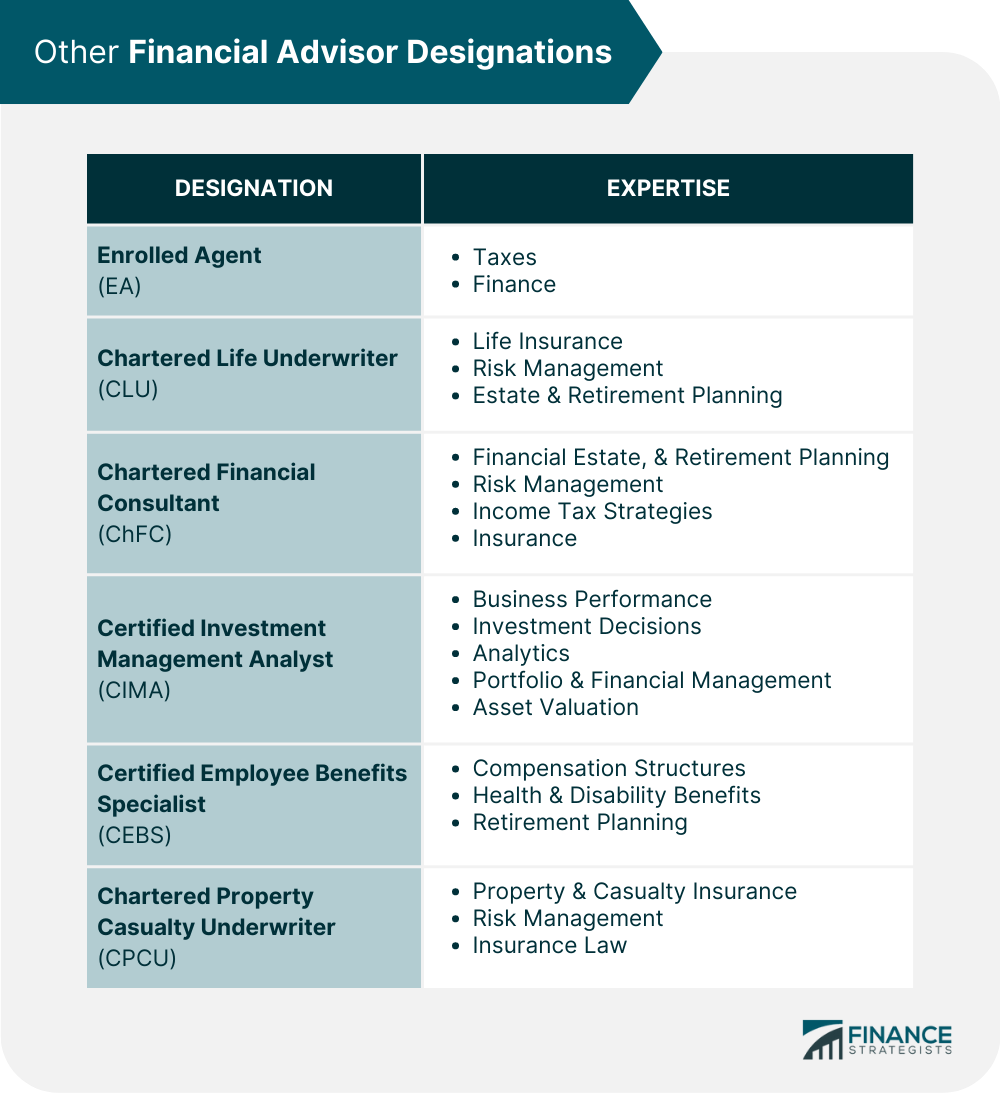

Other Financial Advisor Designations

Enrolled Agent (EA)

Chartered Life Underwriter (CLU)

Chartered Financial Consultant (ChFC)

Certified Investment Management Analyst (CIMA)

Certified Employee Benefits Specialist (CEBS)

Chartered Property Casualty Underwriter (CPCU)

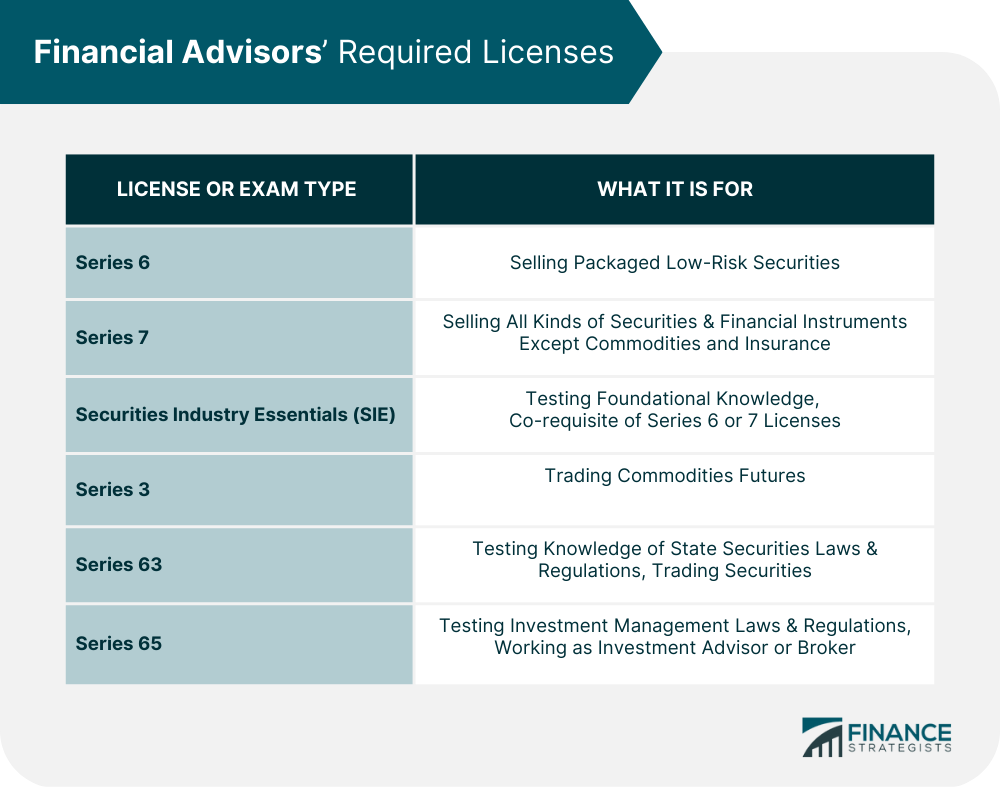

What Licenses Do Financial Advisors Need to Have?

Series 6 License

Series 7 License

Securities Industry Essentials (SIE)

Series 3 License

Series 63 License

Series 65 License

How to Check Your Financial Advisor

FINRA BrokerCheck

Investment Adviser Public Disclosure (IAPD)

SEC Action Lookup - Individuals (SALI)

The Bottom Line

Financial Advisor Designations That Matter FAQs

The easiest financial designation depends on the individual’s background and experience level. The Chartered Financial Consultant (ChFC) may be most accessible because it only requires a high school diploma. Certifications such as the Chartered Financial Analyst (CFA) or Certified Financial Planner (CFP) require a higher level of education.

It is the Certified Financial Planner (CFP) certification, which the Certified Financial Planner Board of Standards, Inc issues. CFPs are held to high ethical standards and must commit to pursuing continuing education requirements to maintain their licensure.

It is the Chartered Financial Analyst (CFA) designation. It is a graduate-level program for investment professionals offered by the CFA Institute. To earn the title, candidates must pass three levels and have at least four years of professional experience in a related field. It is internationally recognized, and holders receive credentials demonstrating their expertise in financial analysis and investment management.

Certified Financial Analyst (CFA) and Certified Financial Planner (CFP) holders offer valuable services. The best choice for you will depend on your individual needs. CFAs can provide expertise in portfolio management and investment analysis. CFPs are trained to design and implement comprehensive financial plans that integrate various aspects of a client’s life, such as budgeting, investments, retirement planning, insurance needs, estate planning, and tax strategies.

CFP may be easier to obtain than CPA. It is because the CFP exam is more focused on investment-related topics and does not require candidates to understand accounting processes deeply. Additionally, there are no degree prerequisites for taking the CFP exam, whereas a college degree in Accounting or Finance is usually needed for the CPA designation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.