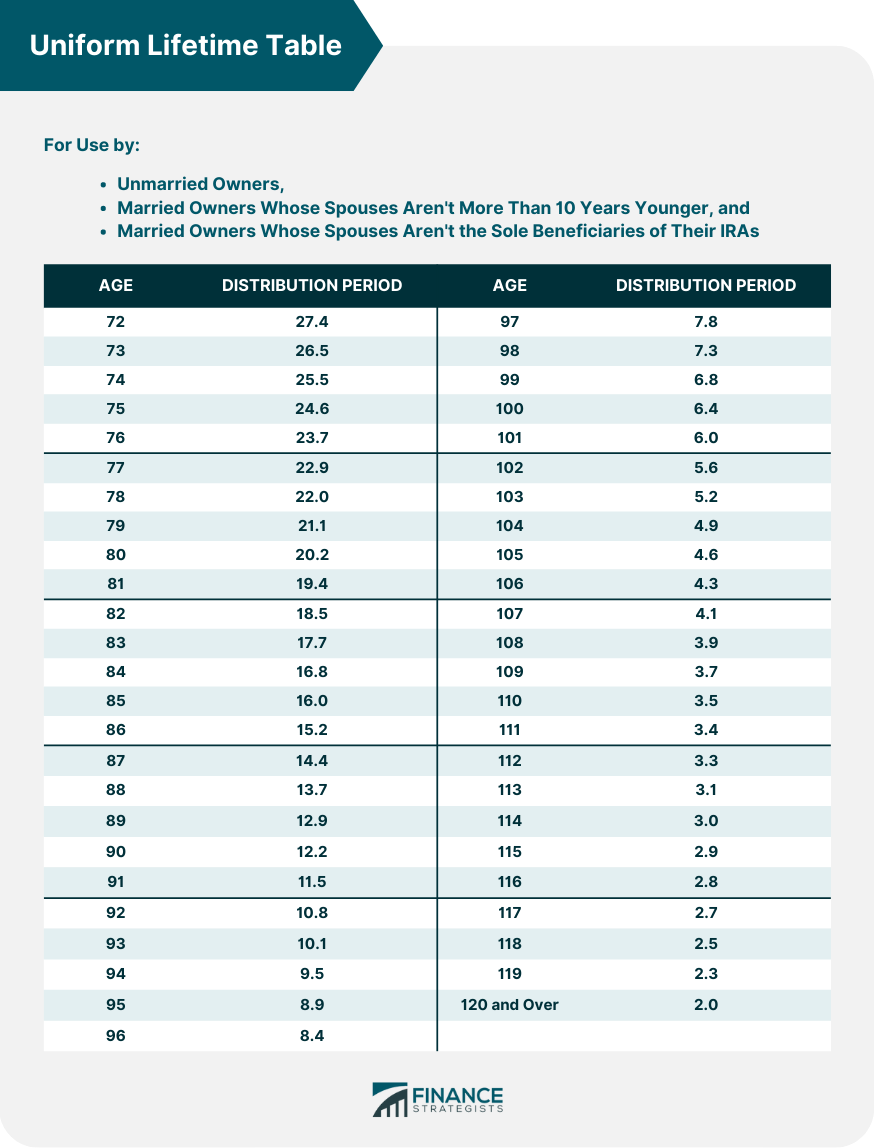

The Uniform Lifetime Table is a chart provided by the Internal Revenue Service (IRS) that outlines the life expectancy factors used to calculate Required Minimum Distributions (RMDs) for retirement account holders. This table serves as a tool for determining the minimum amount an individual must withdraw from their tax-deferred retirement accounts each year, starting at age 73, to avoid tax penalties. The Uniform Lifetime Table plays a crucial role in calculating RMDs, which are mandatory withdrawals from retirement accounts to ensure that individuals do not defer taxes on their savings indefinitely. The Uniform Lifetime Table is an important tool for retirees and their financial advisors to calculate Required Minimum Distributions from their retirement accounts, such as Individual Retirement Accounts (IRAs) and 401(k)s. RMDs are the minimum amount that must be withdrawn from these accounts annually, starting at age 73, to avoid tax penalties. The structure of the Uniform Lifetime Table includes age-based distribution periods and corresponding factors for calculating RMDs. The age-based distribution periods range from 70 to 115 and over, with each age associated with a specific distribution period that represents the life expectancy for individuals at that age. For each age, a factor is provided, which is used in conjunction with the account balance to determine the RMD for that year. The factors are designed to gradually increase as the account owner ages, reflecting the decreasing life expectancy at older ages. It is essential to use the table accurately to comply with IRS regulations and avoid tax penalties. Failing to take the correct RMD can result in a penalty of up to 50% of the amount that should have been withdrawn. Using the table correctly can also help preserve retirement savings by ensuring that withdrawals are calculated appropriately to last throughout retirement. The IRS may periodically update the Uniform Lifetime Table to reflect changes in life expectancy data. It is important for retirees and their financial advisors to stay current with the latest version of the table to accurately calculate RMDs. The IRS also provides other life expectancy tables, such as the Joint Life and Last Survivor Expectancy Table, for certain circumstances, such as when the account owner has a spouse who is more than ten years younger. The Uniform Lifetime Table provides age-based distribution periods that correspond to the life expectancy for individuals at each age. To use the table effectively, individuals must locate their age and identify the corresponding distribution period. Locate the Account Holder's Age: To determine the appropriate distribution period for calculating the RMD, individuals should find the account holder's age in the table. The table lists ages from 70 to 115 and over. Identify Corresponding Distribution Period: The corresponding distribution period can now be identified, which will be used in the RMD calculation. The table gives a factor for each age used in conjunction with the account balance to identify the RMD for that year. To calculate the RMD using the Uniform Lifetime Table; individuals must first obtain the account balance and then divide it by the distribution period identified in the table. Obtaining the Account Balance: The account balance used in the RMD calculation should be determined as of December 31st of the previous year. Dividing the Account Balance by the Distribution Period: Individuals should divide the account balance by the distribution period identified in the table for their age. The resulting quotient is the amount that must be withdrawn as the RMD for the year. In certain situations, adjustments to the RMD calculation may be necessary. For example, spousal or non-spousal beneficiaries may have different life expectancies that affect their RMD calculations. Spousal Beneficiaries: If the account holder's spouse is the sole beneficiary and is more than ten years younger, a different life expectancy table, the Joint Life and Last Survivor Expectancy Table should be used. Non-Spousal Beneficiaries: Non-spousal beneficiaries, such as children or other individuals, may need to use the Single Life Expectancy Table to determine their RMDs from an inherited account. Multiple Beneficiaries: When an account holder has multiple beneficiaries, each beneficiary's portion of the RMD may be calculated using their respective life expectancies. This can result in varying RMD amounts for each beneficiary. Failure to withdraw the appropriate RMD as calculated using the Uniform Lifetime Table may result in a 50% tax penalty on the amount that should have been withdrawn but was not. Timely withdrawals, as guided by the Uniform Lifetime Table, are essential to avoid tax penalties and ensure that retirement savings are accessed as intended. Not adhering to the Uniform Lifetime Table's guidelines can negatively affect retirement savings by incurring tax penalties, reducing the overall value of the retirement account, and limiting financial planning opportunities. Using the Uniform Lifetime Table in conjunction with other tax strategies, such as prioritizing withdrawals from taxable accounts first, can help minimize the overall tax burden on retirement savings. Account holders can satisfy their RMDs while also benefiting charities by making Qualified Charitable Distributions, which are tax-free donations made directly from an IRA to a qualified charitable organization. Converting traditional IRA funds to a Roth IRA can help account holders manage their RMDs, as Roth IRAs do not have RMD requirements during the owner's lifetime. Individuals can reinvest their RMDs in taxable accounts or other investment vehicles to maintain their retirement savings growth and diversify their investment portfolio. There are some exceptions to using the Uniform Lifetime Table, such as when an account holder's spouse is more than ten years younger and is the sole beneficiary, in which case the Joint Life and Last Survivor Expectancy Table should be used. The Uniform Lifetime Table is used to calculate RMDs for account holders, while the Single Life Expectancy Table is typically used for non-spousal beneficiaries who inherit retirement accounts. If an account holder's spouse is more than ten years younger and is the sole beneficiary, the couple should use the Joint Life and Last Survivor Expectancy Table to determine RMDs, as it provides more favorable distribution periods. The Uniform Lifetime Table is an IRS-provided chart for calculating RMDs from retirement accounts. It determines the minimum amount a person must withdraw annually from their tax-deferred accounts, starting at age 73, to avoid tax penalties. Properly understanding and using the Uniform Lifetime Table is critical to ensuring compliance with IRS regulations, avoiding tax penalties, and optimizing retirement savings. The Uniform Lifetime Table plays a vital role in retirement planning by providing a framework for calculating RMDs and guiding individuals in managing their retirement savings effectively. By following the Uniform Lifetime Table and adhering to RMD requirements, individuals can avoid tax penalties and protect their retirement savings. To make the most of retirement savings and navigate RMD requirements confidently, consider consulting with a professional financial planner or retirement planning expert who can provide personalized guidance and advice.What Is the Uniform Lifetime Table?

Understanding the Uniform Lifetime Table

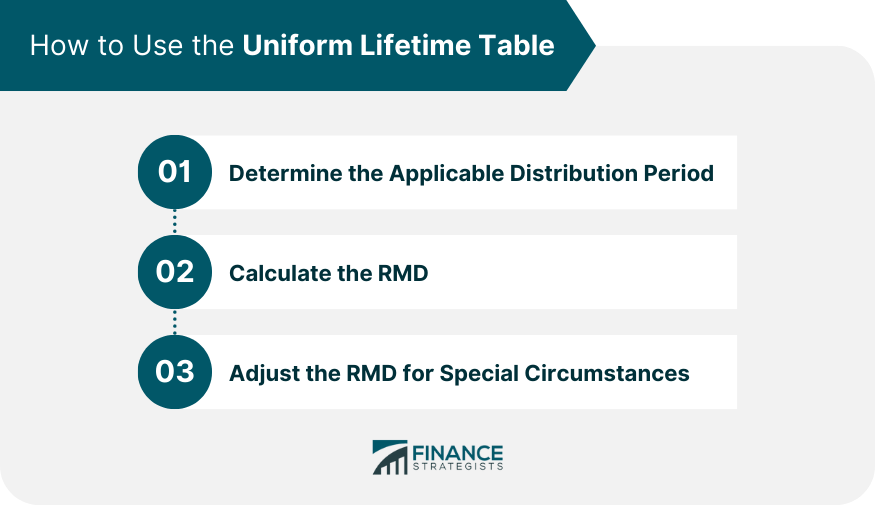

How to Use the Uniform Lifetime Table

Determine the Applicable Distribution Period

Calculate the RMD

Adjust the RMD for Special Circumstances

Implications of Not Following the Uniform Lifetime Table

Tax Penalties for Not Taking the Required RMD

Importance of Timely Withdrawals

Potential Impact on Retirement Savings

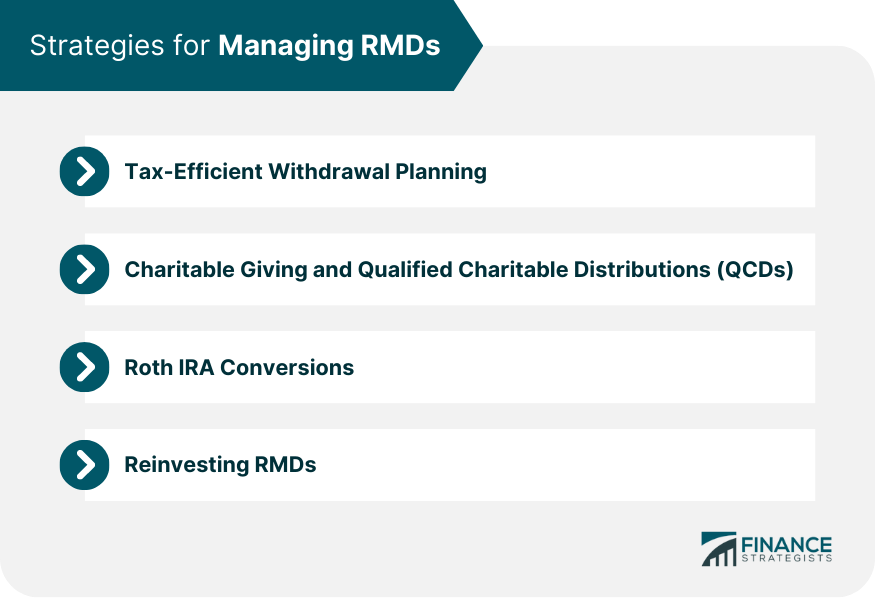

Strategies for Managing RMDs

Tax-Efficient Withdrawal Planning

Charitable Giving and Qualified Charitable Distributions (QCDs)

Roth IRA Conversions

Reinvesting RMDs

Common Inquiries and Concerns

Exceptions to the Uniform Lifetime Table

Comparing the Uniform Lifetime Table and the Single Life Expectancy Table

Adjustments for Account Holders with Significantly Younger Spouses

Final Thoughts

Uniform Lifetime Table FAQs

The Uniform Lifetime Table is used to determine the Required Minimum Distributions (RMDs) that retirement account holders must withdraw from their tax-deferred accounts each year, starting at age 73, to comply with IRS regulations and avoid tax penalties.

The Uniform Lifetime Table provides age-based distribution periods and factors for calculating RMDs, which helps individuals determine the minimum amount they must withdraw from their retirement accounts each year to comply with IRS rules and avoid penalties.

Yes, if an account holder's spouse is more than ten years younger and is the sole beneficiary, the couple should use the Joint Life and Last Survivor Expectancy Table instead of the Uniform Lifetime Table, as it provides more favorable distribution periods.

Failure to comply with the RMD amounts calculated using the Uniform Lifetime Table can result in a 50% tax penalty on the amount that should have been withdrawn but was not, negatively impacting retirement savings and potentially limiting financial planning opportunities.

No, non-spousal beneficiaries who inherit retirement accounts should typically use the Single Life Expectancy Table instead of the Uniform Lifetime Table to determine their RMDs, as it is specifically designed for calculating RMDs for inherited accounts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.