Foreign pensions refer to retirement benefits earned and accumulated outside one's home country. These may include government-sponsored, employer-sponsored, or private pension plans, and are essential to consider for individuals who have worked in multiple countries during their careers. Understanding foreign pensions is crucial for individuals who have accumulated retirement assets in multiple countries, as it enables them to make informed decisions about retirement planning. Proper management of foreign pensions can help ensure financial security, tax compliance, and avoidance of potential penalties. Foreign pensions play a significant role in retirement planning for expatriates, immigrants, and globally mobile professionals. By incorporating foreign pensions into their retirement strategies, individuals can optimize their retirement income, minimize tax liabilities, and ensure a comfortable and secure retirement. Government pensions are retirement benefits provided by the state or government of a foreign country. These usually include social security systems and national pension schemes, which are designed to provide income to retirees based on their years of work and contributions made. Social security systems are public pension programs funded by taxes on employees and employers and often by the government as well. These systems provide retirement, disability, and survivor benefits to eligible individuals, with the goal of reducing poverty and providing a basic level of financial security in old age. National pension schemes are government-sponsored retirement plans, usually mandatory for all workers, with contributions made by employees, employers, and sometimes the government. The benefits are typically based on factors such as the individual's earnings, years of service, and contribution history. Employer-sponsored pensions are retirement plans established and maintained by employers for the benefit of their employees. These plans generally come in two forms: defined benefit plans and defined contribution plans, both of which have different structures and features. Defined benefit plans, also known as traditional pension plans, promise a specific retirement benefit based on a predetermined formula, typically taking into account factors such as salary, years of service, and age. The employer is responsible for managing the plan's investments and ensuring that the promised benefits are available upon retirement. Defined contribution plans, such as 401(k) plans in the United States, require employees and often employers to make regular contributions to an individual account. The retirement benefits are based on the account balance at retirement, which depends on the contributions made and the investment performance of the account. Private pensions are retirement savings vehicles that individuals can establish and manage independently of government or employer-sponsored plans. They generally include individual retirement accounts and annuities, offering greater flexibility and control over retirement assets. Individual retirement accounts (IRAs) are tax-advantaged savings accounts that individuals can set up to save for retirement. Contributions to IRAs may be tax-deductible, tax-deferred, or tax-free, depending on the type of account and the individual's circumstances. Annuities are long-term financial contracts, typically issued by insurance companies, that provide a stream of income in exchange for an initial lump sum payment or a series of premium payments. Annuities can be structured to provide income for a fixed period or for the lifetime of the annuitant, offering a guaranteed income stream in retirement. Tax treaties and agreements are international agreements between countries to prevent double taxation, promote cooperation, and simplify tax compliance for taxpayers with cross-border income. The country where a foreign pension originates may impose taxes on the pension payments, depending on the local tax laws and any applicable tax treaties. The tax treatment of foreign pensions varies greatly between countries, with some imposing taxes on pension contributions, investment returns, or pension benefits, while others may offer tax exemptions or favorable tax treatment. The country of residence for a foreign pension recipient may also impose taxes on the pension income, depending on the domestic tax laws and any tax treaties in place. Tax residents are generally required to report their worldwide income, including foreign pensions, and may be subject to taxes on that income. However, tax exemptions or credits may be available under certain conditions. Double taxation relief is a mechanism that allows individuals to avoid being taxed twice on the same income, such as foreign pensions, in both the country of origin and the country of residence. Tax treaties often contain provisions for double taxation relief, which may include tax exemptions, tax credits, or reduced tax rates on foreign pension income. Foreign pension recipients are generally required to report their pension income on their annual tax returns, regardless of whether the income is taxable or not. Failure to report foreign pensions may result in penalties, interest, or additional taxes. It is essential for individuals with foreign pensions to understand their reporting obligations and comply with tax filing requirements in both their country of residence and their country of origin. International pension transfers involve moving retirement assets from one country to another, often in the context of relocating or retiring abroad. These transfers can be complex and subject to various rules, regulations, and tax implications, depending on the countries involved and the specific pension plans being transferred. Some countries impose restrictions on the transfer of foreign pensions, either to protect their domestic pension systems or to ensure that individuals maintain adequate retirement savings. These restrictions may include limits on the amount of assets that can be transferred, waiting periods, or other conditions that must be met before a transfer can be completed. Transferring foreign pensions may have significant tax implications, depending on the countries involved and the specific pension plans being transferred. Tax consequences may include capital gains taxes, exit taxes, or other charges upon transferring pension assets. It is crucial for individuals to understand the tax implications of pension transfers and seek professional advice to minimize potential tax liabilities. Currency risks and exchange rates are important considerations when transferring foreign pensions, as fluctuations in exchange rates can significantly impact the value of the transferred assets. Individuals should carefully evaluate the potential risks and benefits of transferring pension assets between countries, considering the impact of currency fluctuations on their retirement savings. Totalization agreements are international agreements between countries designed to coordinate social security benefits for individuals who have worked in multiple countries. These agreements ensure that individuals are not disadvantaged due to their international work history and can help prevent double taxation of social security contributions, as well as provide eligibility for social security benefits in both countries. The Windfall Elimination Provision (WEP) is a U.S. Social Security rule that may reduce Social Security benefits for individuals who receive foreign pensions from work not covered by the U.S. Social Security. The WEP is intended to prevent individuals from receiving disproportionately high benefits by taking into account their foreign pension income when calculating their U.S. Social Security benefits. The Government Pension Offset (GPO) is a U.S. Social Security provision that may reduce spousal or survivor benefits for individuals who receive foreign government pensions based on their own work. The GPO is designed to equalize the treatment of individuals receiving foreign government pensions with those receiving U.S. government pensions, which are subject to a similar offset. Currency fluctuations can significantly impact the value of foreign pension income and assets, potentially affecting an individual's retirement income and financial security. As exchange rates fluctuate over time, individuals with foreign pensions must carefully monitor and manage these risks to ensure their retirement savings are not adversely affected. Managing foreign pensions can be challenging due to the diverse legal and regulatory environments that govern pension systems worldwide. Each country has its own set of rules, regulations, and requirements for pension plans, which can create complexities for individuals with foreign pensions and make it difficult to navigate the various systems involved. Inflation and cost-of-living adjustments can significantly impact the purchasing power of foreign pension income over time. Some foreign pension systems may not offer inflation-adjusted benefits or may have different cost-of-living adjustment mechanisms, which can result in varying levels of financial security for retirees who depend on foreign pensions. Foreign pension systems often lack portability between countries, meaning that pension benefits earned in one country may not be easily transferred to another country's pension system. This lack of portability can create challenges for individuals who have worked in multiple countries, as they may have difficulty consolidating their retirement assets or accessing their pensions when needed. Language barriers and limited access to information can create challenges for individuals managing foreign pensions. Navigating pension systems, understanding tax obligations, and accessing relevant resources can be more difficult when faced with language barriers or limited information, which may lead to confusion, misunderstandings, or even costly mistakes. Diversifying pension assets across multiple countries and investment types can help mitigate risks associated with currency fluctuations, regulatory changes, and other uncertainties. By spreading retirement savings across various assets, individuals can reduce the potential impact of negative events on their overall retirement income. Seeking professional financial planning services can help individuals with foreign pensions navigate the complexities of international retirement planning. Financial planners can provide guidance on tax compliance, pension transfers, asset allocation, and other aspects of retirement planning, helping individuals make informed decisions and optimize their foreign pensions. Regularly reviewing and adjusting pension plans is crucial for individuals with foreign pensions, as it helps ensure their retirement strategy remains aligned with their financial goals and evolving circumstances. Regular reviews can help identify potential issues or opportunities, such as changes in tax laws or currency risks, and allow individuals to make timely adjustments to their plans. Proper tax planning and compliance are essential for individuals with foreign pensions to minimize tax liabilities and avoid potential penalties. Understanding the tax implications of foreign pensions, reporting requirements, and any available tax relief mechanisms can help individuals manage their tax obligations and maximize their retirement income. Foreign pensions are retirement benefits earned outside an individual's home country and can include government-sponsored, employer-sponsored, or private pension plans. As individuals work and live in multiple countries, understanding and managing foreign pensions becomes critical to ensuring a comfortable and secure retirement. Proper planning and management of foreign pensions are essential for individuals to navigate the complexities of international retirement planning and make informed decisions. By understanding the challenges and utilizing appropriate strategies, individuals can optimize their foreign pensions, minimize potential risks, and ensure their retirement goals are met. Managing foreign pensions effectively is crucial to ensuring financial security in retirement. By addressing currency risks, tax implications, and regulatory challenges, individuals can help protect their retirement assets and maintain a stable income throughout their retirement years. For those with foreign pensions, seeking professional retirement planning services is an essential step toward securing a comfortable retirement.What Are Foreign Pensions?

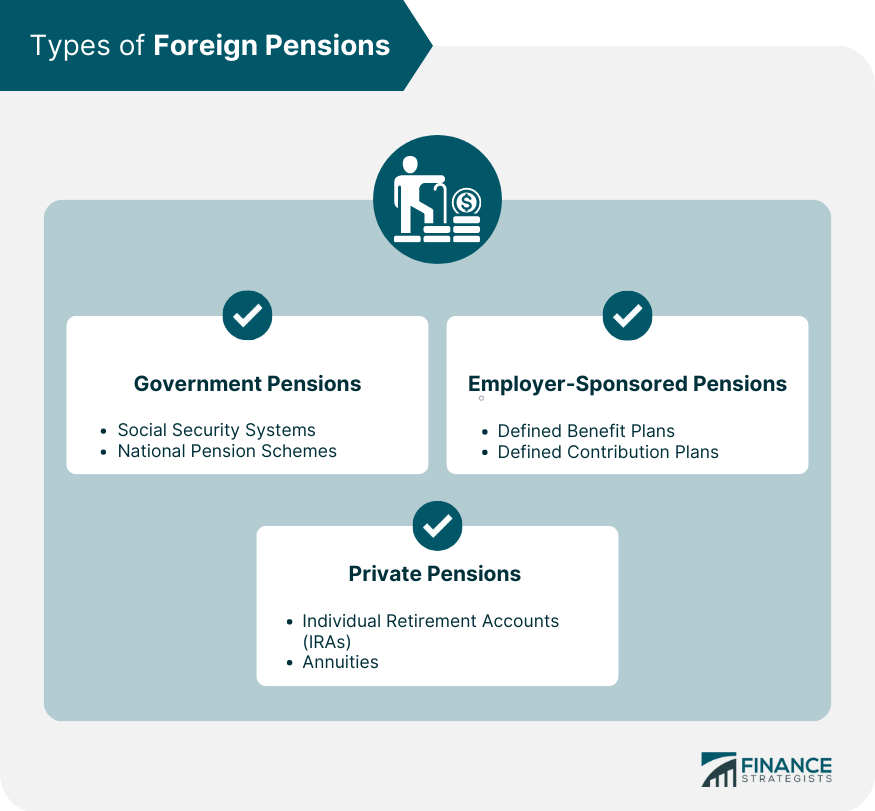

Types of Foreign Pensions

Government Pensions

Social Security Systems

National Pension Schemes

Employer-Sponsored Pensions

Defined Benefit Plans

Defined Contribution Plans

Private Pensions

Individual Retirement Accounts

Annuities

Taxation of Foreign Pensions

Tax Treaties and Agreements

Taxation in the Country of Origin

Taxation in the Country of Residence

Double Taxation Relief

Reporting Requirements and Tax Filing

Transfer of Foreign Pensions

International Pension Transfers

Pension Transfer Restrictions

Tax Implications of Pension Transfers

Currency Risks and Exchange Rates

Impact of Foreign Pensions on Social Security Benefits

Totalization Agreements

Windfall Elimination Provision

Government Pension Offset

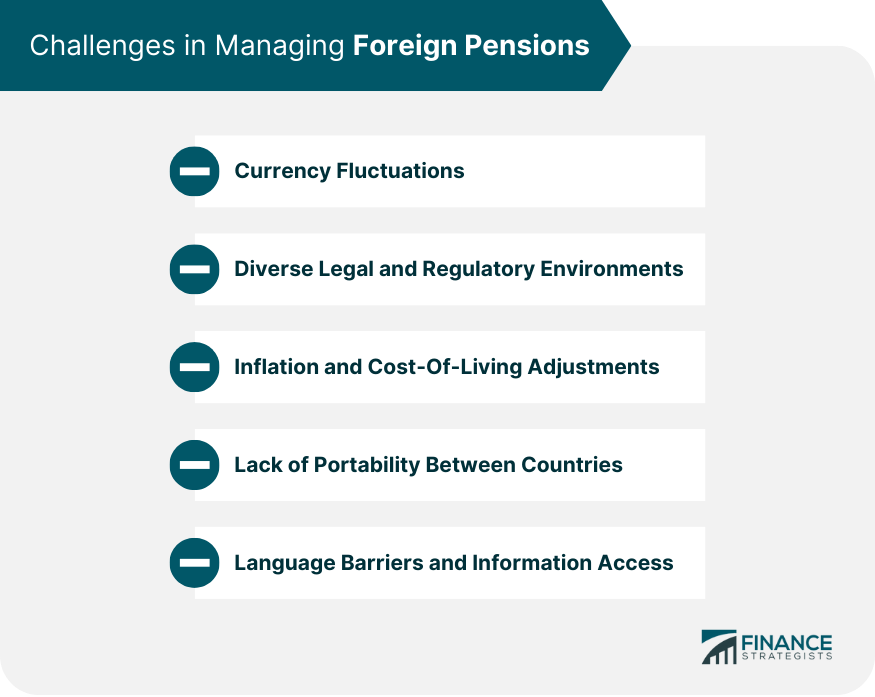

Challenges in Managing Foreign Pensions

Currency Fluctuations

Diverse Legal and Regulatory Environments

Inflation and Cost-of-Living Adjustments

Lack of Portability Between Countries

Language Barriers and Information Access

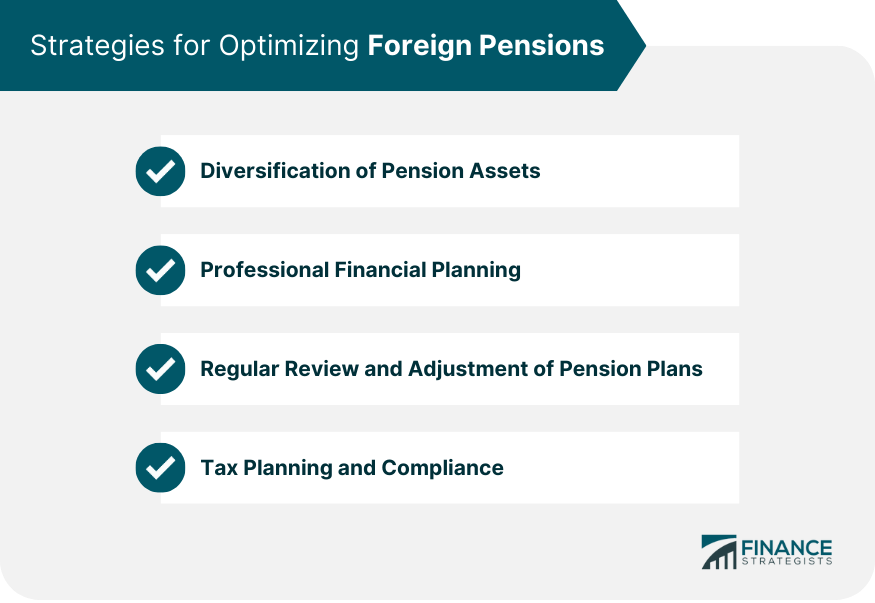

Strategies for Optimizing Foreign Pensions

Diversification of Pension Assets

Professional Financial Planning

Regular Review and Adjustment of Pension Plans

Tax Planning and Compliance

Final Thoughts

Foreign Pensions FAQs

Foreign pensions are retirement benefits earned and accumulated outside one's home country, including government-sponsored, employer-sponsored, or private pension plans. They are important for individuals who have worked in multiple countries, as proper management of foreign pensions ensures financial security, tax compliance, and avoidance of potential penalties during retirement.

The taxation of foreign pensions varies between countries. In the country of origin, taxes may be imposed on pension contributions, investment returns, or pension benefits. In the country of residence, foreign pension income may be subject to taxes, although tax exemptions or credits may be available. Tax treaties and agreements can provide double taxation relief and clarify the tax treatment of foreign pensions.

Managing foreign pensions can be challenging due to currency fluctuations, diverse legal and regulatory environments, inflation and cost-of-living adjustments, lack of portability between countries, and language barriers or limited information access. These factors can make it difficult to consolidate retirement assets, comply with tax obligations, and navigate pension systems across multiple countries.

To optimize foreign pensions, individuals can diversify their pension assets, seek professional financial planning services, regularly review and adjust their pension plans, and maintain proper tax planning and compliance. These strategies can help mitigate risks, ensure tax compliance, and maximize retirement income from foreign pensions.

Foreign pensions can impact U.S. Social Security benefits through totalization agreements, the Windfall Elimination Provision (WEP), and the Government Pension Offset (GPO). Totalization agreements coordinate social security benefits between countries, while the WEP and GPO are provisions that may reduce U.S. Social Security benefits for individuals who receive foreign pensions based on work not covered by U.S. Social Security or for those receiving foreign government pensions, respectively.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.