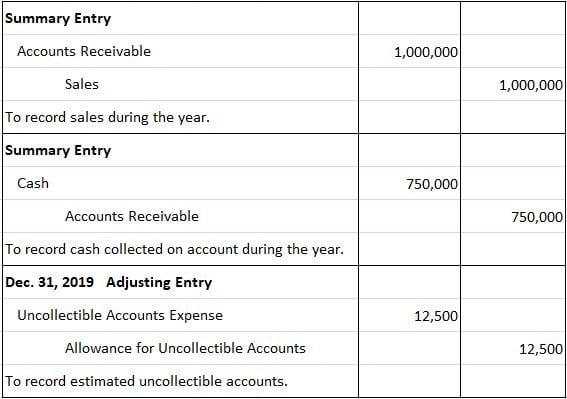

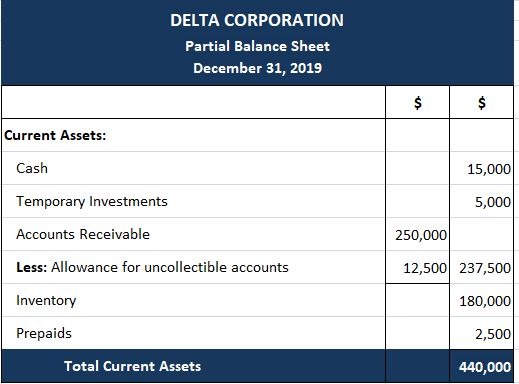

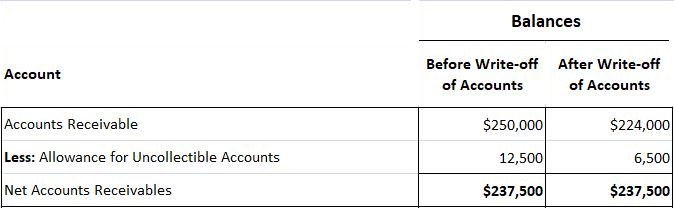

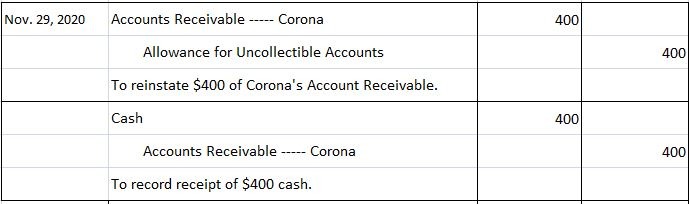

Those receivables that the firm is unable to collect the full amount due from the customer are called uncollectible accounts. The primary accounting issue regarding accounting for uncollectible accounts is matching the bad debts with the sales of the period that gave rise to the bad debts. That is, the bad-debt expense should be recognized in the period in which the sale took place and the receivable was generated, not in the period in which management determined that the customer was unable or unwilling to pay. The accounting problem arises because it may be the following year before management discovers that a sale made in the current year will not be collectible. Waiting to record the bad-debt expense in the year following the sale would violate the matching convention. In order to provide the best matching, the allowance method is used. Under the allowance method, the uncollectible account expense for the period is matched against the sales for that period. This requires estimating the uncollectible account expense in the period of the sale. An estimate is required because it is impossible to know with certainty which accounts outstanding at the end of the year will become uncollectible during the next year. This estimate is usually recorded through an adjusting journal entry at year-end. Although estimates are uncertain, accountants feel that the benefits of applying the matching convention outweigh the problems associated with estimates. To demonstrate the application of the allowance method, we will first discuss the journal entries that must be made, and then we will examine the different methods used to make the required estimates. In order to understand the required journal entries used with the allowance method, assume that during 2019, Delta Corporation’s first year in business, sales totaled $1 million. All sales made on credit, and cash collections on account totaled $750,000. After analyzing the ending balance of $250,000 in Accounts Receivable, management estimated that $12,500 of these accounts would ultimately become uncollectible. The summary journal entries required to record the sales, cash collections, and the $12,500 in uncollectible accounts are: The first two entries are the usual ones to record sales on account and the subsequent collection of cash. However, the adjusting entry on December 31, 2019, to record the estimated uncollectible accounts needs to be explained. The debit part of the adjusting entry is made to the Uncollectible Accounts Expense account. Another title for this account is Bad Debt Expense, This account is closed to Income Summary and is generally shown as a selling expense on the income statement. However, some firms show this item as a deduction from gross sales in arriving at net sales. The credit part of the entry is to an account called Allowance for Uncollectible Accounts. This account, rather than Accounts Receivable, is credited because the firm is only making a total dollar estimate of uncollectible accounts and does not know with certainty which particular account will ultimately prove uncollectible. If a firm knows that a particular account is, in fact, uncollectible, it should already have been written off. The Allowance for Uncollectible Accounts is a contra-asset account in that it is an asset account with a credit balance. Other titles for this account include Allowance for Doubtful Accounts and Allowance for Debts. In preparing a balance sheet, the dollar balance in the Allowance account is netted against the dollar balance of gross accounts receivable. This net amount represents management’s estimate of the net realizable value of the firm’s receivables. Presented below is the current asset section of the Delta Corporation’s balance sheet at December 31, 2019 after the adjusting entry has been made. Because this is the first year of the firm’s operations, the balance in the Allowance account equals the amount of the Journal entry. However, In future years this may not be the case. To extend this Illustration, assume that the following events occur in 2020: Based on this data, Delta makes the following entry on April 14, 2020, to write off the $6,000 account: As this entry shows, the debit part of the entry is to the Allowance account. The entry is not to the Uncollectible Accounts Expense account because we are assuming that the $6,000 is included in the $12,500 debit to expense as part of the December 31, 2019 adjusting entry. The credit part is to Accounts Receivable—–Corona. This part of the entry must be posted to both the general ledger accounts receivable and to Corona’s account in the subsidiary accounts receivable ledger. After the $6,000 entry to write off the specific account, the net amount of accounts receivable (Account Receivable less Allowance for Uncollectible Accounts) remains the same, as illustrated below: These identical balances result from the fact that the adjustment that actually decreased the balance in the net receivables took place on December 31. 2019. The entry on April 14, 2020 just decreases the Allowance account and the Accounts Receivable account by the same amount, $6,000. In effect, once a particular account is determined to be bad, the balance that pertains to that account is taken out of both the Allowance account and the Accounts Receivable account, and there is -no effect on net receivables. In some cases, a customer whose account has been written off will subsequently pay part or all of his or her account. For example, in the Corona case, Delta’s management decided it was prudent to write off the entire balance when Corona entered bankruptcy proceedings. This is because in Delta’s opinion the outcome of such proceedings is uncertain. In November 2020, when Delta received $400 as its full settlement, it had to make the following two entries: The first entry reinstates Corona’s account receivable in the amount Of $400. This entry is a reversal, in the amount of $400, of the entry to write off the receivable. The second entry records the receipt of the $400. These two entries should not be combined. For internal control purposes, therefore, unusual entries or combination of entries should be avoided. The previous entries demonstrate the entries made to write off an account declared uncollectible and reinstate an account that had previously been written off. During the year, similar entries are made to record other accounts declared uncollectible. At the end of 2020, the Delta Corporation would again make an estimate of its uncollectible accounts for 2020 and make the necessary adjusting entry to Uncollectible Accounts Expense and the Allowance for Uncollectible Accounts to record this amount. How this estimate is made will be considered next. As we have shown, the allowance method is based on the accountant’s ability to estimate future uncollectible accounts that result from current year’s sales. The percentage-of-net-sales method and the aging method are the two methods that have been developed to make this estimate. Regardless of which method is used, the actual accounts written off seldom exactly equal the estimates made in the prior year. However, this presents no problem in accounting for accounts receivable. If fewer accounts in dollars are written off than previously estimated, the Allowance account will have a credit balance prior to the adjustment. The adjustment will then increase this balance to reflect management’s new estimate of the uncollectible accounts. If more accounts are written off than previously estimated, the Allowance account will have a temporary debit balance prior to the year-end adjustment. This debit balance will then be eliminated when the new adjusting entry is made. Estimates are inherent in accounting because the accountant attempts to match revenues and expenses. Most individuals feel that the benefits of this proper matching outweigh the disadvantages of using estimates. Furthermore, for stable companies, the amount of receivables and uncollectible accounts tends to be steady from year to year. This point can be illustrated by looking at the following data taken from a recent annual report of J. C. Penney: The following table presents key operating data relative to credit operations (in millions): The Company’s policy is to write off accounts when the scheduled minimum payment has not been received for six consecutive months, or if any portion of the balance is more than 12 months past due, or if it is otherwise determined that the customer is unable to pay. Collection efforts continue subsequent to write off, and recoveries are applied as a reduction of bad debt losses. As we have seen, reasonable errors in a prior year’s estimates are adjusted in current and future years; the accountant does not retroactively change a prior year’s statement. However, if estimates such as uncollectible accounts are consistently incorrect, management should reevaluate the method used to make the estimate.What Are Uncollectible Accounts?

Accounting for Uncollectible Accounts

Using the Allowance Method to Record Uncollectible Accounts Expense

Journal Entries to Record Original Estimate

Journal Entries to Record Actual Write-Off

Journal Entries to Record Subsequent Collection of Accounts Previously Written Off.

How to Estimate Uncollectible Accounts Expense

Difference between Estimates and Actual Experience

Uncollectible Accounts Receivable FAQs

An uncollectible accounts receivable is an invoice for goods or services that the customer has not paid, and is unlikely to ever be collected.

To record uncollectible accounts receivable in your accounting records, you will need to write off the outstanding balance on the invoice as a bad debt expense and reduce the accounts receivable balance accordingly.

Ways of dealing with uncollectible accounts receivables include sending reminders and dunning letters, negotiating payment plans and discounts with customers, and writing off bad debts as an expense.

An uncollectible accounts receivable should be written off when it is determined that the customer will not be able to pay the invoice or if the amount of time has passed in which collecting the debt would no longer make economic sense.

The two main methods of estimating Uncollectible Accounts Receivable are the percentage-of-net-sales method and the aging method. The percentage-of-net-sales method is the simpler of the two and involves calculating an allowance based on a percentage of net sales. The aging method is more complex and requires analyzing customer accounts to determine their collectibility. This method is usually superior as it takes into account factors such as past-due payments and the payment habits of customers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.