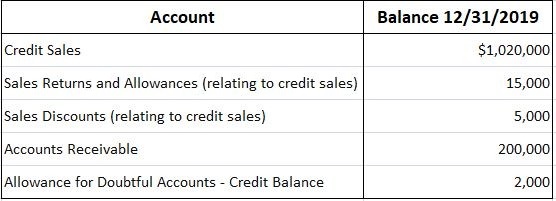

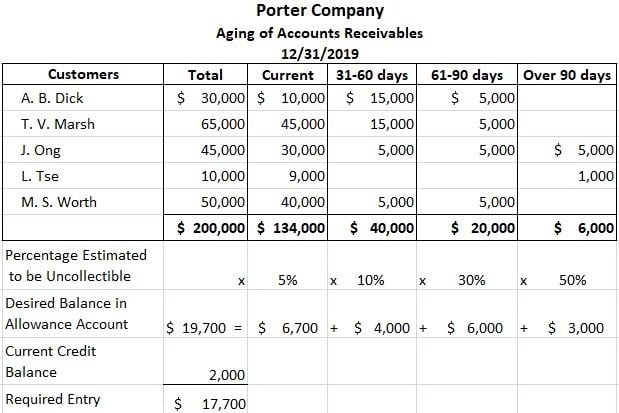

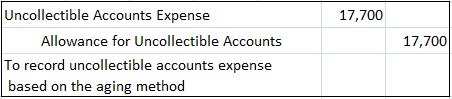

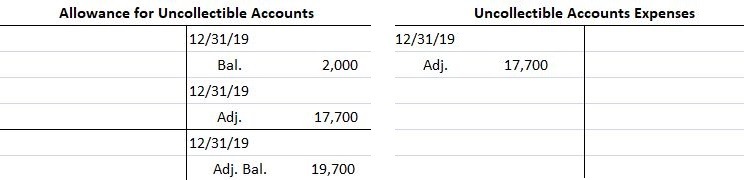

The aging method involves determining the desired balance in the Allowance for Uncollectible Accounts. The aim is to estimate what percentage of outstanding receivables at year-end will not be collected. This amount becomes the desired ending balance in the Allowance for Uncollectible Accounts. A credit entry is made to Allowance for Uncollectible Accounts, thereby adjusting the previous balance to the new, desired balance. The debit part of the entry is made to the Uncollectible Accounts Expense account. The aging method is often referred to as the balance sheet approach because the accountant attempts to measure, as accurately as possible, the net realizable value of Accounts Receivable, which is a balance sheet figure. The method used to estimate the desired balance in the allowance account is called the aging of accounts receivable. It involves dividing the balance in the Accounts Receivable account into age categories based on the length of time they have been outstanding. Categories such as current, 31—60 days, 61—90 days, and over 90 days are often used. On the assumption that the longer an account is outstanding, the less likely its ultimate collection is, an increasing percentage is applied to each of these categories. The total of these figures represents the desired balance in the account Allowance for Uncollectible Accounts. To demonstrate the application of the aging method, we will use the data from the Porter Company. At the end of 2019, the balance in Accounts Receivable was $200,000, and an aging schedule of the accounts is presented below. For the sake of simplicity, let's assume that the entire $200,000 balance in Accounts Receivable consists of only 5 customers. Based on the data shown above, the Porter Company makes the following adjusting entry on 31 December 2019 to record the Uncollectable Accounts Expense: After the entry is posted, the T-accounts appear as follows: A number of points should be highlighted about this illustration. Both the percentage of net sales and aging methods are generally accepted accounting methods in that they both attempt to match revenues and expenses. The percentage of net sales method aims to determine the amount of uncollectible accounts expense, while the aging method focuses on calculating the balance in the account Allowance for Uncollectible Accounts. These methods, therefore, show different balances in both the expense and contra-asset accounts. This is illustrated below using data from the Porter Company example shown above. These differences show that management can choose from various methods when applying generally accepted accounting principles and that these choices influence the firm's financial statements. Once a method of estimating bad debts is chosen, it should be followed consistently. This will enhance the comparability of the financial statements. Both the aging and percentage of net sales methods, as well as other methods, are used in practice. While the percentage of net sales method is easier to apply, the aging method forces management to analyze the status of their accounts receivable and credit policies annually. Some firms use both methods. For example, in these firms, the percentage of net sales method is typically used to prepare monthly and quarterly statements, whereas the aging method is used to make the final adjustment at year-end.What Is the Aging Method?

Example

Given that the Allowance account had a $2,000 credit balance prior to adjustment, the required entry is for $17,700, or the difference between $19,700 and $2,000.

In some situations, the Allowance account may have a debit balance before the adjustment.

This may occur if during the year more accounts were written off as uncollectible than had been estimated for in the prior year.

In this situation, the debit balance should be added to the desired credit balance in the Allowance account to figure the correct amount of the entry.

For example, if Porter Company's Allowance account had a $300 debit balance before the entry for the uncollectible accounts expense, the Allowance account would require a credit entry of $20,000 to establish the necessary ending balance of $19,700.

Generally, these percentages are based on past experience adjusted for the current economic and credit conditions.

These percentages should be evaluated on a regular basis and adjusted when necessary.

When this happens, the account should be written off by debiting the Allowance account and crediting Accounts Receivable before figuring out the desired ending balance in the Allowance account.

In effect, this particular account is eliminated from the aging process because it is already considered uncollectible.Comparison of Percentage of Net Sales Method and Aging Method

Aging Method of Accounts Receivable/Uncollectible Accounts FAQs

The aging method is used because it helps managers analyze individual accounts. This provides information which can be used to determine whether any further collection efforts are justified or not. The aging method also makes it easier for management to make changes in credit policies and discounts offered to customers.

The percentage of net sales method produces a larger amount because it takes all Accounts Receivable into account, whether past due or not. The aging method only takes into account accounts that are considered by management to be uncollectible.

The allowance account represents an estimated amount of uncollectible accounts expense based on past experience adjusted for current economic and credit conditions.

It is determined by adding to $0 any additions to the allowance account during the year, then adding to that total any write-offs of Accounts Receivable during the year. And if there are no additions or write-offs, the balance in the account is zero.

To determine the amount of uncollectible accounts, an aging method is used for a collection system that is divided into time periods.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.