Retirement plan benchmarking is the process of comparing and analyzing a company's retirement plan with industry standards, peer groups, and national averages to identify areas of improvement, ensure competitiveness, and optimize plan performance. Benchmarking in retirement planning is crucial for plan sponsors to ensure they provide a competitive and efficient retirement plan for their employees. It helps identify best practices, enhance plan design, and improve participant outcomes, ultimately contributing to employees' financial well-being in retirement. The primary objectives of retirement plan benchmarking include evaluating plan design and performance, understanding industry trends, identifying areas for improvement, and ensuring regulatory compliance. This process enables plan sponsors to make informed decisions and implement changes to maximize plan effectiveness. Eligibility requirements determine who can participate in a retirement plan and when. By benchmarking these requirements, plan sponsors can ensure they offer competitive plans to attract and retain employees while maintaining compliance with applicable regulations. Vesting schedules dictate when employees acquire full ownership of employer contributions to their retirement accounts. Benchmarking vesting schedules helps plan sponsors balance employee retention and plan costs, while ensuring their plan remains attractive in the competitive marketplace. Contribution structures involve employer and employee contributions to the retirement plan. Comparing contribution structures with benchmark data allows plan sponsors to assess their plan's competitiveness and identify potential enhancements to improve participant outcomes. Distribution options refer to the methods available for participants to access their retirement funds. Benchmarking these options helps plan sponsors understand the flexibility and features offered by similar plans and assess whether their plan meets the diverse needs of their participants. Asset allocation refers to the distribution of investments in a retirement plan across various asset classes. By benchmarking asset allocation, plan sponsors can assess their plan's risk and return profile and ensure it aligns with participants' long-term retirement objectives. Benchmarking investment performance involves comparing the returns of a retirement plan's investment options with relevant market indices or peer group performance. This analysis helps plan sponsors identify underperforming investments and make adjustments as necessary to optimize plan returns. Risk tolerance relates to the level of investment risk plan participants are willing to accept. Benchmarking risk tolerance helps plan sponsors understand whether their plan's investment options align with participants' risk preferences and offer adequate diversification to meet their retirement goals. Fund management fees are the costs associated with managing the investment options within a retirement plan. Comparing these fees against industry benchmarks allows plan sponsors to assess the cost-effectiveness of their plan and identify potential opportunities to reduce fees and enhance participant returns. Participation rates measure the percentage of eligible employees who actively participate in a retirement plan. Benchmarking participation rates enables plan sponsors to gauge the success of their plan in engaging employees and identify potential strategies to increase enrollment and improve retirement outcomes. Savings rates refer to the percentage of income that plan participants contribute to their retirement accounts. By comparing savings rates with benchmark data, plan sponsors can assess the effectiveness of their plan in encouraging participants to save for retirement and identify potential enhancements to boost savings rates. Retirement readiness is the degree to which plan participants are financially prepared for retirement. Benchmarking retirement readiness helps plan sponsors evaluate the success of their plan in supporting participants' retirement goals and identify areas for improvement to ensure participants achieve financial security in retirement. Financial literacy refers to plan participants' understanding of financial concepts and their ability to make informed decisions about retirement planning. By benchmarking financial literacy, plan sponsors can identify gaps in participants' knowledge and develop targeted education and communication strategies to enhance their understanding of retirement planning concepts. Peer groups consist of organizations with similar characteristics, such as size, industry, or employee demographics. Benchmarking against peer groups helps plan sponsors understand how their retirement plan compares to similar organizations, providing valuable insights for improvement and competitiveness. Industry standards represent retirement plan practices and performance metrics commonly observed within a specific industry. Comparing a plan against industry standards helps plan sponsors identify best practices, assess plan effectiveness, and ensure alignment with industry norms. National averages provide a broader comparison point for retirement plan benchmarking by looking at trends and metrics across multiple industries and regions. Benchmarking against national averages helps plan sponsors understand the general landscape of retirement plans and evaluate their plan's competitiveness on a larger scale. Plan documents contain essential information about retirement plan features, policies, and investment options. Reviewing these documents is the first step in the benchmarking process, as it provides the necessary data for comparison with benchmark partners and industry standards. Investment statements provide information on investment performance, fees, and asset allocation within a retirement plan. Collecting and analyzing investment statements is crucial for benchmarking investment-related components of a retirement plan and identifying areas for improvement. Participant surveys can provide valuable insights into plan participants' needs, preferences, and understanding of the retirement plan. Survey data helps plan sponsors identify areas for improvement in plan design, communication, and education to better support participants' retirement goals. Quantitative analysis involves the numerical comparison of retirement plan data with benchmark partners and industry standards. This analysis helps plan sponsors identify specific areas where their plan outperforms or underperforms relative to benchmarks, providing a clear direction for improvement efforts. Qualitative analysis involves a more in-depth review of plan features, policies, and participant feedback to better understand the context and underlying reasons for observed trends. This analysis helps plan sponsors gain a deeper understanding of their plan's strengths and weaknesses and identify targeted strategies for improvement. The benchmarking process culminates in the identification of strengths and weaknesses within a retirement plan. By understanding these areas, plan sponsors can prioritize and implement improvements to enhance plan competitiveness, participant outcomes, and overall plan effectiveness. Benchmarking results can reveal opportunities for plan design modifications, such as adjusting eligibility requirements, vesting schedules, or distribution options. These modifications can enhance the plan's competitiveness and better meet participants' retirement planning needs. Benchmarking may identify underperforming investment options or gaps in asset allocation. Plan sponsors can use this information to adjust investment offerings, ensuring that participants have access to a diversified and high-performing investment lineup. Benchmarking results can highlight gaps in participants' financial literacy or low engagement with the retirement plan. Plan sponsors can address these issues by developing targeted communication and education strategies to improve participant understanding and encourage greater involvement in retirement planning. Implementing changes to a retirement plan often involves collaboration with plan providers, such as recordkeepers or investment managers. Working together, plan sponsors and providers can effectively implement changes to enhance plan competitiveness and participant outcomes. Transparent communication of plan changes to participants is essential for ensuring their understanding and buy-in. Plan sponsors should provide clear, concise information about changes and their potential impact on participants' retirement planning efforts. After implementing changes, plan sponsors should monitor their effects on plan performance and participant outcomes. This ongoing assessment allows for necessary adjustments and fine-tuning to ensure the plan continues to meet its objectives and support participants' retirement goals. Continuous benchmarking involves conducting regular evaluations of a retirement plan to identify emerging trends, new best practices, and potential areas for improvement. This proactive approach helps plan sponsors stay ahead of industry changes and maintain a competitive retirement plan. As the retirement planning landscape evolves, plan sponsors must adapt to new industry trends, such as technological advancements, demographic shifts, or regulatory changes. Continuous benchmarking allows plan sponsors to identify and respond to these trends, ensuring their plan remains relevant and effective. Through ongoing benchmarking and evaluation, plan sponsors can identify and address potential issues before they negatively impact the plan's success. This proactive approach contributes to long-term plan success and helps participants achieve their retirement goals. The effectiveness of benchmarking depends on the availability and quality of data. Limited or inconsistent data can make it challenging to draw accurate conclusions and implement meaningful changes. Plan sponsors should prioritize collecting and maintaining high-quality data to support effective benchmarking efforts. Retirement plans must comply with various regulations, which can change frequently. Plan sponsors must stay current with these regulatory changes and ensure their benchmarking efforts reflect current requirements to maintain compliance and avoid potential penalties. While benchmarking helps identify best practices and industry trends, plan sponsors must balance adopting these standards with customizing their plan to meet their organization's unique needs. Striking the right balance can be challenging, but is critical for creating a plan that effectively supports participants' retirement goals. Each participant in a retirement plan has unique financial needs, goals, and circumstances. It can be difficult for plan sponsors to address these individual needs while also adhering to industry benchmarks and best practices. Plan sponsors should strive to develop a plan that offers flexibility and customization while remaining competitive in the market. Retirement plan benchmarking is a critical process for plan sponsors, helping them evaluate plan performance, identify areas for improvement, and ensure their plan remains competitive. By using benchmarking, plan sponsors can enhance plan design, optimize investment options, and improve participant outcomes, ultimately contributing to participants' financial well-being in retirement. Plan sponsors should prioritize ongoing evaluation and adaptation to ensure their retirement plan continues to meet the needs of participants and remains competitive in the market. Regular benchmarking and monitoring of plan performance will enable plan sponsors to proactively address emerging trends and challenges. Plan sponsors are encouraged to prioritize benchmarking as a key component of their retirement planning strategy. By continually assessing their plan's performance and making necessary adjustments, plan sponsors can provide a valuable retirement benefit to employees and help them achieve their retirement goals. For organizations seeking assistance with retirement plan benchmarking and management, working with professional retirement planning services can be highly beneficial. What Is Retirement Plan Benchmarking?

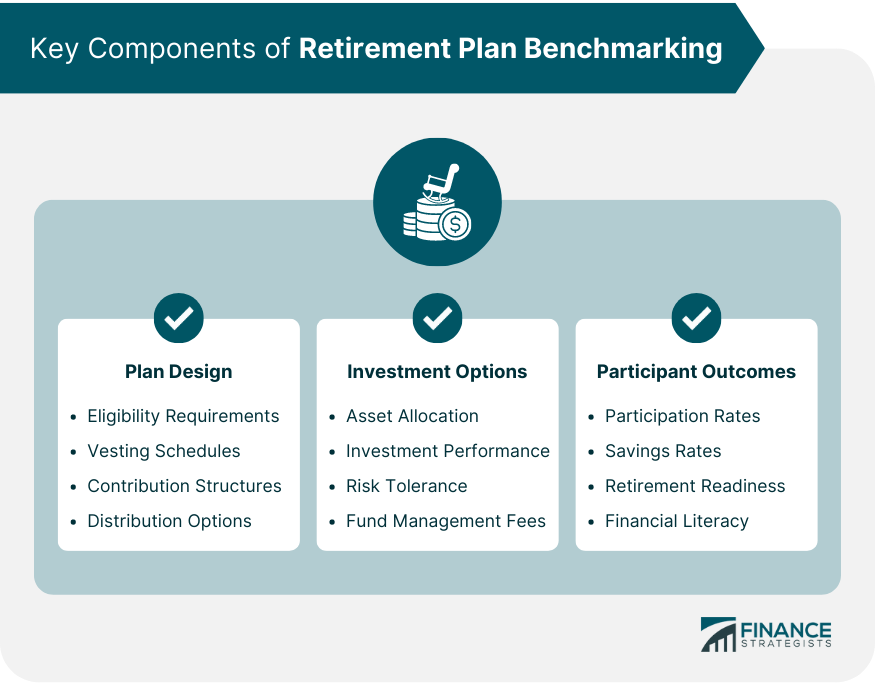

Key Components of Retirement Plan Benchmarking

Plan Design

Eligibility Requirements

Vesting Schedules

Contribution Structures

Distribution Options

Investment Options

Asset Allocation

Investment Performance

Risk Tolerance

Fund Management Fees

Participant Outcomes

Participation Rates

Savings Rates

Retirement Readiness

Financial Literacy

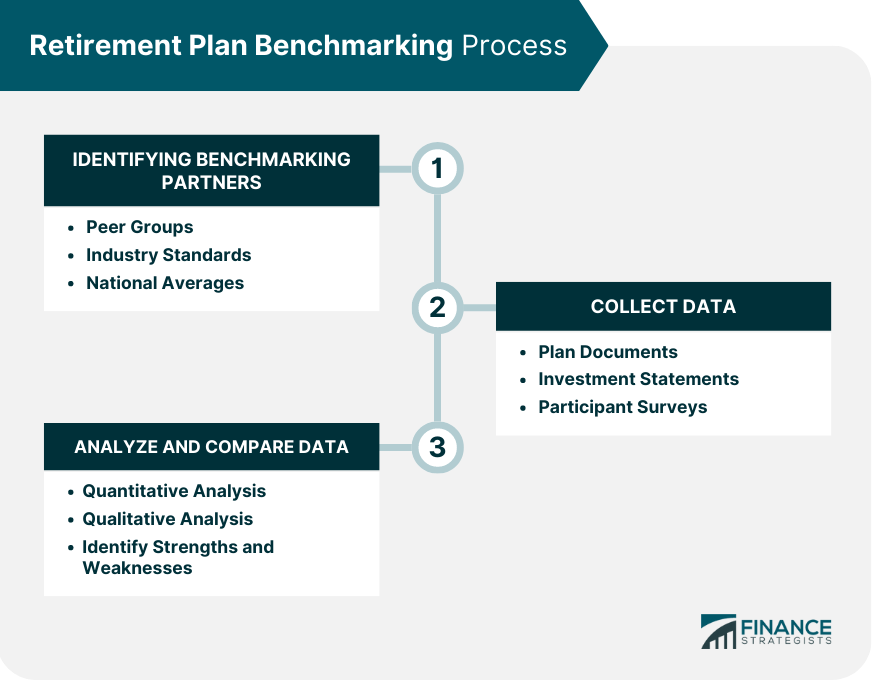

Retirement Plan Benchmarking Process

Identifying Benchmarking Partners

Peer Groups

Industry Standards

National Averages

Collecting Data

Plan Documents

Investment Statements

Participant Surveys

Analyzing and Comparing Data

Quantitative Analysis

Qualitative Analysis

Identifying Strengths and Weaknesses

Utilizing Benchmarking Results

Identifying Areas for Improvement

Plan Design Modifications

Investment Option Changes

Participant Communication and Education

Implementing Changes

Collaborating With Plan Providers

Communicating Changes to Participants

Monitoring Results and Adjusting as Necessary

Continuous Benchmarking

Regular Evaluations

Adapting to Industry Trends

Ensuring Long-Term Plan Success

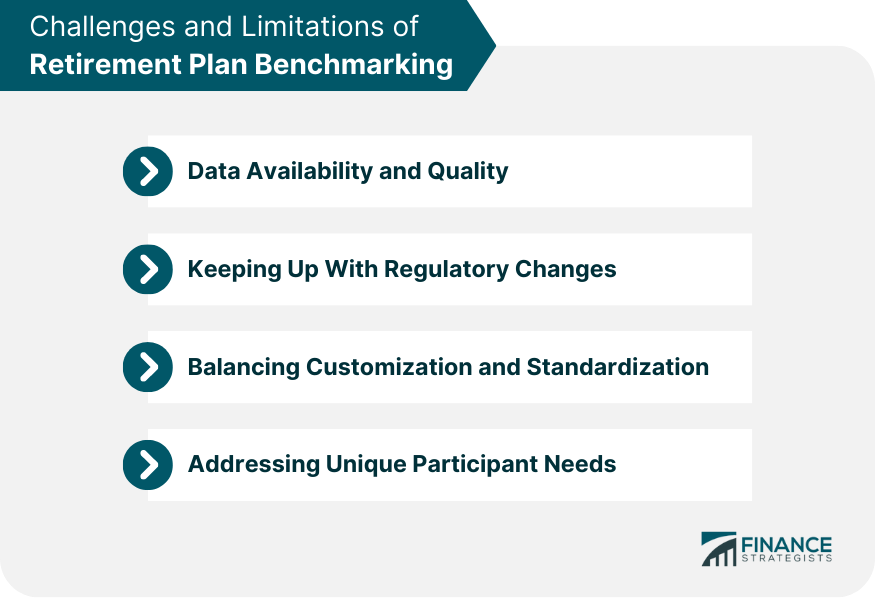

Challenges and Limitations of Retirement Plan Benchmarking

Data Availability and Quality

Keeping Up With Regulatory Changes

Balancing Customization and Standardization

Addressing Unique Participant Needs

Final Thoughts

Retirement Plan Benchmarking FAQs

Retirement Plan Benchmarking is the process of comparing and analyzing a company's retirement plan with industry standards, peer groups, and national averages to identify areas of improvement, ensure competitiveness, and optimize plan performance. It is important for organizations because it helps them provide competitive and efficient retirement plans for employees, enhance plan design, and improve participant outcomes.

By conducting Retirement Plan Benchmarking, plan sponsors can identify best practices, trends, and potential areas for improvement. This process enables them to make informed decisions and implement changes in plan design, investment options, and participant communication and education, ultimately leading to better retirement outcomes for plan participants.

The key components of Retirement Plan Benchmarking include plan design (eligibility requirements, vesting schedules, contribution structures, and distribution options), investment options (asset allocation, investment performance, risk tolerance, and fund management fees), and participant outcomes (participation rates, savings rates, retirement readiness, and financial literacy).

Some challenges and limitations of Retirement Plan Benchmarking include data availability and quality, keeping up with regulatory changes, balancing customization and standardization, and addressing unique participant needs. Plan sponsors should be aware of these challenges and work to overcome them to ensure an effective benchmarking process.

Organizations can utilize Retirement Plan Benchmarking results by identifying areas for improvement, implementing changes in collaboration with plan providers, communicating changes to participants, and engaging in continuous benchmarking through regular evaluations and adaptation to industry trends. This proactive approach contributes to the long-term success of a retirement plan and helps participants achieve their retirement goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.