An opt-out provision in retirement planning allows employees to choose not to participate in their employer-sponsored retirement plan. This feature gives employees more control over their retirement savings strategies and investment choices. While participation in employer-sponsored retirement plans is generally encouraged due to the benefits they offer, such as employer matching contributions and tax advantages, there may be reasons why an employee chooses to opt-out. For example, an employee might choose to opt out of an employer-sponsored plan if they prefer to invest their money in other ways, such as through a personal brokerage account, real estate, or starting their own business. Alternatively, an employee might choose to opt-out if they already have substantial retirement savings in another account, such as an IRA or a retirement plan from a previous employer, and they want to avoid over-contributing to retirement accounts. Opt-out provisions play a significant role in retirement planning by allowing employees to make informed decisions about their retirement savings. They also encourage employees to engage with their retirement plans and make proactive choices about their financial futures. A traditional opt-out provision is the standard approach to retirement plan enrollment. In this scenario, employees are not automatically enrolled in their employer's retirement plan. Instead, they must take active steps to enroll themselves. This approach puts the onus on the employee to understand the benefits of the plan, decide to participate, and complete the enrollment process. While this method gives employees full control, it may result in lower participation rates as some employees may neglect or delay enrollment. An automatic enrollment opt-out provision, also known as a negative election, is a more proactive approach to retirement plan enrollment. In this scenario, employees are automatically enrolled in their employer's retirement plan unless they actively choose to opt-out. This method can significantly increase participation rates by removing barriers to enrollment and leveraging inertia. However, it's important that employees are fully informed about the automatic enrollment process, including the default contribution rate and investment options, so they can make adjustments if desired. Opt-out provisions, particularly automatic enrollment, can significantly increase participation rates in employer-sponsored retirement plans. By removing barriers to enrollment and simplifying the process, more employees are likely to participate in the plan. Opt-out provisions can lead to increased retirement savings for employees. Automatic enrollment, in particular, encourages employees to start saving for retirement earlier, which can lead to greater long-term savings. Opt-out provisions can help reduce administrative costs for employers by streamlining the enrollment process and minimizing paperwork. This can ultimately lead to more efficient plan administration and lower costs for both employers and employees. Opt-out provisions, especially automatic enrollment, may result in lower contribution rates for employees who do not actively choose their contribution levels. This can potentially lead to inadequate retirement savings over time. While opt-out provisions can increase participation rates, they may not guarantee that employees are saving enough for retirement. Employees who opt out or contribute at lower levels may not accumulate sufficient savings for a comfortable retirement. When employees do not actively choose their investments, they may end up in investment options that do not align with their risk tolerance or financial goals. This can lead to suboptimal investment performance and potential losses. The Employee Retirement Income Security Act (ERISA) establishes guidelines for opt-out provisions in retirement plans. These guidelines include specific rules for automatic enrollment and QDIAs to protect employees and employers. The Department of Labor (DOL) enforces ERISA regulations and provides additional guidance on opt-out provisions. Plan sponsors must comply with DOL regulations to ensure their opt-out provisions are legally compliant. Plan sponsors should consult with legal counsel to ensure their opt-out provisions comply with all relevant laws and regulations. This includes considering state and local laws that may impact their retirement plan. Clear communication with employees is essential for successful opt-out provision implementation. Employers should provide information about their retirement plan, including the opt-out provision, to ensure employees understand their options and can make informed decisions. Regular monitoring of the retirement plan and its opt-out provision is crucial for identifying any issues and making necessary adjustments. Employers should periodically review participation rates, contribution levels, and investment performance to ensure the plan is operating effectively and meeting employees' needs. Providing financial education and advice to employees can help them make informed decisions about their retirement planning, including whether to opt-out of the employer-sponsored plan. Employers can offer workshops, seminars, or access to financial advisors to support employees in making the best choices for their financial future. The opt-out provision in retirement planning is a critical feature that allows employees to choose not to participate in their employer-sponsored retirement plan. There are several main types of opt-out provisions: the traditional opt-out provision and the automatic enrollment opt-out provision. Each type has its unique benefits and considerations. Opt-out provisions have several benefits, including increased participation rates, increased retirement savings, and reduced administrative costs. However, they also have potential drawbacks, such as the possibility of lower contribution rates, inadequate retirement savings, and inappropriate investments. Legal requirements for opt-out provisions are primarily governed by the Employee Retirement Income Security Act (ERISA) and Department of Labor regulations. Plan sponsors must comply with these regulations to ensure their opt-out provisions are legally compliant. Best practices for implementing opt-out provisions include effective communication with employees, ongoing monitoring of the retirement plan, and offering financial education and advice. These practices can help ensure that the opt-out provision is implemented successfully and that employees are able to make informed decisions about their retirement planning. It is important for both employers and employees to understand the benefits and potential drawbacks of opt-out provisions to make the most of their retirement savings strategies.Definition of Opt-Out Provision

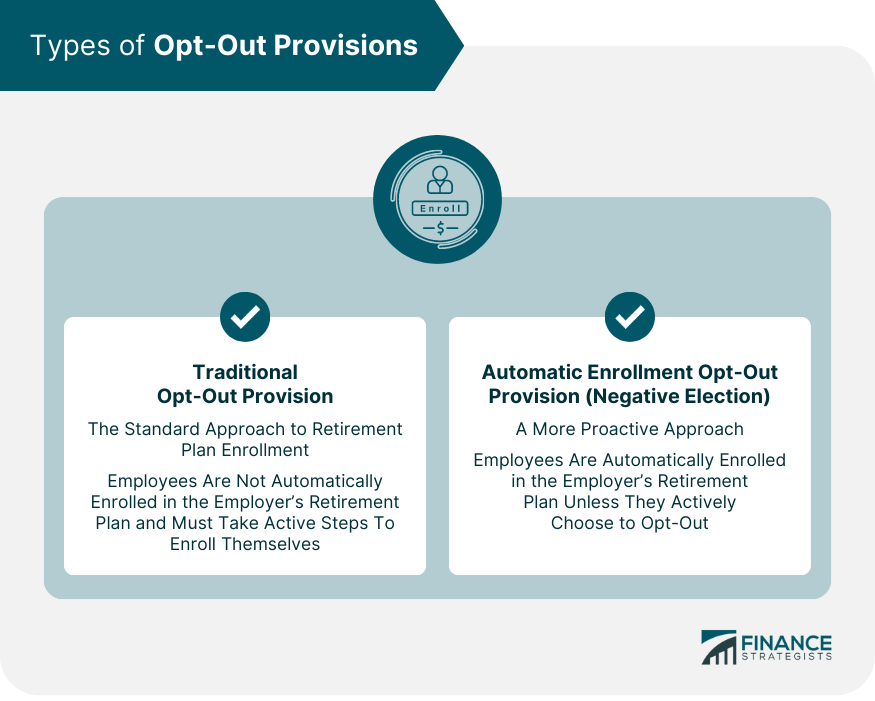

Types of Opt-Out Provisions

Traditional Opt-Out Provision

Automatic Enrollment Opt-Out Provision

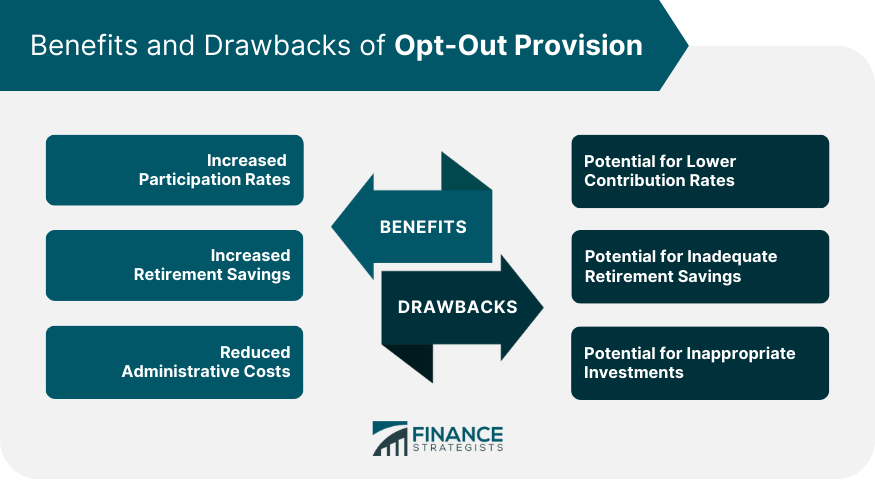

Benefits of Opt-Out Provision

Increased Participation Rates

Increased Retirement Savings

Reduced Administrative Costs

Drawbacks of Opt-Out Provision

Potential for Lower Contribution Rates

Potential for Inadequate Retirement Savings

Potential for Inappropriate Investments

Legal Requirements for Opt-Out Provision

ERISA Requirements

Department of Labor Regulations

Other Legal Considerations

Best Practices for Opt-Out Provision Implementation

Effective Communication

Ongoing Monitoring

Offering Financial Education and Advice

Final Thoughts

Opt-Out Provision FAQs

An Opt-Out Provision is a feature in retirement plans that allows employees to choose not to participate in a plan automatically.

The primary benefits of Opt-Out Provision include increased participation rates, higher retirement savings, and reduced administrative costs.

There are three main types of Opt-Out Provisions: traditional, automatic enrollment, and Qualified Default Investment Alternative (QDIA).

The potential drawbacks of Opt-Out Provision include lower contribution rates, inadequate retirement savings, and inappropriate investments.

Opt-Out Provision is subject to the requirements of the Employee Retirement Income Security Act (ERISA) and Department of Labor regulations, as well as other legal considerations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.