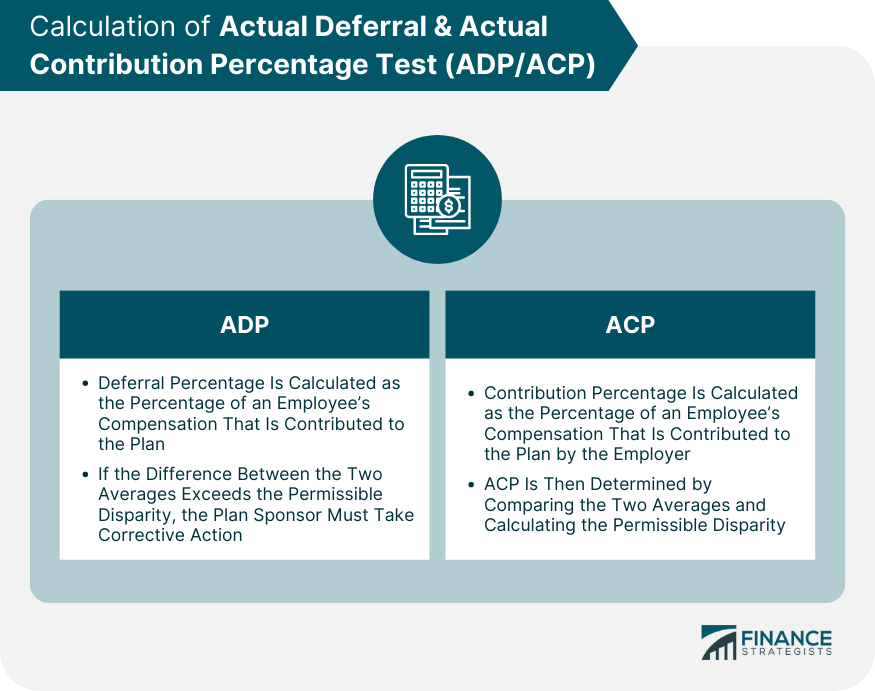

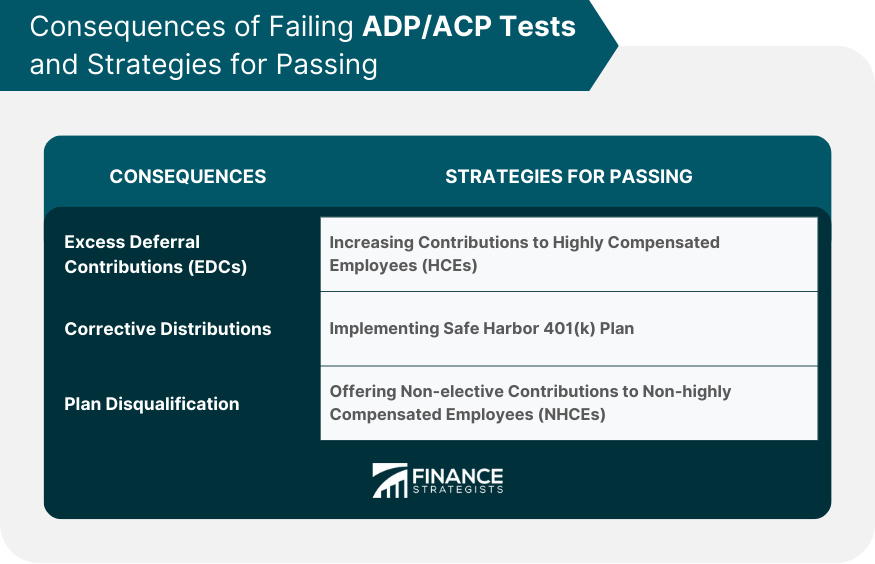

The Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) tests are two tests used by employers to ensure that their 401(k) plans are in compliance with IRS regulations. These tests are used to determine whether the plan is providing benefits to a sufficiently broad range of employees and to prevent highly compensated employees (HCEs) from disproportionately benefiting from the plan. The ADP test measures the average percentage of employee deferrals to the plan for both HCEs and non-highly compensated employees (NHCEs). The ACP test measures the average percentage of employer matching contributions or other non-elective contributions to the plan for both HCEs and NHCEs. ADP and ACP tests are critical for ensuring that 401(k) plans are fair and equitable for all employees. Failure to meet these tests can result in significant tax penalties for the plan sponsor, as well as lost benefits for plan participants. By conducting these tests, plan sponsors can ensure that their plans are providing meaningful benefits to all employees and avoiding any unintended consequences of the plan design. It is important for plan sponsors to understand the requirements and compliance standards associated with these tests to avoid costly mistakes and maintain a successful plan. The ADP test measures the average percentage of employee deferrals to the plan for both HCEs and NHCEs. This test is used to ensure that the plan is not benefiting HCEs disproportionately and that the plan is providing meaningful benefits to all employees. The ADP test compares the average deferral percentage of HCEs to the average deferral percentage of NHCEs. The maximum allowable difference between these two averages is called the "permissible disparity" and is set by the IRS. To calculate the ADP, the average deferral percentage for both HCEs and NHCEs is calculated separately. The deferral percentage is calculated as the percentage of an employee's compensation that is contributed to the plan. The ADP is then determined by comparing the two averages and calculating the permissible disparity. If the difference between the two averages exceeds the permissible disparity, the plan sponsor must take corrective action, such as refunding excess contributions to HCEs or making additional contributions to NHCEs. The ACP test measures the average percentage of employer matching contributions or other non-elective contributions to the plan for both HCEs and NHCEs. This test is used to ensure that the plan is providing meaningful benefits to all employees and that HCEs are not receiving a disproportionate share of the plan's benefits. Like the ADP test, the ACP test also compares the average contribution percentage of HCEs to the average contribution percentage of NHCEs. To calculate the ACP, the average contribution percentage for both HCEs and NHCEs is calculated separately. The contribution percentage is calculated as the percentage of an employee's compensation that is contributed to the plan by the employer, such as matching contributions or profit-sharing contributions. The ACP is then determined by comparing the two averages and calculating the permissible disparity. If a plan fails the ADP or ACP test, highly compensated employees may be required to refund excess contributions that were made to their accounts. These refunds are known as Excess Deferral Contributions (EDCs). EDCs are subject to income tax and are generally refunded with earnings that are attributable to the excess contributions. In some cases, plan sponsors may be required to pay additional taxes or penalties if they fail to take corrective action to resolve excess contributions. In addition to EDCs, plan sponsors may also be required to make corrective distributions to non-highly compensated employees to help bring the plan back into compliance with ADP and ACP requirements. These corrective distributions may include additional matching contributions or other non-elective contributions. Corrective distributions are required to be made within a specified time period, and failure to make these distributions can result in significant tax penalties and lost benefits for plan participants. If a plan repeatedly fails to meet ADP and ACP compliance requirements, it may be at risk of disqualification. Plan disqualification can result in significant tax penalties and can cause plan participants to lose the tax benefits associated with their contributions. It is important for plan sponsors to take corrective action as soon as possible if their plan fails ADP or ACP tests to avoid these consequences and maintain a successful plan. One strategy for passing ADP and ACP tests is to increase contributions to highly compensated employees (HCEs). This may involve offering additional matching contributions or profit-sharing contributions to HCEs to help ensure that they do not receive a disproportionate share of the plan's benefits. However, this strategy may not be feasible for all plans, and plan sponsors should carefully consider the impact of any contribution increases on the plan's overall compliance. Another strategy for passing ADP and ACP tests is to implement a safe harbor 401(k) plan. Safe harbor plans are designed to automatically meet ADP and ACP compliance requirements, as long as certain contribution and vesting requirements are met. Safe harbor plans can be a good option for plan sponsors who want to simplify compliance requirements and ensure that their plans are providing meaningful benefits to all employees. Finally, plan sponsors may also consider offering non-elective contributions to non-highly compensated employees (NHCEs) to help increase their overall contribution percentage and bring the plan into compliance with ADP and ACP requirements. These non-elective contributions may include profit-sharing contributions, employer matching contributions, or other contributions that are not tied to employee deferrals. By offering these contributions, plan sponsors can help ensure that all employees are receiving meaningful benefits from the plan and avoid running afoul of ADP and ACP compliance requirements. It is important for plan sponsors to carefully consider the impact of any contribution increases or plan design changes on the plan's overall compliance and financial viability. By working closely with a qualified retirement plan advisor, plan sponsors can develop effective strategies for passing ADP and ACP tests and maintaining a successful 401(k) plan. Actual Deferral & Actual Contribution Percentage Test (ADP/ACP) is an annual compliance requirement for 401(k) plans to ensure that highly compensated employees do not receive disproportionate benefits from the plan. The Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) tests are critical for ensuring that 401(k) plans are fair and equitable for all employees. If a plan fails to meet ADP or ACP compliance requirements, plan sponsors may be required to refund excess contributions, make corrective distributions, or risk plan disqualification. Failing to comply with ADP/ACP tests can result in excess deferral contributions, corrective distributions, or even plan disqualification. Employers can pass the tests by increasing contributions to NHCEs, implementing a Safe Harbor 401(k) plan, or offering non-elective contributions to NHCEs. It is essential for employers to understand ADP/ACP tests and their compliance requirements to avoid penalties and maintain their 401(k) plan's eligibility.What Is an Actual Deferral & Actual Contribution Percentage Test (ADP/ACP)?

Actual Deferral Percentage Test (ADP)

Explanation of ADP

ADP Calculation

Actual Contribution Percentage Test (ACP)

Explanation of ACP

ACP Calculation

Consequences of Failing ADP/ACP Tests

Excess Deferral Contributions (EDCs)

Corrective Distributions

Plan Disqualification

Strategies for Passing ADP/ACP Tests

Increasing Contributions to Highly Compensated Employees (HCEs)

Implementing Safe Harbor 401(k) Plan

Offering Non-elective Contributions to Non-highly Compensated Employees (NHCEs)

Final Thoughts

Actual Deferral & Actual Contribution Percentage Test FAQs

ADP test ensures 401(k) plan contributions of highly compensated employees (HCEs) aren't too disproportionate compared to non-HCEs.

ACP test ensures that employer matching contributions, after-tax employee contributions and employee elective contributions made by highly compensated employees (HCEs) don't significantly exceed the contributions of non-highly compensated employees (NHCEs).

Employers must annually test the plan and may need to take corrective actions if the plan fails the tests.

If the plan fails the tests, the employer may need to return contributions to HCEs, issue refunds or make additional contributions to NHCEs, or risk plan disqualification.

Employers can pass the tests by increasing contributions to NHCEs, implementing a Safe Harbor 401(k) plan, or offering non-elective contributions to NHCEs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.