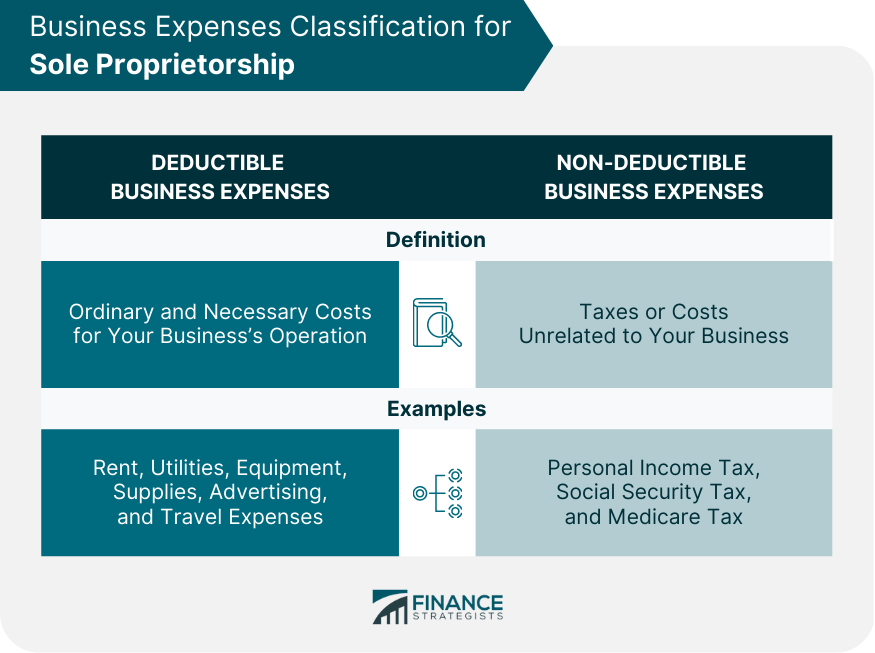

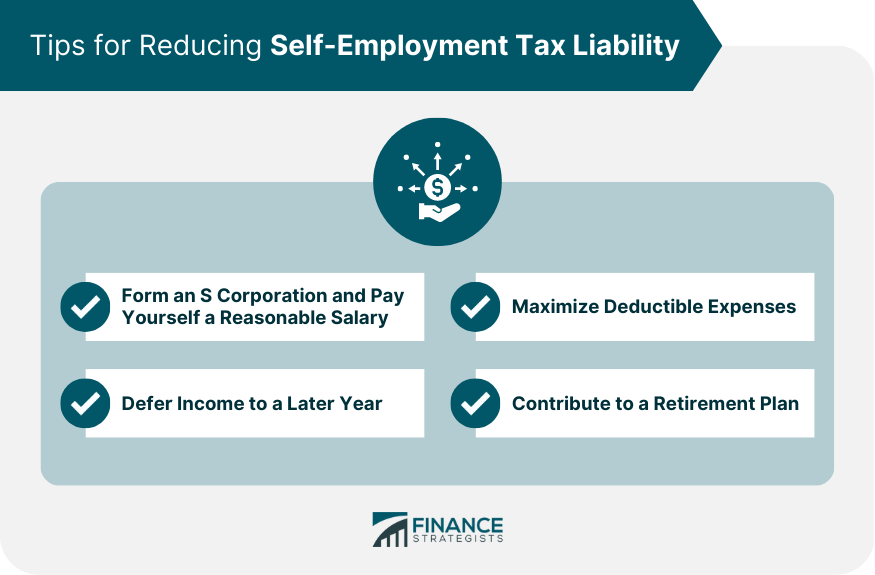

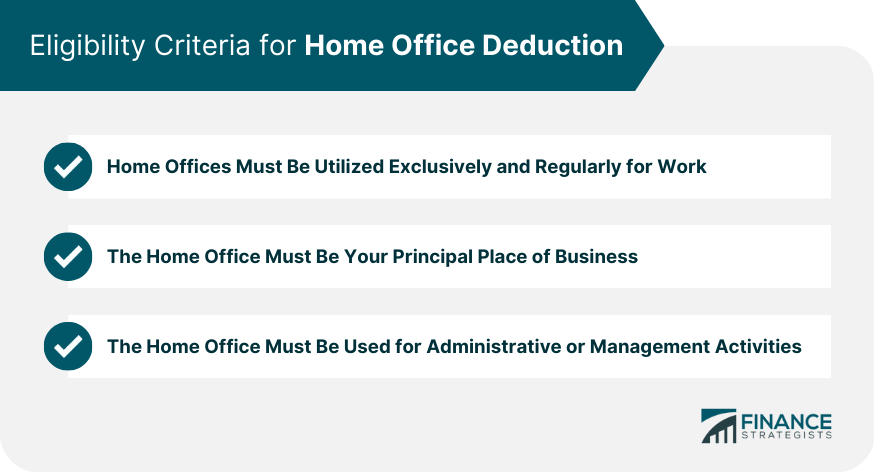

A sole proprietorship refers to a business structure where a single individual owns and manages the enterprise. This is the most straightforward and widely used form of business ownership, granting the owner full authority over all aspects of the company's functions and operations. Business debts, liabilities, and tax compliance are the sole responsibility of the owner. Understanding the tax requirements for sole proprietors is essential for avoiding costly penalties and staying compliant with the law. As a sole owner, you are in charge of all the costs of your business. But not all costs can be deducted from your taxes. Deductible business expenses are those that are ordinary and necessary for your business's operation. The costs that are typical and accepted in your industry are considered ordinary expenses. Essential expenses are those that are helpful and appropriate for your business. Examples of deductible business expenses for sole proprietors include rent, utilities, equipment, supplies, advertising, and travel expenses. However, personal expenses, such as clothing, entertainment, and personal fines, are not deductible. Non-deductible business expenses for sole proprietors include taxes unrelated to your business, such as personal income tax, social security tax, and Medicare tax. Additionally, lavish or extravagant expenses, such as first-class airfare, are not deductible. As a sole proprietor, you must be self-employed and pay self-employment and income taxes. Self-employment tax is equivalent to the combined employer and employee components of social security and Medicare levies. In 2024, the self-employment tax rate is at 15.3% on the first $168,600 net self-employment income. To calculate your self-employment tax, you must first determine your net self-employment income, which is your business's gross income minus your deductible expenses. Then you can apply the self-employment tax rate. You can use several strategies to reduce your self-employment tax liability as a sole proprietor. One option is to form an S corporation and pay yourself a reasonable salary. The salary is subject to payroll taxes, but profits beyond the salary are not subject to self-employment tax. Another option is to maximize your deductible expenses to reduce your net self-employment income. Additionally, you can defer income to a later year or contribute to a retirement plan to lower your taxable income. As a sole owner, you are not an employee, and your wages are not taxed. Instead, you are responsible for paying estimated quarterly taxes to the IRS regularly. Estimated quarterly taxes are prepayments of income and self-employment taxes based on your estimated income for the year. You must first estimate your income and expenses for the year to calculate your estimated quarterly taxes. You can use the previous year's tax return as a starting point and adjust your estimates for any expected changes. You can then use the IRS Form 1040-ES to calculate your estimated taxes and make payments electronically or by mail. There are four due dates for estimated quarterly taxes throughout the year: April 15th, June 15th, September 15th, and January 15th of the following year. It is important to note that the first payment for the current year is due on April 15th, even if you still need to file your tax return for the previous year. As a sole proprietor, keeping accurate records of your business's income and expenses is essential. Good record-keeping can help you track your business's profitability, prepare financial statements, and comply with tax laws. The types of records you should keep as a sole proprietor include bank statements, receipts, invoices, canceled checks, and credit card statements. You should also keep a log of your business mileage and any other travel expenses. Additionally, you should maintain a separate bank account and credit card for your business transactions to simplify record-keeping. You should keep your receipts and other documents organized and up-to-date to maintain accurate records. Use accounting software to help you track your income and expenses, generate financial reports, and prepare your tax returns. You should also back up your electronic records and keep a paper copy of important documents in case of a computer failure or other issues. If you operate your business out of your home, you may be eligible for a home office deduction. To claim this deduction, your home office must be used exclusively and regularly as your principal place of business or a place where you meet clients or customers. To be eligible for a home office deduction, you must meet the following criteria: You must use the home office exclusively and regularly for business purposes. The home office must be your principal place of business, a place where you meet clients or customers, or a separate structure on your property used for business purposes. The home office must be used for administrative or management activities, such as billing, record-keeping, or scheduling appointments. There are two methods for calculating the home office deduction: the simplified and regular methods. The simplified method allows you to deduct $5 per square foot of the home office up to a maximum of 300 square feet. The regular method requires you to calculate the expenses associated with your home office, including mortgage interest, property taxes, utilities, repairs, and depreciation. Several limitations and restrictions exist on the home office deduction for sole proprietors. For example, the deduction cannot exceed your business's annual net income. Additionally, you cannot claim a home office deduction if you are an employee who works from home for the convenience of your employer. As a sole proprietor, it is crucial to understand and comply with your tax obligations, including deductible expenses, self-employment tax, estimated quarterly taxes, record-keeping requirements, and home office deductions. Failing to do so to avoid costly penalties and legal issues. If you need help managing your business's finances and taxes, consider hiring a tax services expert and a financial advisor. These professionals can provide valuable guidance and support to help you navigate the complexities of tax laws and regulations, maximize your deductions, and minimize your tax liability. They can also help you develop a comprehensive financial plan for your business, ensuring its long-term success.Overview of Sole Proprietorship

Business Expenses

Self-Employment Tax

Estimated Quarterly Taxes

Record-Keeping

Types of Records Sole Proprietors Should Keep

Tips for Maintaining Accurate Records

Home Office Deduction

Eligibility Criteria for Home Office Deduction

Calculation of Home Office Deduction for Sole Proprietors

Limitations and Restrictions on Home Office Deduction

Conclusion

Sole Proprietorship Taxes FAQs

As a sole proprietorship, you manage your business's finances and comply with various tax obligations. These include deductible expenses, self-employment tax, estimated quarterly taxes, record-keeping requirements, and potentially a home office deduction.

As a sole proprietorship, you can deduct business expenses that are ordinary and necessary for your business's operation. These include rent, utilities, equipment, supplies, advertising, and travel expenses. However, expenses that are personal in nature or lavish and extravagant are not deductible.

You can use several strategies to reduce your self-employment tax liability, including forming an S corporation, maximizing your deductible expenses, deferring income to a later year, and contributing to a retirement plan.

Estimated quarterly taxes are prepayments of income and self-employment taxes based on your estimated income for the year. They are due four times a year: April 15th, June 15th, September 15th, and January 15th of the following year.

Hiring a financial advisor can help you navigate the complexities of tax laws and regulations, maximize your deductions, and minimize your tax liability. Additionally, a financial advisor can help you develop a comprehensive financial plan for your business, ensuring its long-term success.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.