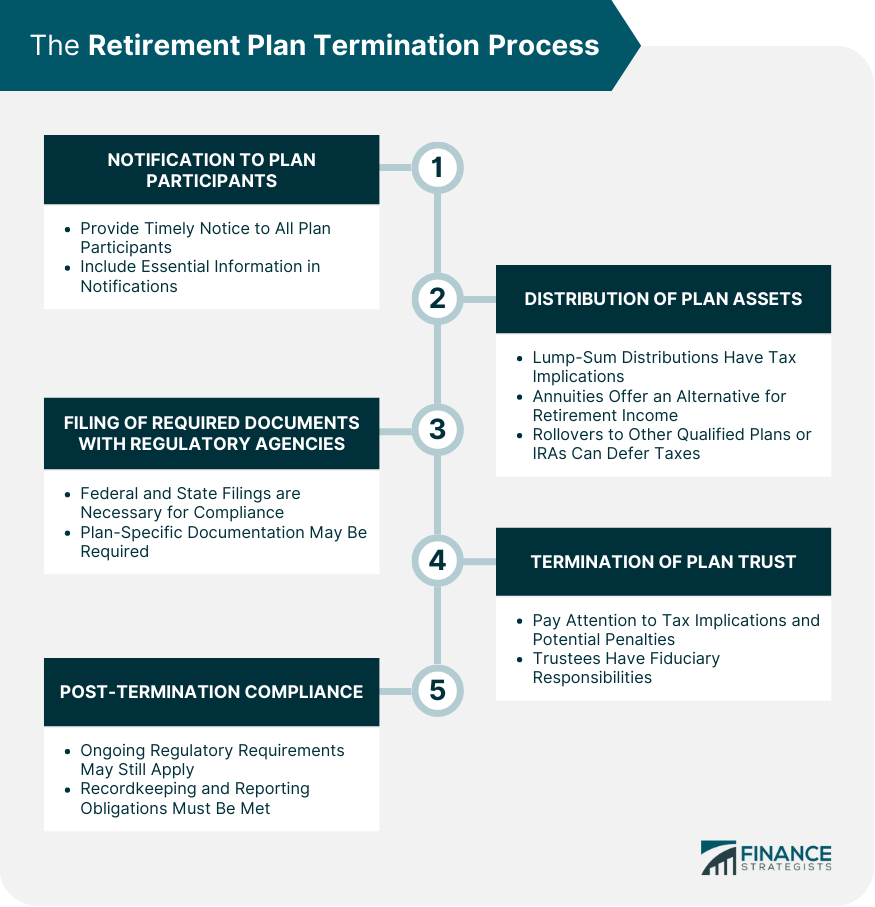

There are various reasons why an employer may decide to terminate a retirement plan, such as changes in company structure, financial difficulties, or shifting employee benefits priorities. Regardless of the reason, the termination process requires careful planning and compliance with legal and regulatory requirements. Retirement plans can be classified into two broad categories: defined benefit plans, which guarantee a specified monthly benefit at retirement, and defined contribution plans, where the benefit depends on the performance of the investment portfolio. Each type of plan has unique termination procedures, and understanding the differences is crucial for a smooth termination process. Terminating a retirement plan involves adhering to various legal and regulatory requirements, including notifying plan participants, distributing plan assets, filing required documents, and ensuring post-termination compliance. Employers must ensure they fully understand and follow these requirements to avoid potential legal issues and penalties. The process for terminating a retirement plan often involves notifying plan participants, distributing the plan assets, filing required documents with regulatory agencies, terminating the plan trust, and complying with the post-termination requirements. When terminating a retirement plan, it is important to provide timely notice to all plan participants. This ensures that employees are aware of their rights and options and have sufficient time to make decisions regarding their retirement benefits. The notification process may differ based on plan type and specific regulations. Notifications must include essential information such as the reason for termination, the date of termination, and the options available to plan participants for receiving their benefits. Providing accurate and comprehensive information helps participants make informed decisions and reduces the likelihood of confusion or disputes. The notification process for terminating a defined benefit plan differs from that of a defined contribution plan. For example, defined benefit plans may require additional steps, such as determining the plan's funded status and obtaining regulatory approvals. It is crucial for employers to understand these differences and tailor their communications accordingly. When a retirement plan is terminated, participants may be eligible to receive a lump-sum distribution of their benefits. However, the tax implications of such distributions can be significant. Participants must be informed of their eligibility and the potential tax consequences to make well-informed decisions. Participants who choose to receive a lump-sum distribution must follow specific procedures, which include submitting a request to the plan administrator and providing necessary documentation. The plan administrator must then process the request and distribute the funds according to applicable regulations and deadlines. Lump-sum distributions can be subject to penalties and fees, such as early withdrawal penalties and mandatory tax withholding. It is important for plan participants to understand these potential costs and weigh them against the benefits of receiving a lump-sum distribution. An alternative to lump-sum distributions is purchasing an annuity, which provides a steady stream of income during retirement. Participants must carefully select an annuity provider, taking into consideration factors such as financial stability, reputation, and the range of available annuity products. Annuities come in various forms, such as fixed, variable, and indexed annuities, each with unique features and benefits. Participants should carefully evaluate their options and choose an annuity product that best aligns with their retirement goals and risk tolerance. Annuity purchases have tax implications, including potential tax-deferred growth and the treatment of annuity payments as ordinary income. It is crucial for participants to understand these tax implications and consult with a tax professional if necessary. Rollovers to other qualified plans or IRAs can help participants defer taxes on their retirement savings. However, rollovers must be completed within specific deadlines, usually 60 days from the date of distribution, to avoid taxes and penalties. Understanding the tax implications and deadlines is crucial for plan participants considering a rollover. To initiate a rollover, participants must follow specific procedures, such as contacting their plan administrator and completing the required paperwork. The plan administrator will then transfer the funds directly to the new plan or IRA (direct rollover) or issue a check to the participant, who is responsible for depositing the funds into the new account (indirect rollover). Terminating a retirement plan involves filing required documents with federal and state regulatory agencies, such as the Internal Revenue Service (IRS) and the Department of Labor (DOL). These filings ensure compliance with applicable laws and regulations and provide necessary information for oversight and enforcement purposes. Specific reporting requirements and deadlines apply to retirement plan terminations, depending on the plan type and jurisdiction. Failure to comply with these requirements can result in penalties and other adverse consequences. Employers must be diligent in understanding and meeting their reporting obligations during the termination process. Terminating a retirement plan may require submitting various plan-specific documents, such as plan termination forms, trust agreements, and actuarial reports (for defined benefit plans). These documents provide essential information about the plan's financial status, participant benefits, and compliance with applicable laws and regulations. Upon plan termination, the plan trust must also be legally terminated. This involves dissolving the trust according to the terms of the trust agreement and applicable laws. Employers and trustees should consult with legal counsel to ensure proper handling of the termination process. Terminating a plan trust may have tax implications, including potential taxes on trust assets and penalties for non-compliance with tax laws. It is essential for employers and trustees to understand these implications and work with tax professionals to minimize adverse consequences. Trustees play a critical role in the termination of a plan trust, including distributing plan assets, filing required documents, and ensuring compliance with applicable laws and regulations. Trustees must fulfill their fiduciary responsibilities and act in the best interests of plan participants throughout the termination process. Even after the termination of a retirement plan, certain ongoing regulatory requirements may still apply, such as maintaining records and submitting reports to regulatory agencies. Employers must remain vigilant in their compliance efforts to avoid potential issues and penalties. Maintaining accurate and up-to-date records is crucial after a plan termination, as regulatory agencies may request documentation to verify compliance with applicable laws and regulations. Employers must continue to meet their recordkeeping and reporting obligations, even after the plan has been terminated. Retirement plan terminations may be subject to audits and enforcement actions by regulatory agencies, such as the IRS and DOL. Employers must be prepared to demonstrate their compliance with applicable laws and regulations and address any potential issues identified during an audit or enforcement action. Retirement plan termination is a complex process that requires careful planning and execution. Employers must understand and comply with applicable laws and regulations, communicate effectively with plan participants, and ensure a smooth distribution of plan assets. Proper planning and execution can help minimize disruptions and protect the interests of both the employer and plan participants. The termination process can present various challenges and pitfalls, such as potential tax consequences, legal compliance issues, and communication difficulties with plan participants. Employers must be prepared to address these challenges and navigate the complexities of the termination process to achieve a successful outcome. Given the complexities involved in the retirement plan termination process, employers and plan participants are encouraged to seek the guidance of professional retirement planning services.Retirement Plan Termination Process

Step 1 Notification to Plan Participants

Timing of Notifications

Required Information in Notifications

Special Considerations for Different Types of Plans

Step 2 Distribution of Plan Assets

Lump-Sum Distributions

Eligibility and Tax Implications

Process for Requesting and Receiving Lump-Sum Distributions

Potential Penalties and Fees

Annuity Purchases

Selecting an Annuity Provider

Types of Annuities and Their Features

Tax Implications and Considerations

Rollovers to Other Qualified Plans or IRAs

Tax Implications and Deadlines

Process for Initiating a Rollover

Step 3 Filing of Required Documents with Regulatory Agencies

Federal and State Filings

Reporting Requirements and Deadlines

Plan-Specific Documentation

Step 4 Termination of Plan Trust

Legal Process for Terminating the Trust

Tax Implications and Potential Penalties

Trustee Responsibilities and Requirements

Step 5 Post-Termination Compliance

Ongoing Regulatory Requirements

Recordkeeping and Reporting Obligations

Potential Audits and Enforcement Actions

Final Thoughts

Plan Termination Process FAQs

Before initiating the retirement plan termination process, you should consider factors such as the reasons for termination, the type of retirement plan, and the legal and regulatory requirements involved. It is essential to carefully plan and execute the process while ensuring compliance with all applicable laws and regulations.

Effective communication is crucial during the retirement plan termination process. You must provide timely and accurate notifications to plan participants, including information on the reason for termination, the date of termination, and the available options for receiving their benefits. Tailor your communication based on the type of plan being terminated.

During the retirement plan termination process, you should distribute plan assets through lump-sum distributions, annuity purchases, or rollovers to other qualified plans or IRAs. Ensure plan participants understand the eligibility, tax implications, and potential penalties associated with each option to make informed decisions.

In the retirement plan termination process, you must file required documents with federal and state regulatory agencies, such as the Internal Revenue Service (IRS) and the Department of Labor (DOL). This includes meeting specific reporting requirements and deadlines, as well as submitting plan-specific documentation like plan termination forms and trust agreements.

To ensure post-termination compliance, you should continue to meet ongoing regulatory requirements, maintain accurate records, and fulfill your reporting obligations even after the retirement plan has been terminated. Be prepared for potential audits and enforcement actions by demonstrating compliance with applicable laws and regulations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.