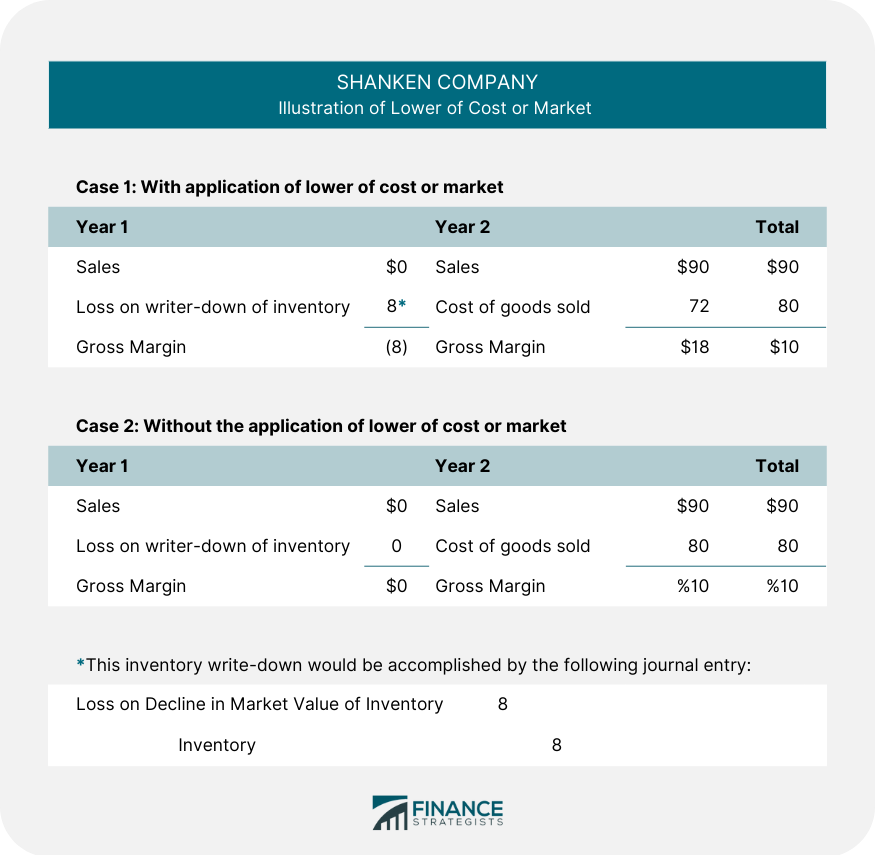

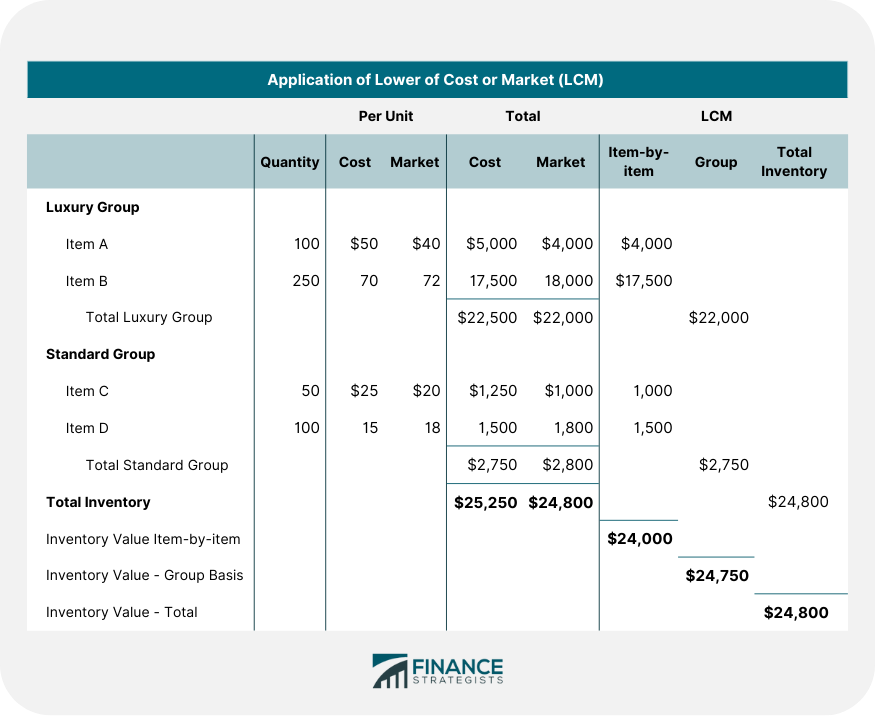

Lower of cost or market is a method of inventory pricing by which the inventory is priced at cost or market, whichever is lower. It is an application of conservatism in accounting. Under generally accepted accounting principles (GAAP), the presumption is that inventories will be recorded at cost. Although this is a violation of the historical cost principle, accountants feel that losses should be recorded as soon as they become evident. thus, in this case, the concept of conservatism takes precedence over historical cost convention. Approximately 90% of the 600 companies surveyed by the AICPA in 2019 reported their inventory at the lower of cost or market. In applying the lower of cost or market rule, cost is determined by one of the cost flow methods; market, in this case, generally means replacement cost, or the cost to purchase a similar inventory item. The use of lower of cost or market is based on the theory that if an item’s replacement cost decreases in the current period, its sales price will ultimately decrease. Because accountants feel that all losses should be recognized when they occur, this loss is recognized in the period that it occurs – that is, when the price declines – not in a later period – when the item is eventually sold. To illustrate the theory behind the LCM rule, assume the following facts: The analysis in the above example shows the effect on reported earnings over a two-year period, both with and without the application of lower of cost or market rule. This example assumes that when replacement cost dropped 10%, or $8 from $80 to $72, there was a corresponding decrease of 10%, or $10 from $100 to $90, in the item’s selling price. Case 1 shows the effect of applying the LCM rule. In year 1, there is a reported loss of $8 due to the decline in the replacement cost. In year 2, when the actual sale takes place, there is an $18 gross margin on sales. This $18 gross margin represents a 20% gross margin percentage, the normal gross margin percentage that the Shanken Company earns. The result of applying the lower of cost or market is to force the company to take a loss in year 1, the year of the price decline, but it allows the company to earn its normal gross margin percentage in future years. Over the 2-year period, the combined income is $10. Case 2 shows the effect of not applying the lower of cost or market rule. There is no income or loss in year 1; the entire effect is felt in year 2 when the sale takes place. In year 2, the gross margin falls to $10, and the gross margin percentage falls to 11%. Over a 2-year period, the combined income is 410, the same as it is in Case 1. Thus, the application of lower of cost or market changes the allocation of income within the 2-year period but does not change the combined income. This illustration is based on the assumption that a decrease in the replacement cost of the item will result in a corresponding decrease in the sales price. However, in reality, that one-for-one relationship does not always hold. For example, assume that although the replacement cost of the inventory item held by the Shanken Company drops 10%, there is little or no change in the sales price. To apply the lower of cost or market in this situation would understate income in year 1 and overstate income in year 2 and would be the improper application of conservatism. Thus, lower of cost or market must be applied with caution. The application of lower of cost or market is a two-step process. In the first step, market, defined as the item’s replacement cost, is determined. This can usually be done by examining vendors’ invoices at the end of the year. In the second step, market or replacement cost is compared with cost, and if necessary, the inventory is reduced to the lower of cost or market (LCM). Under generally accepted accounting principles, the comparison can be made on (1) an item-by-item basis, (2) a group-of-items basis, or (3) the inventory as a whole. The LCM comparison on all three bases is shown in the below example. When the item-by-item basis is used, individual comparison for all items must be made. This results in an inventory value of $24,000. Under the group basis, the inventory is divided into a luxury group and a standard group, and the comparison is then made for each group total. For example, in the luxury group the cost of $22,500 is compared with the market of $22,000, and so the value of the group is determined to be $22,000. The same comparison is then made for the standard group, and its value is $2,750. This results in a total inventory value of $24,750. On a total-inventory basis, the cost and the market of the entire inventory are compared, resulting in an inventory value of $24,800. Comparing all three methods, we see that the item-by-item method is the most conservative; that is, it results in the lowest inventory value. This is because increases in the value of one item cannot offset decreases in other items, as is the case under the group and total inventory methods. The Internal Revenue Code contains specific regulations pertaining to the use of lower of cost or market for federal tax purposes. First, for tax purposes, only FIFO (no LIFO) can be used in conjunction with lower of cost or market. For generally accepted accounting (GAAP) purposes, however, LIFO combined with lower of cost or market is a valid method. Second, for tax purposes, lower of cost or market can be applied only on an item-by-item basis. The group or total inventory method cannot be used.What Is Meant by Lower of Cost or Market?

Explanation

If however, the utility of the goods in the inventory is not as great as their cost is, the goods must be written down to the lower of cost or market.The Theory of Lower of Cost or Market (LCM)

Example

The Application of Lower of Cost or Market

Lower of Cost and Market and Income Taxes

Two of these provisions differentiate the use of lower of cost or market for tax purposes from financial reporting purposes.

Lower of Cost or Market (LCM) Theory FAQs

The Lower of Cost or Market (LCM) Theory is an accounting model that states when determining the value of a product for financial reporting purposes, it should be recorded at either cost or market price, whichever is lower.

Companies use the LCM theory in order to ensure accurate and reliable financial statements by preventing the overstatement of assets. This prevents organizations from misrepresenting their true financial state.

LCM requires companies to record each inventory item at its current market value, or its original cost if it is lower than the market value. This ensures that inventory items are not overvalued and all financial statements are accurate.

An example of LCM Theory in action would be an organization recording the cost of an item at $10 when the current market price for that item is only $5. In this case, according to LCM theory, the inventory should be recorded at $5 instead of $10 for accurate reporting.

Generally, LCM Theory must be applied whenever determining the value of an asset unless there is evidence to suggest that the asset will be sold at a higher price in the future. In this case, the higher price may be used instead. However, it is important to note that this exception should only be used if there is reliable evidence to support it.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.