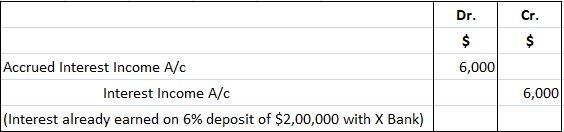

The term accrued revenue, also known as accrued income, refers to revenue or income for which no cash payment has been received before the end of the period in which the income or revenue in question has been earned. If an income or revenue remains uncollected and no entry is made in the books of accounts for any reason, an adjusting entry is required at the end of the accounting period. This requirement is imposed by the accrual principle. This states that the revenues/incomes and expenses must be brought into account in the accounting period in which they are earned or incurred, regardless of their receipt or payment. Accrued revenues are revenues received for services completed or goods delivered that have not been recorded. This necessitates adjusting entries and the inclusion of items such as interest revenue and rental revenue. Along with the profit made on trading activities, a business may occasionally have other sources of income, including rental income, commission income, interest income, and so on. Similar to expenses, most businesses record their incomes only after they have been received in cash. Therefore, it is possible that at the end of a financial year, a business may have rendered a service without yet receiving payment. The trial balance may fail to disclose this accrued revenue or income unless a suitable adjustment is made. Accrued revenues include items such as interest revenue, rental revenue, and investment revenue. Adjusting entries must be made for these items in order to recognize revenue in the accounting period in which it is earned. This is despite the fact that the receipt of cash may take place in the future. Revenues from these items occur continuously, but to simplify the process, they are recorded only once at the end of the accounting period. This involves recognizing an accrued receivable and a corresponding revenue item. A firm may have other accrued revenues that require adjusting entries. For example, a company may earn commission on the sale of a building in the current accounting period for which it won't receive payment until the next period. In this case, an adjusting entry must be made at the end of the current period in order to accrue the commission earned but not yet received. Consider the example of John, a wholesaler who deposits $200,000 at 6% interest on 1 July 2019 in his bank for a 12-month period. John will, therefore, receive his principal, $200,000, and interest in July 2020. When he draws up his Trial Balance on 31 December 2019, it may not show any record of the interest earned by that date. This is simply because John has not yet received it in cash. But the fact remains that John has already earned interest for 6 months by 31 December 2019. It should be reflected in his profit and loss account for 2019. Another important fact is that while John's trial balance doesn't disclose it, John has acquired a current asset in the form of accrued interest income of $6,000 (6/12ths of 6% on $200,000) on 31 December 2019. This accrued interest must be shown on John's balance sheet on that date. The journal entry needed to account for accrued income is: In this case, the debit and credit entries are made for the amount of income already earned. In John's case, the journal entry for accrued revenue or income is shown below. In the case of accrued revenue: In the case of accrued income: The Fine Repairing Company provided repair services for $5,000 to Monster Company on 25 December 2016. The Monster Company promises to pay the service fee on 15 January 2017. No service revenue has been recorded by the Fine Repairing Company until the end of its accounting period, which is on 31 December 2016. Make an adjusting entry for this accrued revenue item in the books of Fine Repairing Company on 31 December 2016. Small Company makes an investment of $40,000 in Big Company on 1 July 2016. The investment earns 10% interest per anum. Small Company neither receives nor records any interest income relating to this investment until the end of its accounting period, which is on 31 December 2016. Make an adjusting entry in the books of Small Company for this accrued interest item. Note: Interest for 6 months (from 1 July to 31 December) = ($40,000 × 0.1) × 6/12 = $2,000Accrued Revenue or Accrued Income: Definition

Accrued Revenue: Explanation

Example

Journal Entry for Accrued Income/Revenue

Adjusting Entry for Accrued Income/Revenue

Example 1

Solution

Example 2

Solution

Accrued Revenue or Accrued Income FAQs

Accrued revenues are recorded as receivables on the balance sheet to reflect money that customers owe for goods or services they purchased. Accrual revenue may be contrasted with realized and recognized, which means it's not available right away but will come in later when you make sure everything has been paid back plus any interest owed.

Accrued revenue needs to be recognized because it is a measure of increasing income. Income can be made use of only when earned and not just expected. However, the actual earning takes time compared to receipt of an amount that occurs almost instantly.

The reasons for recognizing accrued interest are similar to those of revenue. Interest is calculated on the basis of a certain rate per period and it would be erroneous not to recognize interest which has been earned but not yet recorded.

The journal entry for recording accrued interest shows a credit balance in the account 'Interest Receivable'. There may be a debit entry to the account 'Interest Revenue' and the credit balance in the 'Interest Receivable' account may be transferred to that account.

The journal entry for recording accrued revenue and accrued interest would show both of them as credits with equal values on each side of the account.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.