Contract costing is the method of costing applied in a business where separate contracts of a non-repetitive nature are undertaken. According to Sharie, “contract or terminal cost accounts are applicable to a concern which makes specific contracts and requires to know the cost of each.” A contract is a job of a large size that may extend beyond one accounting period. The person executing the contract is known as a contractor, and the person for whom it is executed is known as the contractee. Contract costing is a form of job costing involving big jobs that require a considerable amount of time to complete and comprise numerous activities. A separate account is opened for each contract in the contract ledger or the general ledger. The account is debited with all direct and indirect expenses and credited with the contract price on completion. The balance of this account is transferred to a profit and loss account. However, if the contract is not completed before the end of the accounting period, a reasonable amount of profit (or logs) is transferred to a profit and loss account. For materials, three specific forms of accounting may need to be performed. In case materials are purchased for the contract and directly delivered to the site of the contract, there arises no specific accounting system. However, if the materials purchased are first delivered to the store’s department, the contract account will be debited and the store control account will be credited. If, however, certain materials are charged to the contract account but returned to stores, the store's contract account will be debited and the contract account credited. Materials sold at the contract site are credited to the contract account. However, if a sale is made, the resulting profit or loss is credited to the profit and loss account. In case of a sale of contract assets and property for profit or loss, the profit and loss account is credited. In some cases, the contractor may supply the materials to the contractee. Here, the value of such materials should not be charged to the contract account. The unused materials are to be returned to the contractor. All labor used to complete the contract is direct labor and treated as such. The wages abstract is prepared to maintain a proper record and retain control over the labor expenses. If a plant, machinery, or equipment is specially purchased for a particular contract and will be exhausted at the site, it will naturally be debited in the contract account and any amount of depreciation shall be charged to the credit side of the contract account. However, if it is acquired for a shorter period, the amount is only debited with the usual depreciation of the assets. Any sale proceeds at the midway point of a contract or upon completion are credited to the contract account, and profit or loss on such a sale is transferred to the profit and loss account. Indirect expenses are treated and apportioned in the same manner as any costing system. If on three contracts, Nos. 1, 2, and 3, $3,000, $2,000, and $1,000 are spent, respectively, on materials, labor, and plant, and if indirect expenses are $1,200, the share in indirect expenses of contract Nos. 1, 2, and 3 will be $600, $400, and $200 at the ratio of 3 : 2 : 1, respectively. The cost-plus contract involves the contractee agreeing to pay the contractor the cost price of the work carried out on the contract plus an agreed amount or percentage thereof by way of different overheads and profit. An agreement may be in place to charge extra money for any addition(s) or alteration(s) to work originally agreed to be carried out under a particular contract. In such a case, the extra money becomes payable to the contractor by the contractee for all subsequent additions and alterations. The contractor (if allowed to do so by the agreement entered into) may entrust a portion of the work to one or more than one sub-contractor(s). The cost in this connection is the direct charge on the contract and is treated as such in the contract costing. A contract agreement usually makes a provision for the escalation clause: the contractor is interested in being safeguarded against any charge in the price level. The agreement specifies the procedure for the calculation of adjustment in order to avoid all disputes. In the case of small contracts, the usual practice is to make the payment to the contractor in a lump sum upon completion. However, in a large contract, the payment is made in installments on the basis of progress made. Progress is judged by technical personnel, such as architects, surveyors, and engineers. Such personnel issue a certificate for the complete work, otherwise known as work certified, which may be expressed in terms of percentage. Here, the contractor may not pay for 100% work certification and may withhold or retain payment. This is called retention money. The work for which certification is not granted is known as work uncertified. The following are the ways the value of work certified is treated in cost accounts: OR ALTERNATIVELY If the contract is not complete and the accounting year has come to a close, then the profit on incomplete contracts is required to be calculated and accounted for. In this respect, the following rules may be followed: The main features of contract costing may be summarized as follows: Contract costing is most suitable for ship-building, road construction, building construction, civil engineering works, and the like. Contract costing, job costing, and terminal costing do not differ so far as the nature of the work involved is concerned. However, contract costing differs from job costing because a contract is executed at the site outside the factory premises of the contractor, whereas a job is executed by the contractor inside the factory premises. Moreover, ascertaining the cost of a contract is simple in contrast to ascertaining the cost of a job. A contract is executed at the site of the contract outside the factory premises, and, as such, most of the expenses incurred by the contractor in the execution are direct in nature. A job is performed inside the factory premises and involves the simultaneous completion of different jobs; indirect expenses have to be apportioned to these jobs on an equitable basis. Contract costing and job costing differ slightly from terminal costing because terminal costing involves a deadline fixed by the contractee within which a job or contract must be completed. In case of a missed deadline, the contractor shall pay damages to the contractee on account of loss suffered due to the delay in the completion of the job or contract. The main objectives of contract costing are: A contractor maintains a contract ledger in which a separate account is opened for each contract they undertake. The contract ledger should be ruled out so as to provide maximum information. A specimen ruling of the contract ledger is given below: Contract Costing: Definition

Contract Costing: Explanation

Specific Aspects of Contract Costing

Materials

Labor

Plant and Machinery

Indirect Expenses

Cost-Plus Contract

Extras

Sub-Contracts

Escalation Clause

Payment

Profit on Incomplete Contracts

By deducting the total estimated cost from the agreed total contract price and the profit and loss account before being credited by the proportion of total estimated profit vis-à-vis cash received from the contractee.Features of Contract Costing

Difference Between Contract Costing, Job Costing, and Terminal Costing

Objectives of Contract Costing

Procedure of Contract Costing

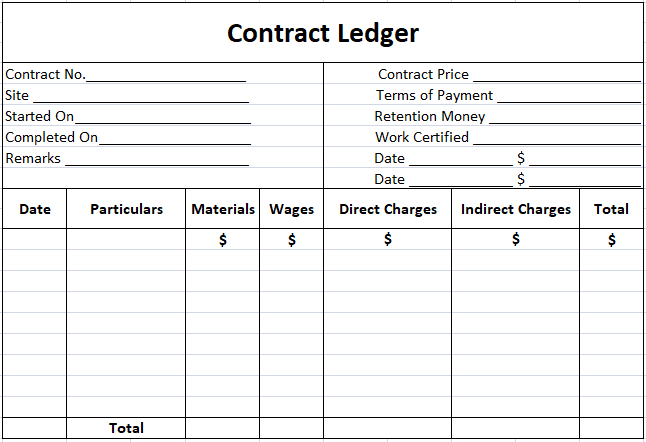

Contract Ledger

Contract Costing FAQs

Contract costing is the method of costing applied in a business where separate contracts of a non-repetitive nature are undertaken.

The person executing the contract is known as a contractor, and the person for whom it is executed is known as the contractee.

All labor used to complete the contract is direct labor and treated as such. The wages abstract is prepared to maintain a proper record and retain control over the labor expenses.

Indirect expenses are treated and apportioned in the same manner as any costing system.

A contract agreement usually makes a provision for the escalation clause: the contractor is interested in being safeguarded against any charge in the price level. The agreement specifies the procedure for the calculation of adjustment in order to avoid all disputes.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.