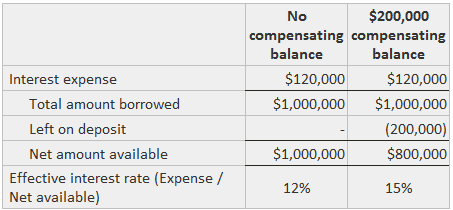

Generally Accepted Accounting Principles (GAAP) call for the presentation of information about restricted cash balance. These restrictions may include amounts set aside in escrow accounts, which can be used only for a specified purpose. These amounts should be excluded from cash and from current assets if appropriate. There may be informal restricted cash arising from management's intention of using a certain amount of cash for a particular purpose. This type of restriction rarely produces formal segregation on the balance sheet because of its non-binding nature. If the amount is material, special footnote disclosure may be justified. A major restriction may be placed on cash by a bank in connection with a loan or a commitment to a loan (known as a line of credit). Specifically, the depositor must leave a stated amount on deposit in an account (either checking or savings). These compensating balances result in the borrower paying a higher effective interest rate because the bank has the use of the money. For example, suppose that Sample Company has two separate loans of $1,000,000 bearing interest at 12 percent. One has no compensating balance requirement, but the other calls for $200,000 to be left on deposit at all times. The analysis below shows how the effective interest rate is affected. Disclosures about compensating balances have not been addressed in any authoritative pronouncements. This publication from GAAP (which is binding for SEC filings) requires that an enforceable compensating balance agreement be disclosed by segregating the amount from cash if it is greater than 15% of total cash and marketable investments. The same disclosure is required if the impact on the effective interest rate is "significant." If the arrangement is not enforceable, not more than 15% of cash and marketable investments, or does not have a significant effect on the effective interest rate, then disclosure is appropriate. The GAAP does not require disclosure of the effective interest rate. From a practical standpoint, formal segregation seldom occurs because the agreements are virtually always informal and non-binding. Thus, their existence is generally disclosed in a footnote. Presented below is a note written by Dan River, Inc. to describe its compensating balances: In 2018, the average compensating balance needed amounted to $4,354,000, while the amount required on 30 December 1978 was $4,008,000 after adjustment for estimated average float. The average amount of outstanding loans amounted to $9,461,000, and the maximum amount outstanding at the end of any month was $16,631,000. The unused available borrowings under the lines of credit agreements amounted to $58,150,000 on 30 December 1978. The weighted average interest rate on the short-term bank loans during the year amounted to 8.59%. Notice that the arrangement lacks legal enforceability.Compensating Balances

Note 2: Compensating Balances—Informal lines of credit agreements with several banks require the Company to maintain average cash compensating balances principally equal to 20% of the average outstanding short-term bank loans or 10% of the amount of the credit line, whichever is higher.

The agreements require interest on the loans at the prime rate and are subject to review from time to time and can be terminated at the option of either party.

Restricted Cash FAQs

Yes, but not at the rate that is customary for demand deposits. There may be informal restrictions that do not produce formal segregation and require no special disclosure (if they result in increased effective rates). However, if the amounts are material and restraints significant, then additional footnote disclosure is required.

Compensating balances should be segregated from unrestricted cash. If the compensating balance is not legally enforceable (the creditor can terminate it at will), then footnote disclosure is required (like any other non-enforceable agreement). The volume and dollar amounts of compensating balances are, by themselves, immaterial and require no additional footnote disclosure (if they result in increased effective rates).

Restricted cash may be counted as collateral if both the cash balance is segregated and it has some level of enforceability. If the arrangement is not enforceable, then no additional footnote disclosure is required (if they result in increased effective rates).

No. All disclosure of non-enforceable formal restrictions on cash balances is required, regardless of their amount.

Yes. If there are significant formal restrictions on cash balances, including compensating balance arrangements that do not meet the legal enforceability criteria, the rate of interest would need to be disclosed.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.