The treatment of small stock dividends differs from the treatment of splits effected as dividends. This is because they serve fundamentally different purposes. A small stock dividend is treated as if it is a cash dividend reinvested in capital stock. Consequently, Retained Earnings should be debited for the market value of the stock. The credits should be recorded in Capital Stock and Capital in Excess of Par. The Committee on Accounting Procedures justifies the use of this approach on the grounds that the dividend is perceived as a reinvestment. While specifying that the market value should be used, there is no specification regarding the day (declaration or distribution) on which the market value is to be measured. It seems reasonable to think that the declaration date is more appropriate: namely, because the information available on that date was used by the board when its members were deciding on whether to declare the dividend. Up to this point, the discussion has focused on small stock dividends, which range from 20% to 25%. Occasionally, a corporation will issue a large stock dividend. The accounting profession defines a large stock dividend as one in excess of 20% to 25%. Some stock dividends are as large as 100%. These have the effect of proportionately reducing the market price of the corporation's stock. Large stock dividends are recorded by debiting Retained Earnings and crediting Common Stock for the total par value of the stock issued by the stock dividend. The market value of the stock is ignored. Accountants must be able to identify whether a particular stock dividend is small or large. The key factor cited by the Committee on Accounting Procedures is the management's intent. If the objective of the board of directors was to produce a stimulation of market activity, the dividend should be accounted for as a large dividend. While this test may be theoretically sound, it depends on subjective evidence. In recognition of this weakness, the accountant examines the dividend's effect on the stock's market value. That is to say, if the value apparently drops because the dividend is declared, then it should be considered large. However, this test also relies on potentially inadequate evidence in the sense that the accountant simply may not be able to determine whether it was the dividend or other factors that caused the price to change. Consequently, the committee established a third test that depends on the size of the dividend compared to the number of shares outstanding prior to its declaration. While the percentage size can be easily and objectively calculated, the committee did not establish a specific dividing point between small and large. Perhaps because this imprecise guideline left an unsatisfactorily high degree of judgment in the test, the SEC issued the Accounting Series Release. This pronouncement holds that all dividends less than or equal to 25 percent are small and all others are large. Even though the SEC rule technically applies only to firms under the commission's jurisdiction, it appears to have been very influential in establishing generally accepted practice. This example shows a disclosure from Checker Motors Corporation related to the declaration and payment of a small stock dividend. In February 2019, the board of directors approved a 2-for-1 split of the company's common stock in the form of a 100% stock dividend. To effect this stock split, the stockholders approved an increase in the authorized common stock from 10,000,000 to 25,000,000 shares. All references to per share data and stock option data have been adjusted to reflect this stock split.What Are Small Stock Dividends?

Large Versus Small Stock Dividends

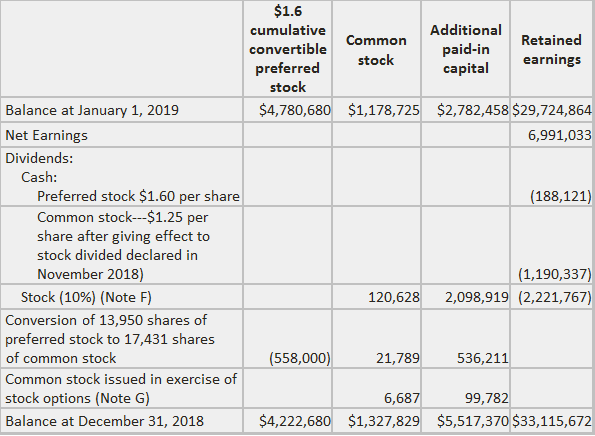

Identifying Small and Large Stock Dividends

Example: How to Pay Small Stock Dividends

Small Stock Dividends FAQs

A stock dividend or bonus issue is an increase in the number of outstanding shares of a corporation. A shareholder with 100 shares will now have 200, since he has received one bonus share for every 100 he already held. The market value per share should not be affected by this event.

Stock dividends are accounts on the books of companies that issue them. They do not result in immediate income but rather as an increase in shareholders' equity. Companies may pay cash dividends to distribute profits, or they may give shareholders additional shares as a sort of "bonus" for investing in the company. When this happens, the shareholder's equity increases in proportion to the number of shares.

When a company declares a small stock dividend, it issues additional shares to its holders without paying cash dividends. The Bookkeeping entry for this transaction is one debit, which increases Retained Earnings by increasing common stock. Retained Earnings show the total amount of income that a company has earned and not paid to its shareholders as dividends.

Since there are no guidelines for determining what percentage of a Stock Split is "small" and what percentage is "large," the test used by the Securities and Exchange Commission (SEC) and most companies with common stocks on file is based on the amount of dividends. The SEC, which regulates public offerings of corporate stocks, has ruled that a dividend is "small" if it represents less than 10% of the market price of the stock before the dividend announcement.

The board of directors of every company issues small stock dividends, although in some cases they are approved by shareholders at large. This happens most often when a company has more cash than it needs or when its stock is trading at a rather high price.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.