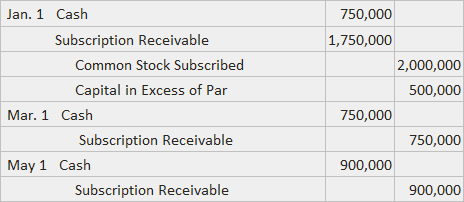

Additional paid-in capital (APIC) is the amount invested in a corporation by its owners, in addition to the par value of any capital stock. Stockholders may have claims against the corporation arising from payments into the company from events other than operations or the issuance of stock. While the most precise approach would identify the specific origin of the claims, immateriality usually results in their being grouped into a single Additional Paid-In Capital or Capital in Excess of par account. The paragraphs below describe several examples of events that create this type of claim. In the event that a subscriber to stock fails to pay in the full amount promised and the corporation is allowed to keep some or all of the cash paid in prior to the default, additional paid-in capital is created to the extent of the unrefunded amount. To illustrate, consider Sample Company's situation shown below and assume further that a subscriber to 10,000 shares defaults on 1 May. If 90,000 shares are issued to the paid-up subscribers, this entry would be made: At this point, the account associated with the default has the following balances: Furthermore, the corporation has accepted $150,000 in cash from subscribers. If the full amount is refunded on 15 May, this entry would be made: A more likely situation would call for the corporation to keep part of the cash in order to recover its costs. Suppose that Sample Company is allowed by the agreement to keep 30% of the cash. The following entry would be made when the defaulted subscriber is refunded $105,000, or 70% of the $150,000 paid in: The $45,000 of additional paid-in capital (30%of $150,000) represents claims held by the non-defaulting stockholders. A firm may accept a donated asset from a local government agency. The most common practice for recognizing the increase in stockholders' equity calls for a credit to Additional Paid-In Capital. If Sample Company accepts a plot of land worth $850,000 as a donation, the following entry would be made: If the amount of capital created by this action is material, a more descriptive title might be used, such as Paid-In-Capital—Donated Assets, and the account balance would be separately disclosed. Whatever name you decide to use, it should be remembered that the account describes the claims held by the stockholders that arose from the acceptance of the assets.What Is Additional Paid-In Capital (APIC)?

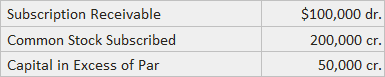

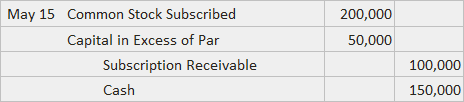

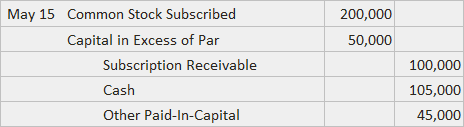

Defaulted Subscriptions

Donated Assets

Additional Paid-In Capital (APIC) FAQs

Additional paid-in capital (APIC) is the amount invested in a corporation by its owners, in addition to the par value of any capital stock.

Examples of such events include defaulted subscriptions and the acceptance of donated assets.

The easiest way would be to take the total amount accepted by the corporation from the stockholders in excess of par value, and subtract this value from capital surplus if any. If there is no capital surplus, for instance in the case of a new company that had not issued any capital stock prior to its first financing, the amount remaining after this calculation is your additional paid-in capital. Another way to calculate it would be to take the par value of stock outstanding and subtract that number from total contributed capital (par plus paid in excess of par).

You will need to use an account called "additional paid-in capital" or "paid in cap excess of par."

When transactions arise, you will need to create a separate account to record them under. This will be separate from your common stock, capital surplus, and Retained Earnings accounts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.